Section 107D was incorporated into the Income Tax Act of 1967 (ITA) on January 1, 2022.

It says that companies that make payments to agents, dealers, or distributors due to sales, transactions, or schemes must withhold tax at 2% of the gross amount.

This applies to payments made to agents, dealers, or distributors who are individuals and tax residents of Malaysia and who have received more than RM100,000 (in cash or other forms) from the company in the immediate-preceding year.

Following the above, the IRB has published a FAQ document in Bahasa Malaysia on its website titled “Soalan Lazim Berkaitan Potongan Cukai 2% Terhadap Pembayaran Oleh Syarikat Pembayar Kepada Ejen, Pengedar Atau Pengagih Di Bawah Bajet 2022“, dated February 28, 2022.

These Frequently Asked Questions have been updated on August 19, 2022

On October 21, 2022, the Frequently Asked Questions (FAQ) on 2% Tax Deducted from Payment by Payer Companies to Agents, Dealers, or Distributors under Section 107D of the Income Tax Act 1967 was updated by the Inland Revenue Board of Malaysia (IRBM).

The old FAQ, which was last updated on August 19, 2022, has been replaced by this FAQ.

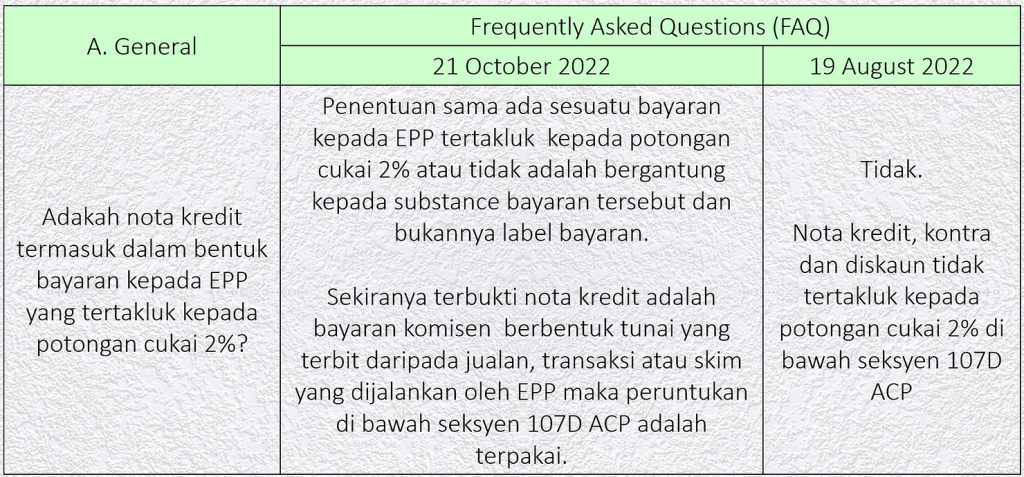

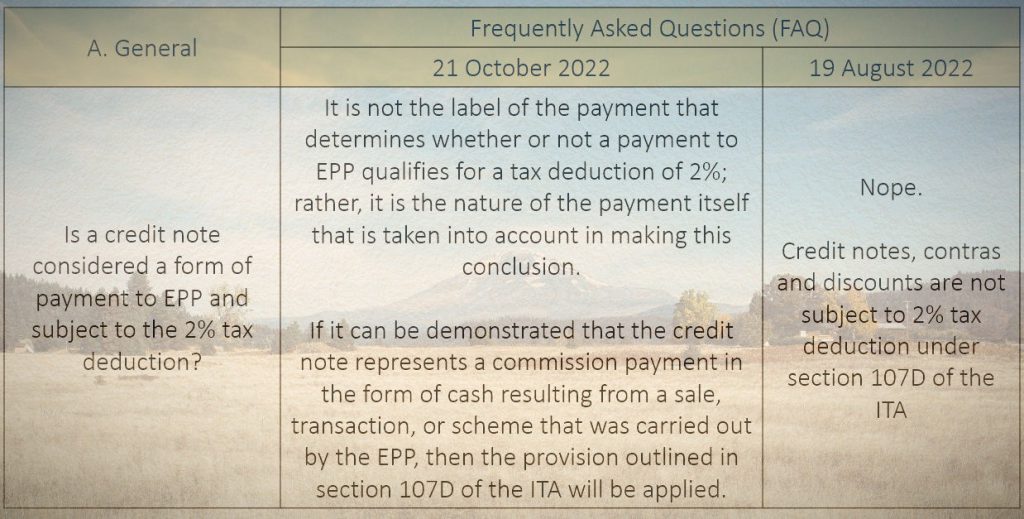

The updates are extracted below:

In English:

Reference

Both Frequently Asked Questions can be found here:-

The latest FAQ, which was last updated on 21 October 2022

The old FAQ, which was last updated on 19 August 2022

Our website's articles, templates, and material are solely for reference. Although we make every effort to keep the information up to date and accurate, we make no representations or warranties of any kind, either express or implied, regarding the website or the information, articles, templates, or related graphics that are contained on the website in terms of its completeness, accuracy, reliability, suitability, or availability. Therefore, any reliance on such information is strictly at your own risk.

Keep in touch with us so that you can receive timely updates |

要获得即时更新,请与我们保持联系

1. Website ✍️ https://www.ccs-co.com/ 2. Telegram ✍️ http://bit.ly/YourAuditor 3. Facebook ✍

- https://www.facebook.com/YourHRAdvisory/?ref=pages_you_manage

- https://www.facebook.com/YourAuditor/?ref=pages_you_manage

4. Blog ✍ https://lnkd.in/e-Pu8_G 5. Google ✍ https://lnkd.in/ehZE6mxy

6. LinkedIn ✍ https://www.linkedin.com/company/74734209/admin/