The Inland Revenue Board of Malaysia (HASiL) has issued a letter dated 28 June 2023 to CTIM and other professional bodies regarding the submission requirements for Form CP22A/ CP22B/ CP21 and the online submission process for employee-related notification forms.

The letter includes the following information:-

1. Notice of cessation of employment

Section 83(3) of the Income Tax Act 1967 (ITA 1967) require every employer:

- who intends to cease employing a taxable (chargeable) or potentially taxable (likely to be chargeable) employee; or

- where an individual under his employment dies

to submit a notification (Form CP22A / CP22B) to the Director General of Inland Revenue (DGIR) at least 30 days before the cessation of employment or in respect of cessation because of death not more than thirty days after being informed of the individual’s death.

However, employers are not required to submit such notification if the income of an individual employee is subject to Monthly Tax Deduction (MTD/PCB) or if the employee’s monthly remuneration falls below the minimum amount eligible for MTD.

2. Notification for Employees intending to Leave Malaysia

Additionally, according to Section 83(4), employers are responsible for providing notice regarding employees who will be leaving Malaysia for a period of three (3) months or more by submitting a notification through Form CP21.

This notification must be made at least 30 days before the expected departure date of the employee from Malaysia.

However, if the employee’s departures are frequent and part of their employment travel, the employer is not required to submit such notification.

The Inland Revenue Board of Malaysia (LHDNM) has updated the general guidelines for employers on the Official Portal of LHDNM to assist them in determining the requirements for submitting notifications related to employees through Form CP22A, CP22B, and CP21.

The table below provides a general guide for employers to determine the submission requirements for Forms CP 22A and CP 22B:-

The table below provides a general guide for employers to determine the submission requirements for Form CP21:-

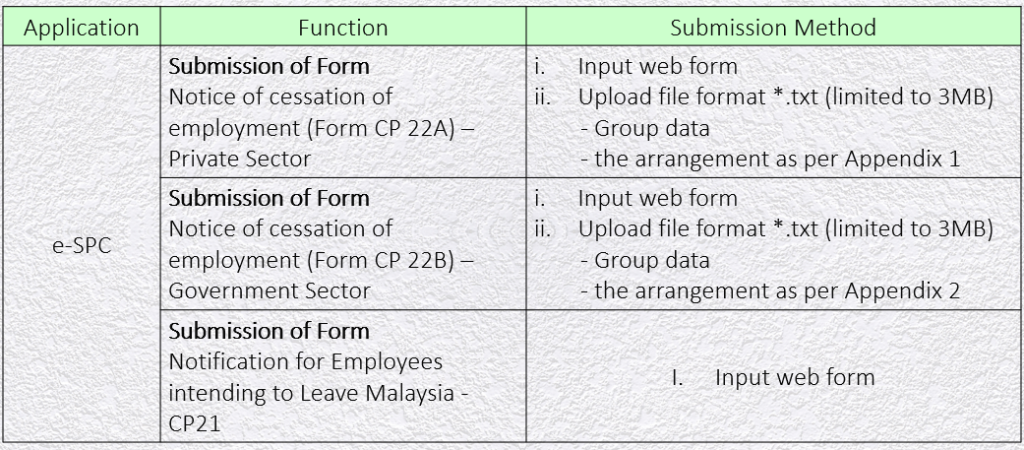

Forms CP 22A / CP 22B and CP 21 can be submitted:

- online via the e-SPC application at MyTax Portal or

- at the IRBM office, which handles the employee’s tax file.

The complete guidelines can be accessed through the link: https://www.hasil.gov.my/en/employers/termination-of-service/

The e-SPC application can be accessed through the MyTax Portal at the link https://mytax.hasil.gov.my/ > Services > e-SPC.

Employers can refer to the Information Arrangement Format provided with this letter to prepare the required CP22A, CP22B, and CP21 forms.

In line with the digital transformation of LHDNM services, starting from 1 January 2024, LHDNM will mandate online services such as e-Filing, e-SPC, and other applications as the primary medium for tax-related transactions.

Non-compliance by the employer:

- Failure to comply with the responsibility without any reasonable excuse, upon conviction of an offence, will be liable to a fine of not less than RM200 and not more than RM20,000 or to imprisonment for a term not exceeding 6 months or to both.

- An employer shall be liable to pay the full amount of tax due from his employee. The amount due from the employer shall be a debt due to the Government and may be recovered by way of civil proceedings.

Related provisions:

- Subsections 83(3), (4) and (5) of the Income Tax Act 1967

- Subsection 106 of the Income Tax Act 1967

- Subsection 107(4) of the Income Tax Act 1967

- Subsection 120(1) of the Income Tax Act 1967

Feedback

Any inquiries or feedback can be directed to HASiL through:-

- HASiL Care Line at 03-8911 1000 / 603-8911 1100 (International)

- HASiL Chat on MyTax

- Customer Feedback Form on the official LHDNM portal at the following quick link: https://maklumbalaspelanggan.hasil.gov.my/Public/

References:

Disclaimer:

The articles, templates, and other materials on our website are provided only for your reference.

While we strive to ensure the information presented is current and accurate, we cannot promise the website or its content, including any related graphics. Consequently, any reliance on this information is entirely at your own risk.

If you intend to use the content of our videos and publications as a reference, we recommend that you take the following steps:

- Verify that the information provided is current, accurate, and complete.

- Seek additional professional opinions, as the scope and extent of each issue may be unique.

免责声明:

我们网站上的文章、模板和其他材料只供参考。

虽然我们努力确保所提供的信息是最新和准确的,但我们不能保证网站或其内容,包括任何相关图形的完整性、可靠性、适用性或可用性。因此,您需要承担使用这些信息所带来的风险。

如果你打算使用我们的视频和出版物的内容作为参考,我们建议你采取以下步骤:

- 核实所提供的信息是最新的、准确的和完整的。

- 寻求额外的专业意见,因为每个问题的范围和程度,可能是独特的。

Keep in touch with us so that you can receive timely updates

请与我们保持联系,以获得即时更新。

1. Website ✍️ https://www.ccs-co.com/ 2. Telegram ✍️ http://bit.ly/YourAuditor 3. Facebook ✍

- https://www.facebook.com/YourHRAdvisory/?ref=pages_you_manage

- https://www.facebook.com/YourAuditor/?ref=pages_you_manage

4. Blog ✍ https://lnkd.in/e-Pu8_G 5. Google ✍ https://lnkd.in/ehZE6mxy

6. LinkedIn ✍ https://www.linkedin.com/company/74734209/admin/

7. Threads ✍ https://www.threads.net/@ccs_your_auditor

8. 小红书 ID ✍ 2855859831