Overview:

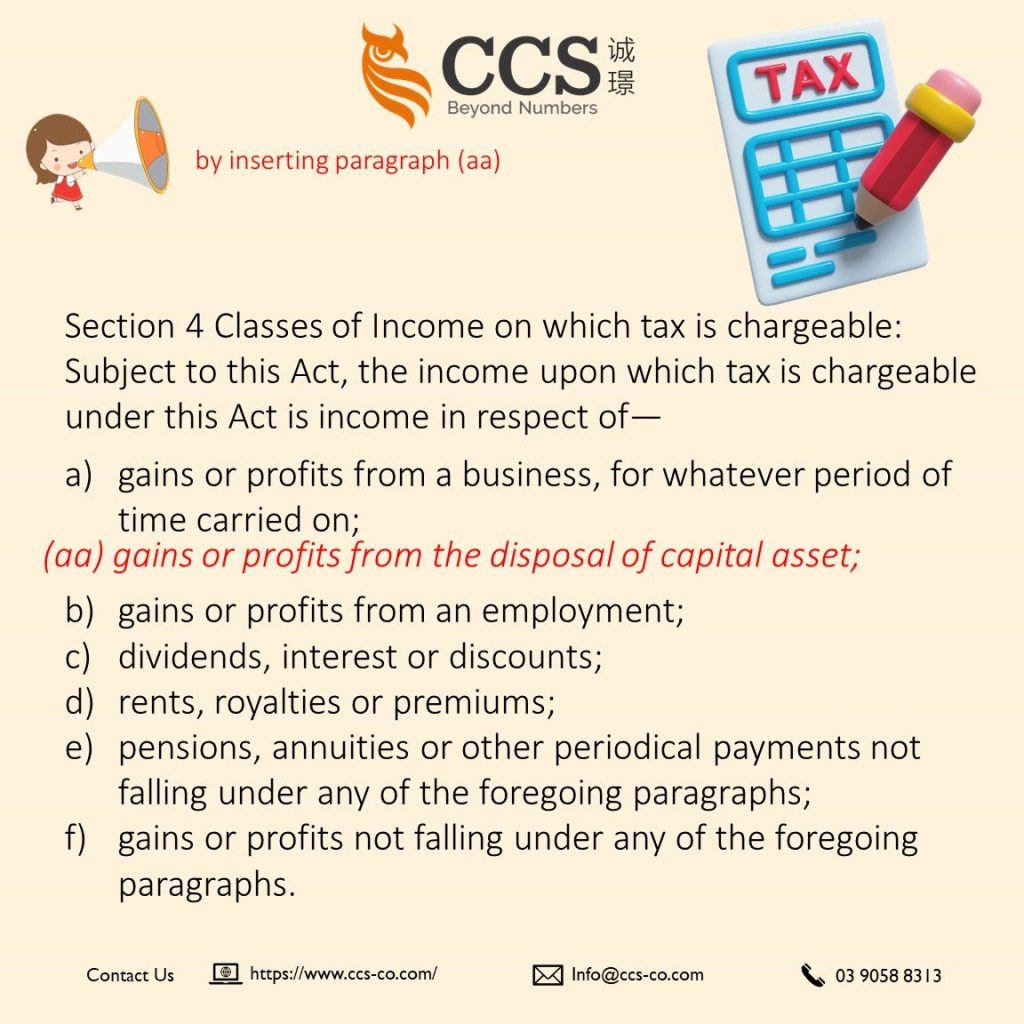

The proposed amendment to Section 4 of Act 53 introduces a significant change by inserting a new paragraph (aa), expanding the scope of income subject to taxation. Specifically, it includes “gains or profits from the disposal of capital assets” as taxable income under the Income Tax Act.

Key Points:

1) Broader Taxable Income:

Inserting paragraph (aa) broadens the categories of income subject to tax. Taxpayers must now consider gains or profits derived from the disposal of capital assets as part of their taxable income.

2) Inclusion of Capital Gains:

Previously, the Income Tax Act primarily focused on various sources of income, such as business profits, employment income, dividends, and others. With this amendment, gains or profits realised from the sale of capital assets are explicitly brought into the realm of taxable income.

3) Expanded Compliance Requirements:

Taxpayers engaging in the sale of capital assets must now adhere to additional compliance requirements associated with taxing gains or profits from such transactions. This may include detailed reporting and documentation related to capital disposals.

4) Effective Date:

The amendment takes effect from 1 January 2024. Taxpayers need to be prepared for the inclusion of gains or profits from the disposal of capital assets in their taxable income calculations starting on this date.

5) Potential Impact on Tax Liability:

Depending on the volume and nature of capital asset disposals, taxpayers may experience changes in their overall tax liability. Capital gains, now explicitly taxed, contribute to the total taxable income, potentially affecting the applicable tax rates and penalties.

6) Advisory Considerations:

Taxpayers are strongly advised to seek professional tax advice to understand the specific implications of this amendment for their financial situations. Tax consultants can provide tailored guidance on compliance, reporting, and strategies to manage potential tax implications.

7) Conclusion:

The amendment aligns with the government’s effort to enhance the tax framework and ensure more comprehensive coverage of taxable income. Taxpayers, especially those involved in the disposal of capital assets, should proactively assess and adjust their tax strategies to accommodate this expansion in the scope of taxable income.

对纳税人的影响评估: 第 53 号法案第 4 条修正案

概述:

第 53 号法案(也就是我们常说的1967年所得税法令)第 4 条文的拟议修正案通过插入新的 (aa) 段引入了一项重大变更,扩大了应纳税收入 的范围。具体而言,它将 “出售资本资产的收益或利润”列为《1967年所得税法令》规定的应税收入。

要点:

1) 更广泛的应税收入:

第(aa)段的插入扩大了应税收入的类别。

此修订生效后,纳税人现在必须将出售资本资产所得的收益或利润视为应纳税收入的一部分。

2) 包括资本收益:

以前,《1967年所得税法令》主要关注各种收入来源,如:营业利润、就业收入、股息等。此次修订后,出售资本资产实现的收益或利润被明确纳入应税收入范畴。

3) 扩大了合规要求:

出售资本资产的纳税人,现在必须遵守与此类交易收益或利润征税相关的额外合规要求。这可能包括与资本出售相关的详细报告和文件。

4) 生效日期:

该修正案自 2024 年 1 月 1 日起生效。

纳税人需要做好准备,从这一天开始,需要将出售资本资产的收益或利润纳入应税收入计算。

5) 对纳税义务的潜在影响:

根据资本资产出售的数量和性质,纳税人的总体税负可能会发生变化。

把资本资产出售的收益或利润计入应税收入总额后,势必影响适用税率和税负。

6) 咨询考虑:

强烈建议纳税人寻求专业税务建议,以了解该修正案对其财务状况的具体影响。

税务顾问可就合规性、报告和管理潜在税务影响的策略提供量身定制的指导。

7) 结论:

该修正案与政府为加强税收框架,并确保更全面地涵盖应纳税收入所做的努力相一致。

纳税人,尤其是涉及资本资产出售的纳税人,应积极评估并调整其税务策略,以适应应税收入范围的扩大。

Related-Article:

Finance (No.2) Bill 2023 – https://www.ccs-co.com/post/finance-no-2-bill-2023

Finance (No. 2) Bill 2023: Amendment of section 2 – https://www.ccs-co.com/post/finance-no-2-bill-2023-amendment-of-section-2