1. Companies are required to pay tax in monthly instalments depending on estimated tax liabilities. Each month’s instalments must be paid on or by the 15th of the month.

2. A 10% penalty may be imposed for late or inadequate payments. If the actual tax payable exceeds the estimate by more than 30%, a 10% penalty will be imposed.

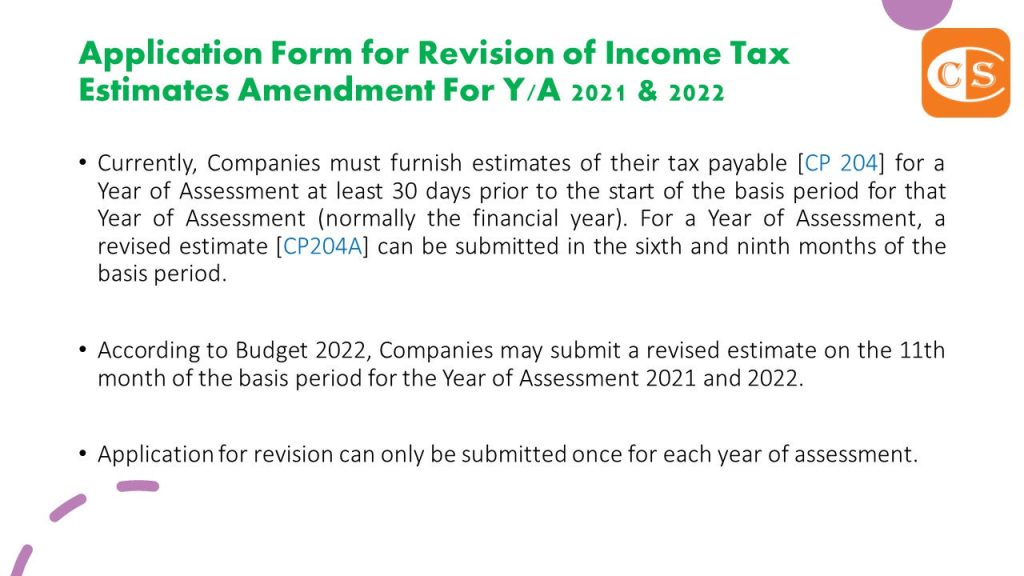

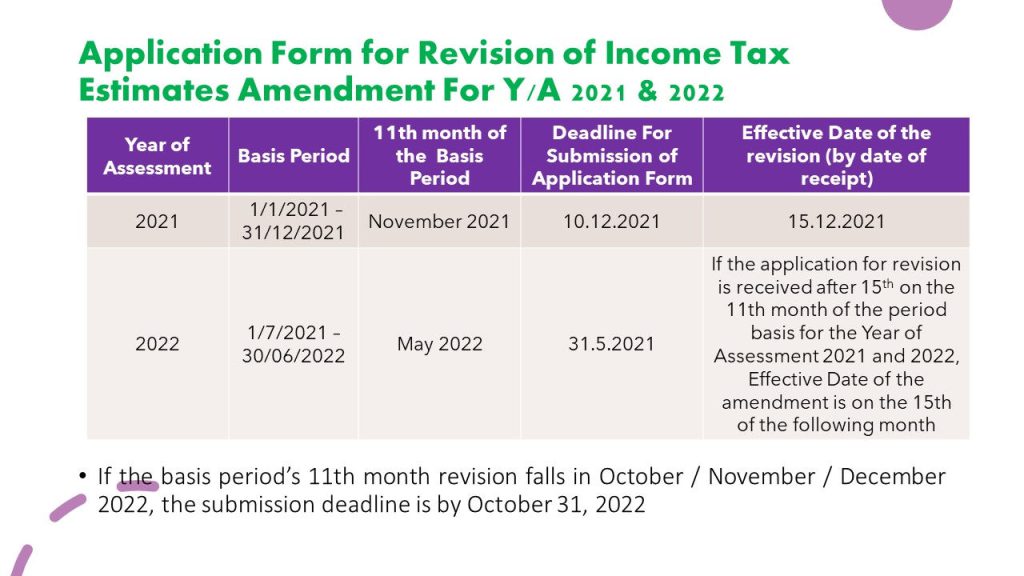

3. According to Budget 2022, Companies may submit a revised estimate on the 11th month of the basis period for the Year of Assessment 2021 and 2022.

4. On its website, the Malaysian Inland Revenue Board has uploaded the Application Form (in Bahasa Malaysia version only)

5. The LHDNM has also uploaded the Frequently Asked Questions (FAQs) dated November 25, 2021 (in Bahasa Malaysia only). 6. To Download Application Form & FAQs – https://www.ccs-co.com/publications

🌻🌻🌻🌻🌻🌻🌻🌻🌻🌻🌻

1. 公司需要根据预估应缴所得税,按月分期缴税。每个月的分期付款必须在该月的15日或之前支付。 2. 举凡逾期支付或没有支付,可处以10%的罚款。如果最终实际应缴税款超过估算的30%或以上,之间的差额将被处以10%的罚款。

3. 2022年预算案宣布,公司可以在2021年和2022年的课税年度基础期内的第11个月提交预估应缴所得税修订 [CP 204A]。

4. 在其官方网站上,马来西亚税收局已经上传了申请表格(国文版本)

5. 2021年11月25日,马来西亚税收局也上传了的常见问题解答(FAQ)(国文版本)。

6. 下载第11个月修订表格以及 FAQ – – https://www.ccs-co.com/publications