In Malaysia, a tax rebate for the company or limited liability partnership under section 6D of the Income Tax Act 1967 refers to a tax incentive the Malaysian government provides to eligible companies and limited liability partnerships.

The tax rebate is a form of tax relief where the taxable income of the company or limited liability partnership is reduced by a specified amount, effectively lowering the amount of tax payable.

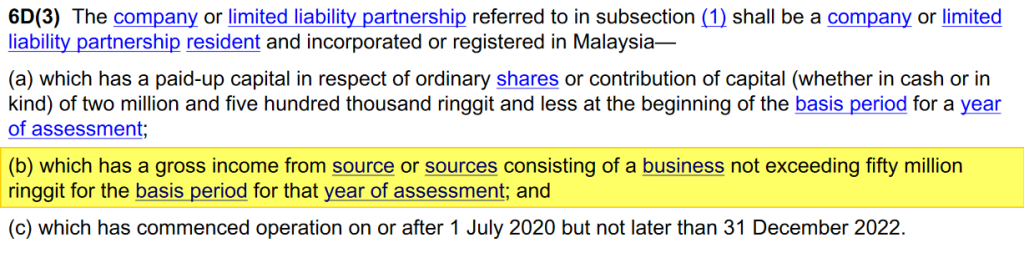

The tax rebate is available for a limited time and is subject to certain conditions:-

The Inland Revenue Board of Malaysia has issued their responses dated 29 December 2022 to CTIM members’ issues dated 21 September 2022 on the following:-

- 2% tax deducted under Section 107D of the Income Tax Act 1967

- Amended Guidelines dated 17 August 2022 on Deduction for Secretarial & Tax Filing Fees from YA 2022

- Tax rebate under Section 6D of the Income Tax Act 1967

- Gazette Order – Income Tax (Deduction for the Sponsorship of Scholarship to Malaysian Students Pursuing Studies at Technical and Vocational Certificate, Diploma, Bachelor’s Degree, Master’s Degree or Doctor of Philosophy Levels) Rules 2022 [P.U. (A) 49/2022] – w.e.f. YA 2022

This article will focus on item No 3 – Tax rebate under Section 6D of the Income Tax Act 1967; item 4 will be discussed in our upcoming articles, and items 1 & 2 have already been discussed in our previous posts.

CTIM Comments:

The LHDNM Practice Note No. 4/2020 on Clarification On Determining The Gross Income From Business Sources Of Not More Than RM50 Million Of A Company Or Limited Liability Partnership indicates that it applies to paragraphs 2A & 2D, Part 1, Schedule 1 of the Income Tax Act (ITA) 1967 and paragraph 19A(3), Schedule 3 of the ITA 1967.

Please clarify whether the LHDNM Practice Note No. 4/2020 also applies to Section 6D(3)(b) of the ITA 1967.

LHDNM’s response: Practice Note 4/2020 states that it is used to determine tax treatment under paragraphs 2A and 2D of Part 1, Schedule 1 of the Income Tax Act 1967.

For the purpose of claiming tax rebates under Section 6D of the Income Tax Act, the eligibility requirements should refer directly to that provision and the additional conditions that have been gazetted in P.U.(A) 504/2021, Income Tax (Conditions for the Grant of Rebate under Subsection 6D(4)) Order 2021.

P.U.(A) 504/2021 (the Order) was gazetted on 31 December 2021 and has effect from YA 2021 to specify the conditions imposed under Section 6D(4) of the Income Tax Act 1967 (ITA) for the purposes of the grant of tax rebate under Section 6D of the ITA.

Our website's articles, templates, and material are solely for you to look over. Although we make every effort to keep the information up to date and accurate, we make no representations or warranties of any kind, either express or implied, regarding the website or the information, articles, templates, or related graphics that are contained on the website in terms of its completeness, accuracy, reliability, suitability, or availability. Therefore, any reliance on such information is strictly at your own risk.

Keep in touch with us so that you can receive timely updates |

要获得即时更新,请与我们保持联系

1. Website ✍️ https://www.ccs-co.com/ 2. Telegram ✍️ http://bit.ly/YourAuditor 3. Facebook ✍

- https://www.facebook.com/YourHRAdvisory/?ref=pages_you_manage

- https://www.facebook.com/YourAuditor/?ref=pages_you_manage

4. Blog ✍ https://lnkd.in/e-Pu8_G 5. Google ✍ https://lnkd.in/ehZE6mxy

6. LinkedIn ✍ https://www.linkedin.com/company/74734209/admin/