Liquidation of a Partnership 合伙企业的清算

The following actions must be taken to account for the dissolution of a partnership properly:

- Sell Non-Cash Assets [In general, these are assets that are not easily converted into cash unless there is a drastic price reduction] for cash

- Applying the Profit-Sharing Ratio, allocate any gain or loss from the sale of noncash assets to each partner.

- Pay any liabilities that are owed by the partnership.

- Proceed by dividing the remaining funds among the partners per the Profit-Sharing Ratio.

合伙企业若要妥善的解散,必须采取以下行动:

- 出售非现金资产 [一般来说,这些是不容易转化为现金的资产,除非价格急剧下降] 以换取现金;

- 应用利润分配比率,将出售非现金资产的任何收益或损失分配给每个合伙人;

- 支付合伙企业尚拖欠的任何债务;

- 将剩余的资金按照利润分配比例在合伙人之间进行分配。

Illustration 实例

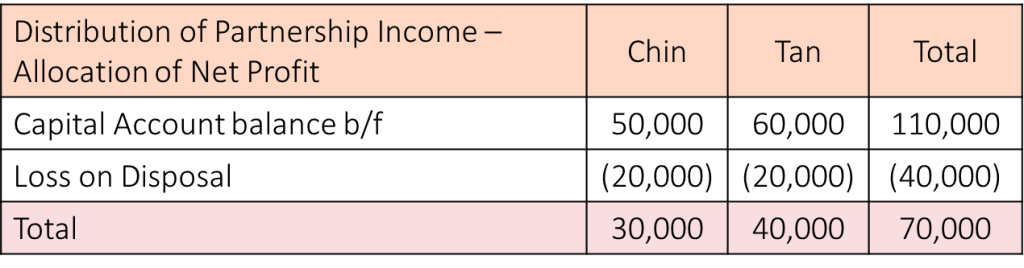

As an illustration, let’s say a partnership has two partners, partner Chin and partner Tan.

They share the partnership’s net revenue and losses proportionally (the Profit-Sharing Ratio is 1:1). Furthermore, their respective capital balances are RM50,000 and RM60,000.

The partnership has:

- cash balance of RM20,000;

- non-cash assets of RM140,000; and

- liabilities of RM50,000.

The partnership is dissolved, and noncash assets are sold for a total of RM100,000.

举个例子,假设一个合伙企业有两个合伙人,即合伙人秦和合伙人陈。

他们按比例分享合伙企业的净收入和损失(利润分配比率为1:1)。此外,他们各自的资本余额为50,000令吉及60,000令吉。

该合伙企业有:-

- 现金余额 – 20,000令吉;

- 非现金资产 – 140,000令吉;以及

- 负债 – 50,000令吉。

该合伙企业正在进行解散,因此总价值为100,000令吉的非现金资产以100,000令吉被出售。

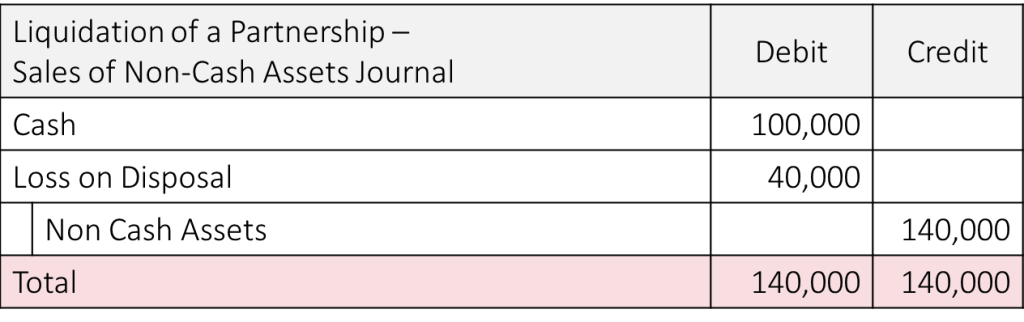

Step 1: Sell illiquid [non-cash] assets for cash 出售非现金资产以套现

The selling of the non-cash assets with a value of RM140,000 for only RM100,000 results in a loss on sale of RM40,000.

以100,000令吉出售价值140,000令吉的非现金资产,将造成40,000令吉的出售损失。

The following would be what the loss on sale of non-cash assets would be recorded as in the bookkeeping journal with double entries:

以下是出售非现金资产的损失在记账本上的复式记录:

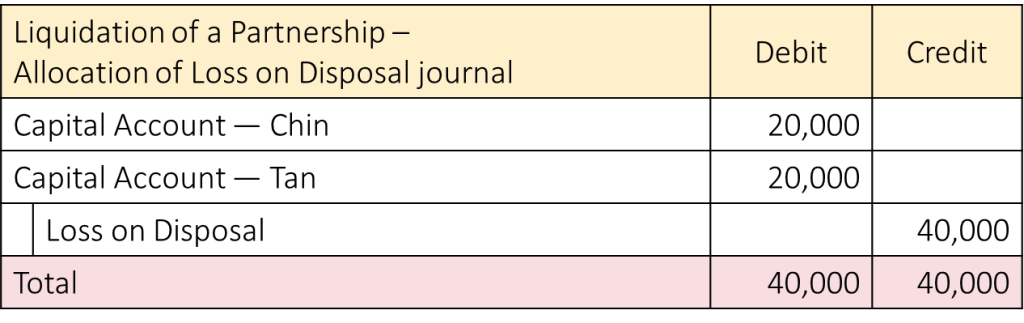

Step 2: Applying the Profit-Sharing Ratio, allocate any gain or loss from the sale of noncash assets to each partner 应用利润分配比率,将出售非现金资产的任何收益或损失分配给每个合伙人

After that, the Profit-Sharing Ratio is used to determine how much of the loss on the sale of the non-cash assets should be allocated to each partner.

之后,利润分配比率被用来确定出售非现金资产的损失应该如果分配给每个合伙人。

The following would be the entries in the double-entry bookkeeping journal that would be used to record the allocation of the loss to each partner:

以下是复式记账本中用来记录每个合伙人的损失分配的日记账:

Step 3: Pay any liabilities that are owed by the partnership 支付合伙企业尚拖欠的任何债务

Following the sale of the non-cash assets, the cash available to the partnership is equivalent to a total of RM120,000, which is comprised of:

- the opening balance of RM20,000; and

- the money obtained from the sale of the non-cash assets was RM100,000.

This cash is utilised to settle the liabilities of RM50,000, leaving a residual balance of RM70,000 to be distributed [RM120,000 minus RM50,000].

在出售非现金资产后,合伙企业手上的现金总额相当于 120,000令吉,其中包括:-

- 期初余额 – 20,000令吉;以及

- 出售非现金资产获得的资金 – 100,000令吉。

这笔现金被用来清偿 50,000令吉的负债,剩下 70,000令吉的剩余资金将被分配 [金额为120,000令吉减去50,000令吉]。

The following would be the entries that would be made in the double-entry bookkeeping journal to record the payment of the liabilities:

以下是在复式簿记中记录负债支付的日记账条目:

Step 4: Proceed by dividing the remaining funds among the partners per the Profit-Sharing Ratio 将剩余的资金按照利润分配比例在合伙人之间进行分配

The remaining cash of RM70,000 is paid out to the partners using the Profit-Sharing Ratio.

剩余的70,000令吉现金,则采用利润分配比例支付给合伙人。

The following would be the entries in the double-entry bookkeeping journal that would be used to record the distribution of the leftover funds to each partner:

以下是复式簿记日记账条目,用于记录向每个合伙人分配剩余资金的情况:

Conclusion 总结

Once all of the remaining cash from the partnership has been distributed and the journal entries that need to be made, the partnership will become zero assets and zero liabilities, allowing it to be dissolved without any problems.

In practice, winding up typically takes a significant amount of time.

If the shareholders of a partnership don’t intend to keep running the company, it is in their best interest to make preparations for exit strategies as soon as possible.

一旦合伙企业的剩余现金被分配,且日记账已被记入,合伙企业则变成零资产和零负债,从而使其得以解散。

然而现实中,一般上清盘是需要花上冗长的时间。

因此合伙企业的股东们如果不打算继续经营下去,建议应该尽早做规划。