Section 44(7) reads as follows:

In subsection (6)—

“fund” means a fund administered and augmented by an institution or organization in Malaysia for the sole purpose of carrying out the objectives for which the fund is established or held and that fund is not established or held primarily for profit;

“institution” means an institution in Malaysia which is not operated or conducted primarily for profit and which is—

- a hospital;

- a public or benevolent institution;

- a university or other educational institution;

- a public authority or society engaged solely in research or other work connected with the causes, prevention or cure of disease in human beings;

- a Government-assisted institution engaged in socio-economic research; or

- a technical or vocational training institution;

“organisation” means an organisation in Malaysia which is not operated or conducted primarily for profit and which is—

(a) an organisation established and maintained exclusively to administer and augment a public or private fund established or held for the sole purpose of the establishment, enlargement or improvement of an institution or solely for the provision of a scholarship, exhibition or prize for an individual for educational work, research work or other similar work in an institution or in what would be an institution if it were in Malaysia;

(aa) an organisation established and maintained exclusively to administer and augment a public or private fund established or held for the sole purpose of carrying out the objective in which the institution is operated or conducted;

(b) an organisation established and maintained exclusively to administer and augment a public fund established or held solely for the relief of distress among members of the public;

(c) an organisation established and maintained exclusively to administer and augment a public fund established and held solely for the purposes of religious worship or the advancement of religion and such fund is to be used—

(i) for the construction, improvement, purchase or maintenance of a building in Malaysia which is—

(A) intended to be used (and, when constructed or purchased, is used) exclusively for those purposes; and

(B) intended to be open (and, when constructed or purchased, is open) to any member of the public for those purposes; or

(ii) to provide facilities to carry on the activity related to those purposes; or

(iii) to provide for the management of the activity related to those purposes.

(d) an organisation which maintains or assists in maintaining a zoo, museum, art gallery or similar undertaking or is engaged in or in connection with the promotion of culture or the arts;

(e) an organisation engaged in or in connection with the conservation or protection of animals;

(f) a Government-assisted organisation engaged solely in addressing problems relating to industrial and commercial development and promoting and enhancing the relationship between the public sector and the private sector;

(g) a Government-assisted organisation established and maintained exclusively to administer and augment a fund established or held solely for promoting national unity;

(h) an organisation established exclusively for the conservation or protection of the environment;

(i) an international organisation as defined under the International Organization (Privileges and Immunities) Act 1992 [Act 485] carrying out such charitable activities as determined by the Minister;

(j) an organisation established and maintained exclusively to administer or augment a fund established or held for the purpose of carrying out projects towards the acculturation of the community in information and communication technology, approved by the Minister; or

(k) a benevolent fund or trust account established or held for the sole purpose of providing relief or aid to an individual who has no, or insufficient means, or in the case of a dependent individual whose parents or guardian has no, or insufficient means, to pay for the cost of the medical treatment required by such individual to treat a serious disease as defined in subsection 46(2).

Section 44(7A) is read as follows:

An institution or organisation referred to in subsection (7)—

(a) may apply not more than twenty-five per cent of its accumulated funds or that of the fund approved under subsection (6) as at the beginning of the basis period for the year of assessment for the carrying on of, or participation in, a business:

Provided that the profits or income derived therefrom shall be used solely for charitable purposes or for the primary purpose for which the institution, organisation or fund was established; or

(b) may carry out charitable activities outside Malaysia with the prior consent of the Minister.

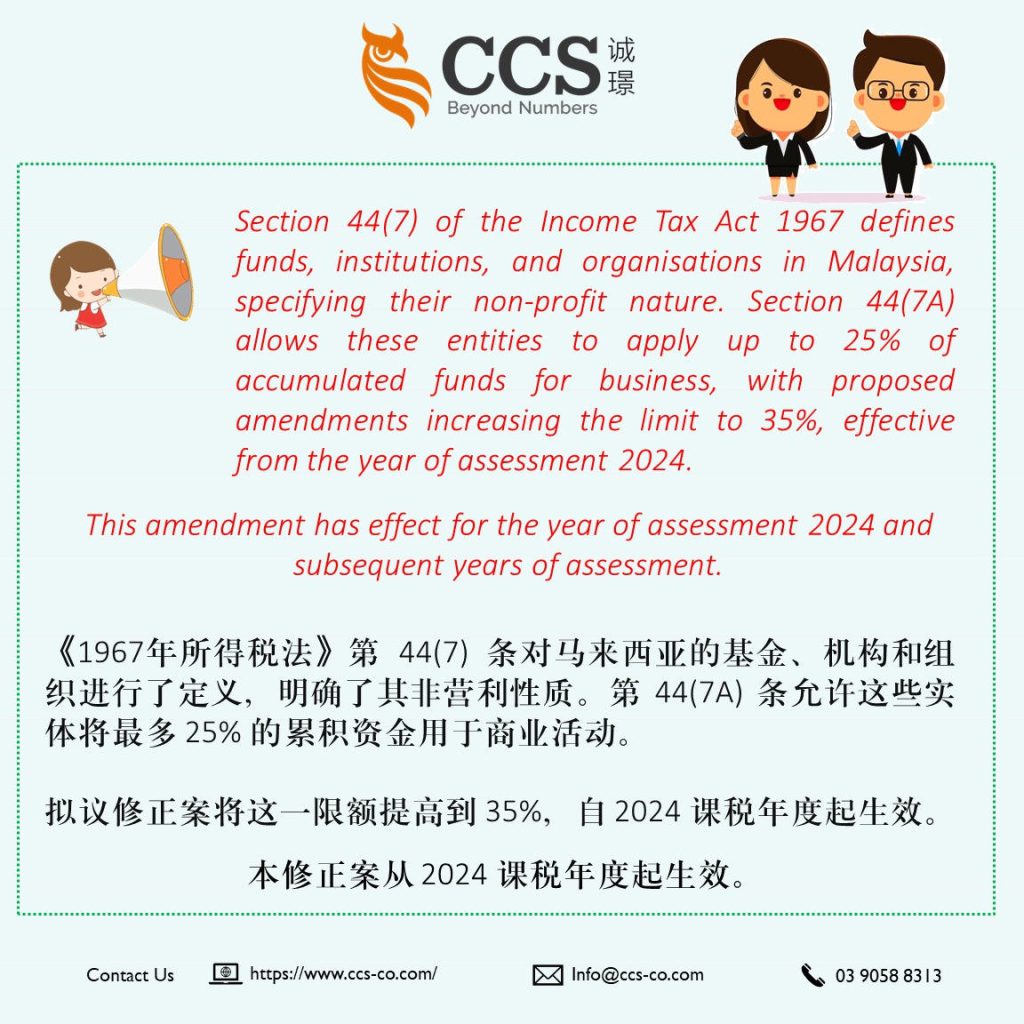

In the context of Section 44(7) and (7A) of the Income Tax Act, these provisions outline the conditions under which funds administered by institutions or organisations in Malaysia, particularly those not operated primarily for profit, can apply a portion of their accumulated funds for business activities.

Additionally, subsection 44(7A)(b) emphasises that institutions or organisations may engage in charitable activities outside Malaysia, but this requires prior consent from the Minister.

The proposed amendment in the Finance (No. 2) Bill 2023 seeks to amend subsection 44(7A) by increasing the allowable percentage of accumulated funds that can be applied for business activities from “25%” to “35%.”

This amendment has effect for the year of assessment 2024 and subsequent years of assessment.

This change has implications for the tax treatment of funds administered by qualifying institutions or organisations. Specifically:

Increased Allowable Percentage:

With the proposed amendment, these institutions or organisations can now utilise up to 35% of their accumulated funds for carrying on or participating in a business.

Tax Impact:

The amendment provides greater flexibility for qualifying entities to allocate a higher proportion of their funds for business activities.

This could lead to potential tax consequences as any profits or income generated from such business activities must still be utilised solely for charitable purposes or for the primary purpose for which the institution, organisation, or fund was established.

Charitable Purpose Requirement:

It’s important to note that despite the increased percentage, the profits derived from business activities must continue to be directed toward charitable purposes or the primary objectives of the institution, organisation, or fund.

In summary, the proposed amendment offers a higher allowable percentage for funds to be used in business activities, providing greater financial flexibility for qualifying institutions or organisations.

However, the core requirement of directing profits toward charitable purposes or the primary objectives remains unchanged.

Organisations impacted by this amendment should consider these changes in their financial planning and compliance with tax regulations.

Related-Article:

Finance (No.2) Bill 2023 – https://www.ccs-co.com/post/finance-no-2-bill-2023

Finance (No. 2) Bill 2023: Amendment of section 2 – https://www.ccs-co.com/post/finance-no-2-bill-2023-amendment-of-section-2

Budget 2024: Further Tax Deduction For Voluntary Carbon Market (VCM) – https://www.ccs-co.com/post/budget-2024-further-tax-deduction-for-voluntary-carbon-market-vcm

Amendment to Section 4 of the ITA 1967 – Gains from the Disposal of Capital Asset – https://www.ccs-co.com/post/amendment-to-section-4-of-the-ita-1967-gains-from-the-disposal-of-capital-asset