The word “materiality” basically means how important or significant something is in relation to the financial statements as a whole.

ISA 320 Materiality in Planning and Performing an Audit says [defines] the following about the term:

‘A matter is material if its omission or misstatement would reasonably influence the economic decisions of users taken on the basis of the financial statements.’

This definition basically says that whether something is “material” or not depends on how big the item is or how important the error or omission on the financial statements is.

The main objective of the external audit is for the auditor to express an opinion on whether or not the financial statements show a true and fair view of the business (or present fairly in all material respects).

This level of assurance is high but not absolute.

This is because the auditor can’t test every single transaction or event that goes into a reporting entity’s financial statements.

In addition to this limitation, there is also a degree of estimation in financial statements. Because of this, it is generally accepted in the business world that financial statements will never be 100% accurate in every way.

Example

A manufacturing company is in the business of manufacturing coffee powder.

At the end of the year, several containers with different ingredients go into making coffee powder.

These containers must be valued to be included in the reporting entity’s closing inventory valuation.

All of these kinds of products will be called “work-in-progress,” and work-in-progress will always contain a degree of estimation in relation to the actual cost of the product still in production at year-end, together with estimations of overhead absorption (both fixed and variable) such as factory heat and light and direct labour costs.

Most of the time, these valuations are done by management based on their “best estimates.”

The example above showed how a reporting entity would use accounting estimates to create a balance for the financial statements (i.e. work-in-progress, which will be included within current assets).

In this case, the auditor will follow a certain standard for auditing:

ISA 540 Auditing Accounting Estimates, Including Fair Value Accounting Estimates and Related Disclosures.

Types of Materiality

There are two types of materiality:

- Financial Statement Materiality; and

- Performance Materiality.

Financial statement materiality is calculated for the financial statements as a whole (see later), and this calculation is based on the auditor’s experience and judgement.

Performance materiality is the amount or amounts set by the auditor that are less than materiality for the financial statements as a whole.

This is done to make it less likely that the total number of uncorrected and undetected mistakes will add up to more than what is considered “material” for the financial statements.

Thus, performance materiality reduces the probability that the aggregate amount of uncorrected and undetected misstatements exceeds the materiality level for the financial statements.

The level of performance materiality selected is a matter of professional judgment and is impacted by the auditor’s understanding of the client, including the types and amounts of misstatements found during previous audits of the client; these matters impact the auditor’s expectations regarding misstatements that might be present in the current period. The performance materiality level can be set at different levels for different accounts.

Example

An audit senior has determined that the materiality of financial statements for the audit of ABC Corporation is RM65,000.

Here are some excerpts from the financial statements of ABC Corporation:

- Turnover – RM7.5 million

- Trade and other receivables – RM2.6 million

- Cash at the bank – RM0.75 million

- Trade payables – RM1.4 million

Now think about what would happen if the financial statement materiality of RM65,000 was used for all of the above areas.

There will be several balances or parts of balances that the auditor does not test because they are less than the RM65,000 “materiality level” for financial statements.

Suppose the auditor only looked at what was important in the financial statements. In that case, the untested items could have misstatements that could add up to material [big] misstatements when added to other misstatements. This is where the idea of how important performance materiality is comes into play.

So, performance materiality is a lower level of materiality than that set for the financial statements as a whole.

This lower level of materiality is used during sampling to reduce the risk of small errors [immaterial misstatements] becoming big ones [material] when they are added up.

ISA 320 adds to the definition of performance materiality by saying that performance materiality:

‘also refers to the amount or amounts set by the auditor at less than the materiality level or levels for particular classes of transactions, account balances or disclosures.’

There are no formulas in ISA 320 that say how performance materiality should be calculated. Instead, the auditor uses his or her own judgement, taking the following things into account:

- The nature and extent of misstatements that were identified in prior year audits;

- The auditor’s understanding of the entity and the environment in which it operates; and

- The result of the auditor’s risk assessment procedures.

Calculation of financial statement materiality

Again, it’s up to the auditor’s professional judgement to come up with a materiality level for the financial statements as a whole.

But over the years, it has become common to put percentages on certain parts of the financial statements and use those numbers to figure out the materiality level of the financial statements.

For example:

- ½ to 1% of turnover

- 1 to 2% of gross assets (non-current + current assets (also known as the statement of financial position/balance sheet total))

- 5% of profit before tax

- 2 to 5% of net assets

Whilst not as common in real-life practice, it is not unheard of for ½ to 1% of gross profit to be included in the above percentage calculations.

Most audit methods use the “averaging” method to determine financial statement materiality level.

This is where three elements of the financial statements will be used, percentages applied and then an average worked out to arrive at a financial statement materiality level.

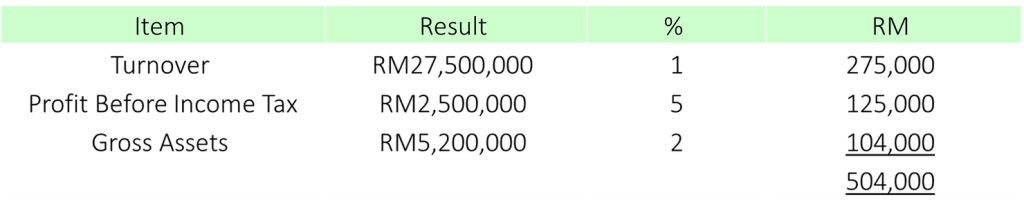

Example

Here are some extracts from a client’s financial statements from the planning stage:

- Turnover – RM27.5 million

- Profit before income tax – RM2.5 million

- Non-current assets [NBV] – RM1.2 million

- Current assets – RM4 million

Using the averaging method, financial statement materiality at the planning stage can be calculated as follows:

So, RM504,000/3 = RM168,000, and using the averaging method; this is how important each item is on the financial statement as a whole.

The auditor could reduce this by a certain percentage to get to a performance materiality level.

For example, they could reduce the financial statement materiality by 75% to arrive at a performance materiality level.

However, this is not a rule, and it is up to the auditor to decide how they will reach a performance materiality level.

Using percentages to determine a financial statement’s materiality level is not prescriptive, and the benchmarks above are only meant as a guide.

Since no two audits are the same, it may be better to use different ways to calculate the financial statement’s materiality level. Depending on the level of risk, the auditor may decide that the above calculations give a materiality level that is too high. In this case, they may either lower the percentages (based on their past experience and risk assessment) or use a different method to determine the materiality of a financial statement.

Materiality considerations during the course of the audit

Materiality, like planning, doesn’t end once it’s been figured out.

Things could happen during the detailed audit work that would have led the auditor to a different materiality level during the planning phase.

Because of this, the auditor must always keep in mind that he or she needs to go back to the planning phase and make any changes that are needed based on what was found during the detailed audit work (this links into the concept of planning being an iterative and continuous process).

Suppose a situation makes the auditor think that a lower financial statement materiality level would have been set during planning. In that case, the auditor must also look at performance materiality and decide if it needs to be changed because of the situation.

This would be the case where the results of the financial statements are going to change (which would then give rise to a need to revise materiality levels).

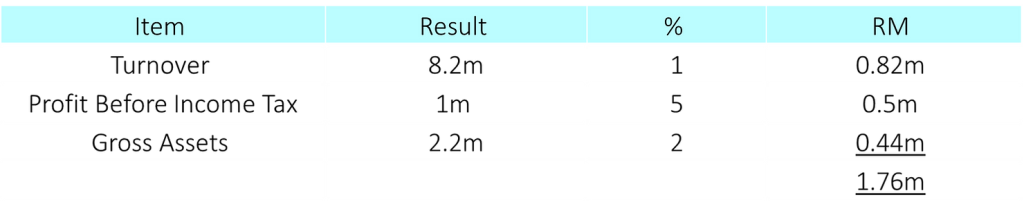

Here are some extracts from XYZ Corporation’s financial statements for the year that ended on December 31, 2021, along with the materiality levels that were calculated at the planning stage using the averaging method:

Financial statement materiality:

= 1.76m / 3

= RM59,000 (rounded up)

The performance materiality level is 65% of financial statement materiality, hence

= (RM59,000—(RM59,000 × 65/100))

= RM20,650

During the review of correspondence from the company’s lawyers, the audit senior noticed that the company had been fined for the illegal dumping of toxic waste amounting to $500,000 plus costs of RM100,000.

The company was taken to court in October 2021, and the fine was paid in February 2022, as ordered by the courts.

The directors didn’t tell the auditors about this fine at the pre-audit meeting in October 2021, and nothing has been written down about it in the planning.

The finance director said that he didn’t think it was important to bring this to the attention of the audit firm because it wouldn’t be paid until the next financial year. Because of this, it didn’t have anything to do with the audit of the financial statements for December 31, 2021.

IAS 10: Events after the Reporting Period [Malaysia: MFRS 110] would be especially important in this case.

The fact that the company was prosecuted DURING the financial year to 31 December 2021 means that these conditions existed at the end of the year.

The fine is an adjusting event under IAS 10, so the financial statements for the year ended 31 December 2021 should have taken this fine into account.

So, it’s wrong that the director put the fine in the next financial year. If the auditor had known about it, it would have caused them to arrive at a different materiality level (and performance materiality level).

If this fine had been added as IAS 10 required, the profit before income tax would have been RM400,000.

This is because RM1 million minus RM500,000 minus RM100,000 is RM400,000.

Finance statement materiality levels would have been:

= (RM0.82 + RM0.20 + RM0.44) / 3

= RM49,000 (rounded up).

Performance materiality would have been:

= RM49,000 – (RM49,000 × 65/100)

= RM17,150.

This scenario highlights a situation where the auditors have discovered an event during the course of the audit of which they were previously unaware and which would have otherwise resulted in a lower financial statement materiality level and a lower performance materiality level.

Other considerations

When the auditor detects transactions or events that he or she didn’t know about before, he or she must also decide if the nature, timing, and scope of any further audit procedures should still be done.

Obviously, if the situation is caused by fraud and/or an error, the auditor should extend the nature, timing and extent of planned further audit procedures.

Documentation of materiality

ISA 320 requires the auditor to document various aspects of materiality, including:

- Materiality calculated for the financial statements as a whole;

- Materiality level(s) for particular classes of transactions account balances or disclosures(where applicable);

- Performance materiality; and

- Revisions made to financial statement and

- performance materiality as the audit progresses.

Even if the auditor has found few or no misstatements, that doesn’t mean that the auditors should disregard materiality levels at the completion phase of the audit.

At the end of the audit, the auditor should check the materiality levels to ensure they still remain appropriate.

To do this, the auditor should look at the results of the audit procedures performed, and any misstatements found. The auditor should also evaluate these misstatements according to ISA 450 Evaluation of Misstatements Identified During the Audit.

When these misstatements are getting close to the materiality levels, the auditor should consider whether they need additional audit procedures to lower the risk of material misstatements.

Our website's articles, templates, and material are solely for you to look over. Although we make every effort to keep the information up to date and accurate, we make no representations or warranties of any kind, either express or implied, regarding the website or the information, articles, templates, or related graphics that are contained on the website in terms of its completeness, accuracy, reliability, suitability, or availability. Therefore, any reliance on such information is strictly at your own risk.

Keep in touch with us so that you can receive timely updates |

要获得即时更新,请与我们保持联系

1. Website ✍️ https://www.ccs-co.com/ 2. Telegram ✍️ http://bit.ly/YourAuditor 3. Facebook ✍

- https://www.facebook.com/YourHRAdvisory/?ref=pages_you_manage

- https://www.facebook.com/YourAuditor/?ref=pages_you_manage

4. Blog ✍ https://lnkd.in/e-Pu8_G 5. Google ✍ https://lnkd.in/ehZE6mxy

6. LinkedIn ✍ https://www.linkedin.com/company/74734209/admin/