he process of spreading the total profit or net loss of a partnership among its participants in the proportion corresponding to the Profit-Sharing Ratio is referred to as the distribution of profits.

In the absence of a partnership agreement, each partner is entitled to an equal share of the partnership’s net profit or a net loss.

This would indicate that the ratio of income sharing might be expressed as 1:1 for a business with only two partners.

将合伙企业的总利润或净亏损,按照与利润分配比例 [Profit-Sharing Ratio] 在合伙人之间进行分配的过程,被称为“利润分配”。

在没有合伙协议的情况下,每个合伙人都有权获得合伙企业净利润或净亏损的平等份额。

这就表明,对于只有两个合伙人的企业来说,收入分配的比例可以表示为1:1。

What is an Appropriation Account?

An appropriation account shows how an organization’s funds are distributed among partners, shareholders, and departments.

For partnerships, it shows how profits are distributed among the partners.

什么是拨款账户?

拨款账户显示一个组织的资金是如何在合伙人、股东和部门之间作出分配的。

对于合伙企业来说,它显示利润如何在合伙人之间分配。

How does Appropriation Account work?

After finalising the business’s profit and loss account, an appropriation account for partnerships is often prepared.

It shows how the net profits are allocated among the partners, including components such as the interest each partner earned on their capital, the salary that was provided to each partner, and the share of the remaining profits each partner is entitled to receive.

拨款账户是如何运作的?

在最终完成企业的损益表后,接下来的工作通常就是要编制合伙企业的拨款账户。

它显示了净利润是如何在合伙人之间作出分配的,包括每个合伙人从其资本中获得的利息、提供给每个合伙人的工资以及每个合伙人有权获得的剩余利润份额等。

Consider the following Scenarios

Partner Chin and Partner Tan form a partnership and agree to share the net profits or the net losses equally (sharing ratio of 1:1). If the net profit for the year is RM40,000.

让我们看看以下实例

秦合伙人和陈合伙人共同成立了一家合伙企业,并同意平均分享净利润或净亏损(分享比例为1:1)。如果当年的净利润为 40,000 令吉。

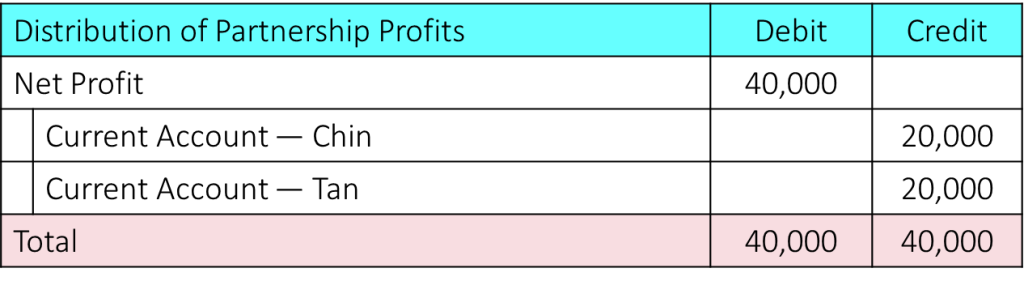

Scenario 1 – Distribution of Partnership Profits

Assuming there is no Partners’ Salary, Interest on Capital, and also Interest on Drawings during the year.

The following double-entry bookkeeping entries would be made:

情景 1– 合伙企业利润的分配

假设在这一年中没有存在任何合伙人的工资、资本的利息,以及提款的利息。

那我们将需要做以下的复式簿记分录:

The RM 40,000 in net profit is split evenly between the two partners by the transfer of RM 20,000 to each of their respective Current Accounts.

40,000 令吉的净利润在两个合伙人之间平均分配,将 20,000 令吉分别转入他们各自的往来账户。

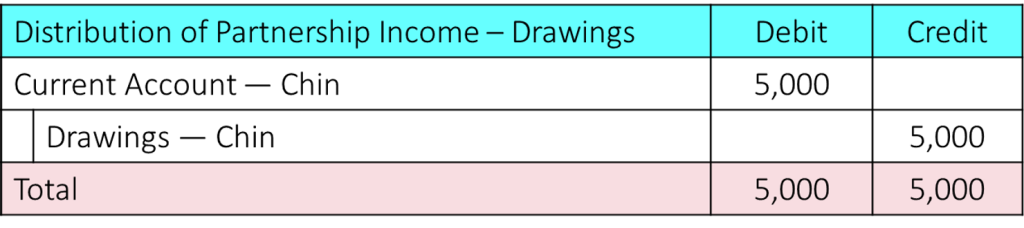

Scenario 2 – Distribution of Partnership Profits and Drawings

Continue from Scenario 1.

If Partner Chin had drawn RM 5,000 during the year, then this amount needs to be transferred to the Current Accounts using the following journal.

情景 2 — 合伙企业利润和提款的分配

继续情景 1。

如果秦合伙人在这一年中有过 5,000 令吉的提取,那么这笔钱需要用以下日记账转入往来账户。

The Current Account of Partner Chin is reduced by the drawings of RM5,000.

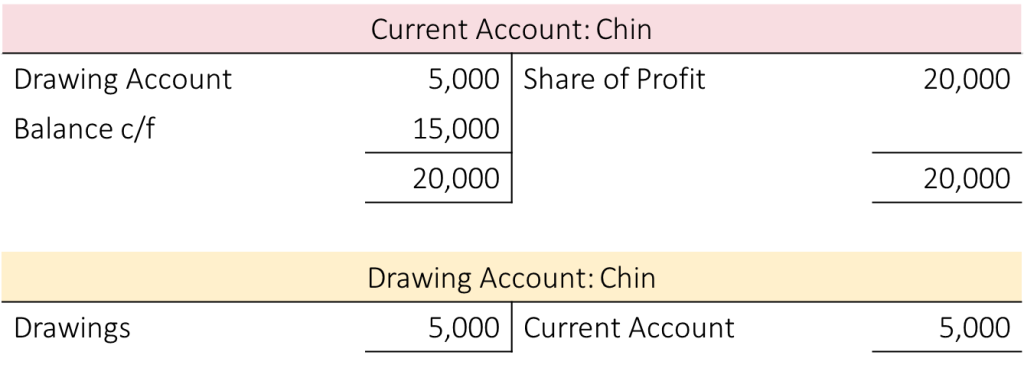

Both the Current Account and the Drawing Account that belong to Partner Chin will be as follows:

秦合伙人的往来账户被扣除了 5,000 令吉的提款。

属于秦合伙人的往来账户和提款账户,如下图所显示:

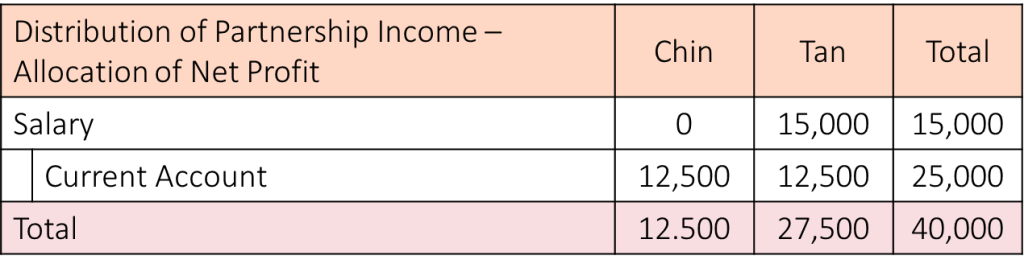

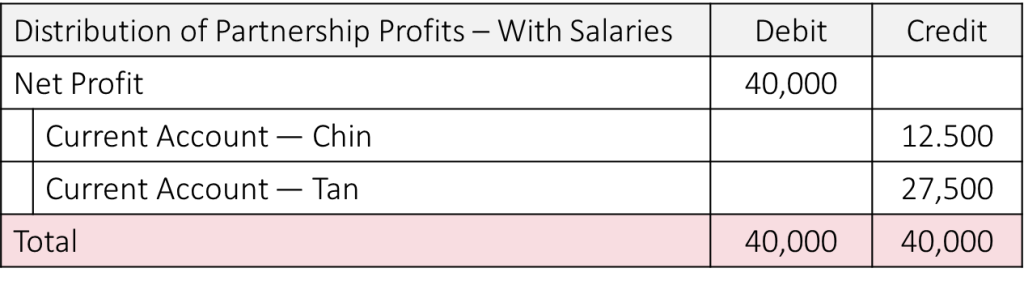

Scenario 3 – Distribution of Partnership Profits and Salaries

If the partnership had a total profit of RM 40,000, but Partner Tan had a salary of RM 15,000, then the amount that needed to be allocated equally would be RM 40,000 minus RM 15,000, which is RM 25,000.

This would mean that each partner would receive RM 25,000 divided by 2, which is RM 12,500.

Following is a breakdown of how the net profit would be distributed:

情景 3 – 合伙企业利润与薪金的分配

如果合伙企业的总利润为 40,000 令吉,但陈合伙人领了 15,000 令吉的工资,那么需要平均分配的金额为 40,000 令吉减去 15,000 令吉,即为 25,000 令吉。

这意味着每个合伙人将获得 25,000 令吉除以2,也就是 12,500 令吉。

以下是净利润如何分配的明细:

The following would be the entries in the double-entry bookkeeping journal that would be used to record the distribution of the net profit:

以下是复式记账本中用来记录净利润分配的分录:

Scenario 4 – Distribution of Partnership Profits and Interest

If the partnership had a net profit of RM 40,000, partner Chin was entitled to receive interest at a rate of 5% on the opening capital balance of RM 30,000.

Partner Chin would be entitled to receive interest equal to RM 30,000 multiplied by 5%, which is RM 1,500.

RM 40,000 minus RM 1,500 is RM 38,500, so the sum that should be split evenly between the partners would be RM 38,500 divided by 2, which comes to RM 19,250.

The distribution of the net income could look somewhat like this:

情景 4 – 合伙企业利润和利息的分配

如果合伙企业有 40,000 令吉的净利润,秦合伙人有权获得期初资本余额 30,000 令吉的5%的利息。

秦合伙人有权获得相当于 30,000 令吉乘以5%的利息,也就是 1,500 令吉。

40,000 令吉减去 1,500 令吉是 38,500 令吉,所以合伙人之间应该平均分配的金额是 38,500令吉除以 2,也就是 19,250 令吉。

净收入的分配如下:-

The double-entry bookkeeping journal to record the allocation of net income would be as follows:

记录净收入分配的复式记账本将如下:

In Practice

Using an allocation table, one can deduct any combination of salary and interest, and the final net profit or loss is then distributed among the partners according to the Profit Sharing Ratio.

It is important to note that the salary and the interest will still need to be paid even if the partnership has experienced a loss.

The net loss that was incurred will then be divided among the partners in accordance with the sharing ratio.

在实践中

使用分配表,我们可以先扣除工资和利息,然后根据利润分享率在合伙人之间分配最终的净利润或损失。

值得注意的是,即使合伙企业出现了亏损,还是需要支付工资和利息。

然后,所产生的净亏损将按照分享比率在合伙人之间进行分配。