Acquisitions are a standard business practice, and several motivations exist behind this. For instance, they may be interested in increasing their overall size, diversifying the types of products they sell or services they provide, or expanding into new markets or geographical areas.

However, the question that needs to be answered is how we can determine whether or not the transaction is considered a business combination. What exactly does it imply when people talk about business combinations?

The accounting for acquisitions can be complex and begins with determining whether a transaction is a business combination.

Scope of MFRS 3 Business Combinations

This MFRS applies to a transaction or other event that meets the definition of a business combination.

This MFRS does not apply to:

- the formation of a joint venture

- the acquisition of an asset or a group of assets that does not constitute a business.

- a combination of entities or businesses under common control

What is a business combination?

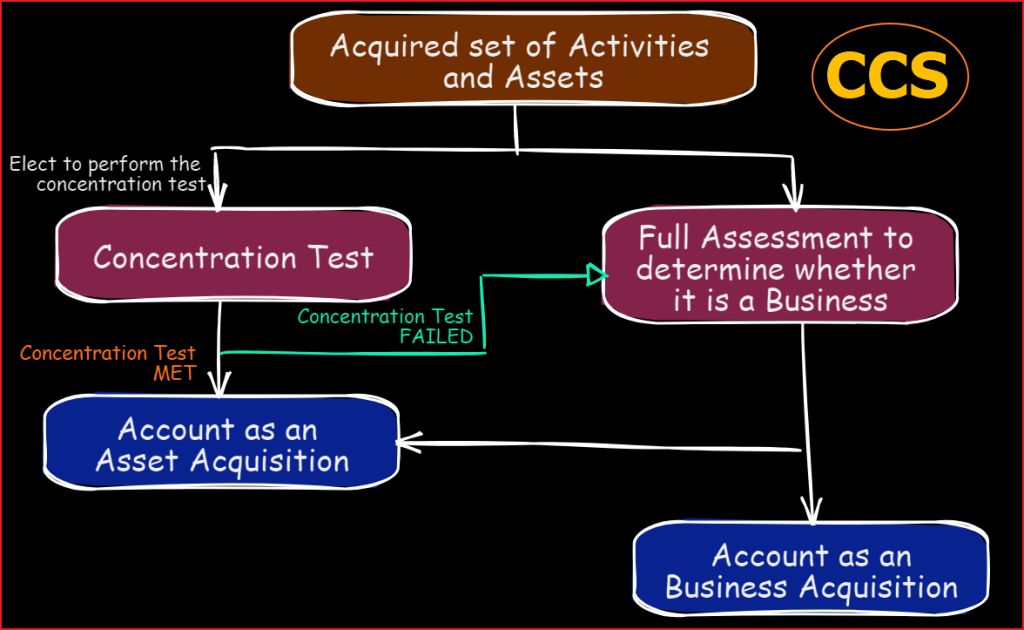

An acquisition is a business combination when the assets acquired, and liabilities assumed constitute a business. If an acquisition does not involve the purchase of a business, an entity accounts for it as an asset acquisition.

What is a business? MFRS 3 defines a business as:

“an integrated set of activities and assets that is capable of being conducted and managed to provide goods or services to customers, generating investment income (such as dividends or interest) or generating other income from ordinary activities.“

A business consists of inputs and processes applied to those inputs that have the ability to contribute to the creation of outputs. The three elements – input, processes and outputs – constitute a business.

To decide whether or not the acquired combination of activities and assets constitutes a business, entities must determine and assess the relevant factors. When we talk about this method, we refer to it as “the full assessment approach.”

Full Assessment Approach

Under the full assessment approach, entities need to assess the three elements. The three elements are explained in the table below:

The Concentration Test

MFRS 3 sets out an optional test (the concentration test) to permit a simplified assessment.

The acquired set of activities and assets is not a business if the concentration test is met.

An entity may elect to apply or not apply for the test. An entity may make such an election separately for each transaction or event.

On the other hand, if an entity fails the test or chooses not to apply the test, then that entity is obligated to carry out the full assessment to decide whether or not the acquisition is a business.

What exactly the Concentration Test is?

The entity carries out this test to determine the degree to which the acquired set of activities and assets are concentrated regarding their fair value. If substantially all of the fair value of the gross assets acquired is concentrated in a single or a group of similar identifiable assets, then the concentration test has been satisfied.

As part of the concentration test, the following requirements must be met by entities:

- Firstly, gross assets acquired — Exclude cash and cash equivalents, deferred tax assets, and goodwill resulting from the effects of deferred tax liabilities.

- Secondly, the fair value of the gross assets acquired – Includes any consideration transferred (plus the fair value of any non-controlling interest and the fair value of any previously held interest) in excess of the fair value of net identifiable assets acquired. T

- Thirdly, single identifiable asset – Include any asset or group of assets that would be recognised and measured as a single identifiable asset in a business combination.

- Fourthly, tangible asset – A tangible asset that is attached to and cannot be physically removed and used separately from another tangible asset (or from an underlying asset subject to a lease, as defined in MFRS 16 Leases) without incurring significant costs or diminution in utility or fair value to either asset (for example, land and buildings), those assets are considered as a single identifiable asset.

- Lastly, similar assets — Entities should consider the nature of every single identifiable asset and the risk associated with managing and creating outputs from the assets.

Substantive Process

However, to be considered a business, an integrated set of activities and assets must include, at a minimum, an input and a substantive process that significantly contribute to the ability to create output.

In other words, the two essential elements of a business are inputs and processes. It is unnecessary to include all of the inputs or processes that the seller used to operate that business.

Notably, the process in question needs to be a substantive process for input and the process combined to significantly contribute to the capability of producing output.

Even if an acquired set of activities and assets has outputs, the continuation of revenue does not indicate that both an input and a substantive process have been acquired.

Depending on whether a set of activities and assets have outputs or not at the acquisition date, an acquired process is a substantive process only if:

1. A set of activities and assets does not have outputs at the acquisition date

- it is critical to the ability to develop or convert an acquired input or inputs into outputs; and

- the inputs acquired include both an organised workforce that has the necessary skills, knowledge, or experience to perform that process (or group of processes) and other inputs that the organised workforce could develop or convert into outputs.

2. A set of activities and assets has outputs at the acquisition date

- is critical to the ability to continue producing outputs, and the inputs acquired include an organised workforce with the necessary skills, knowledge, or experience to perform that process (or group of processes); or

- significantly contributes to the ability to continue producing outputs and:

- is considered unique or scarce; or

- cannot be replaced without significant cost, effort, or delay in the ability to continue producing outputs

评估所取得的过程是否是实质性的

为确定所取得的过程是否是实质性的,需视在购买日是否具有产出而应用不同的标准。

对于在购买日不具有产出的一组活动和资产的集合,如果同时满足下述两项标准,则所取得的过程是具有实质性的:

- 该过程对将所取得的一项或多项投入开发或转换为产出的能力至关重要;

- 所取得的投入同时包括具备实施该过程(或一组过程)的必要技能、知识或经验的有组织的员工,以及员工能够用于开发或转换为产出的其他投入。

对于在购买日具有产出的一组活动和资产的集合(即,在购买日产生收入的活动和资产的 集合),如果符合下述两种情形之一,则所取得的过程具有实质性:

- 该过程对继续生产产出的能力至关重要,且所取得的投入包括具备实施该过程 (或一组过程)的必要技能、知识或经验的有组织的员工;

- 该过程能够显著促进持续生产产出的能力,且

- 被认为是独特或稀缺的;或

- 不能在不付出重大成本、努力或延误继续生产产出的能力的情况下被置换。

Conclusion

The information provides an overview of the primary considerations for determining a business combination.

MFRS 3 – Business Combinations

Business Combinations

Our website's articles, templates, and material are solely for reference. Although we make every effort to keep the information up to date and accurate, we make no representations or warranties of any kind, either express or implied, regarding the website or the information, articles, templates, or related graphics that are contained on the website in terms of its completeness, accuracy, reliability, suitability, or availability. Therefore, any reliance on such information is strictly at your own risk.

Keep in touch with us so that you can receive timely updates |

要获得即时更新,请与我们保持联系

1. Website ✍️ https://www.ccs-co.com/ 2. Telegram ✍️ http://bit.ly/YourAuditor 3. Facebook ✍

- https://www.facebook.com/YourHRAdvisory/?ref=pages_you_manage

- https://www.facebook.com/YourAuditor/?ref=pages_you_manage

4. Blog ✍ https://lnkd.in/e-Pu8_G 5. Google ✍ https://lnkd.in/ehZE6mxy

6. LinkedIn ✍ https://www.linkedin.com/company/74734209/admin/