The Finance (No 2) Bill 2023 has been officially unveiled, comprising a comprehensive 231 pages that delve into pivotal amendments in various aspects of taxation.

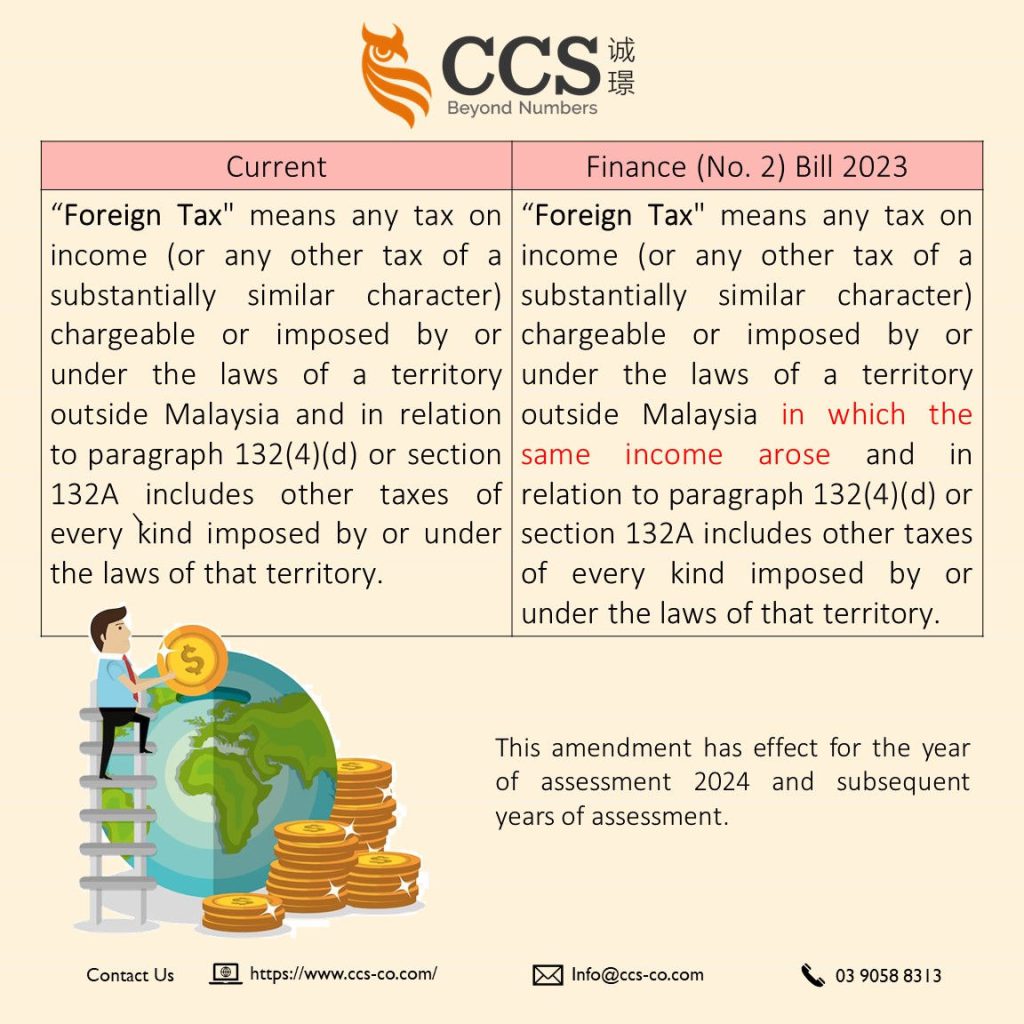

Among the notable changes lies a modification to Section 2 of the Income Tax Act 1967, specifically altering the definition of “Foreign Tax.”

Key Amendment: Redefining “Foreign Tax”

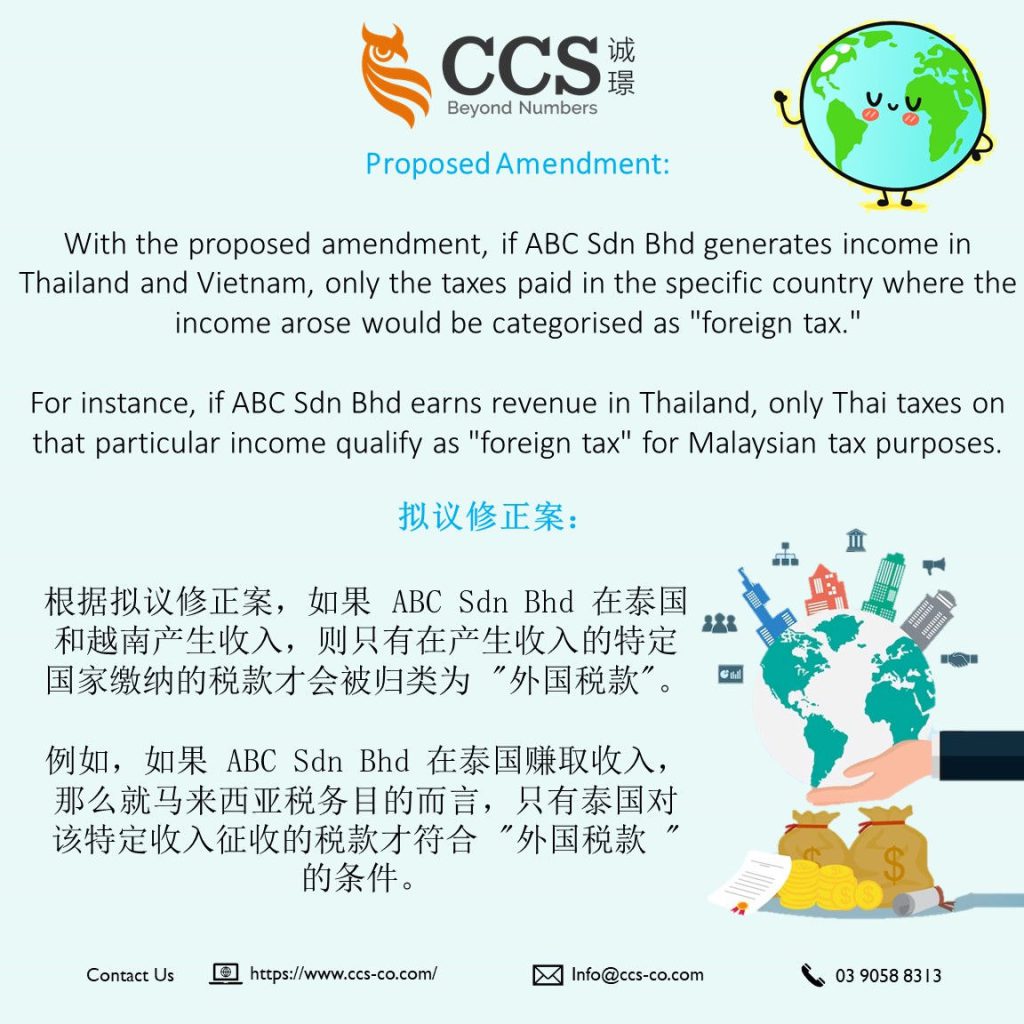

The proposed alteration emphasises that foreign tax should be identified based on the territory where the income arises.

As businesses, this amendment necessitates a strategic and meticulous approach to handling international income and tax calculations.

Considerations for Businesses:

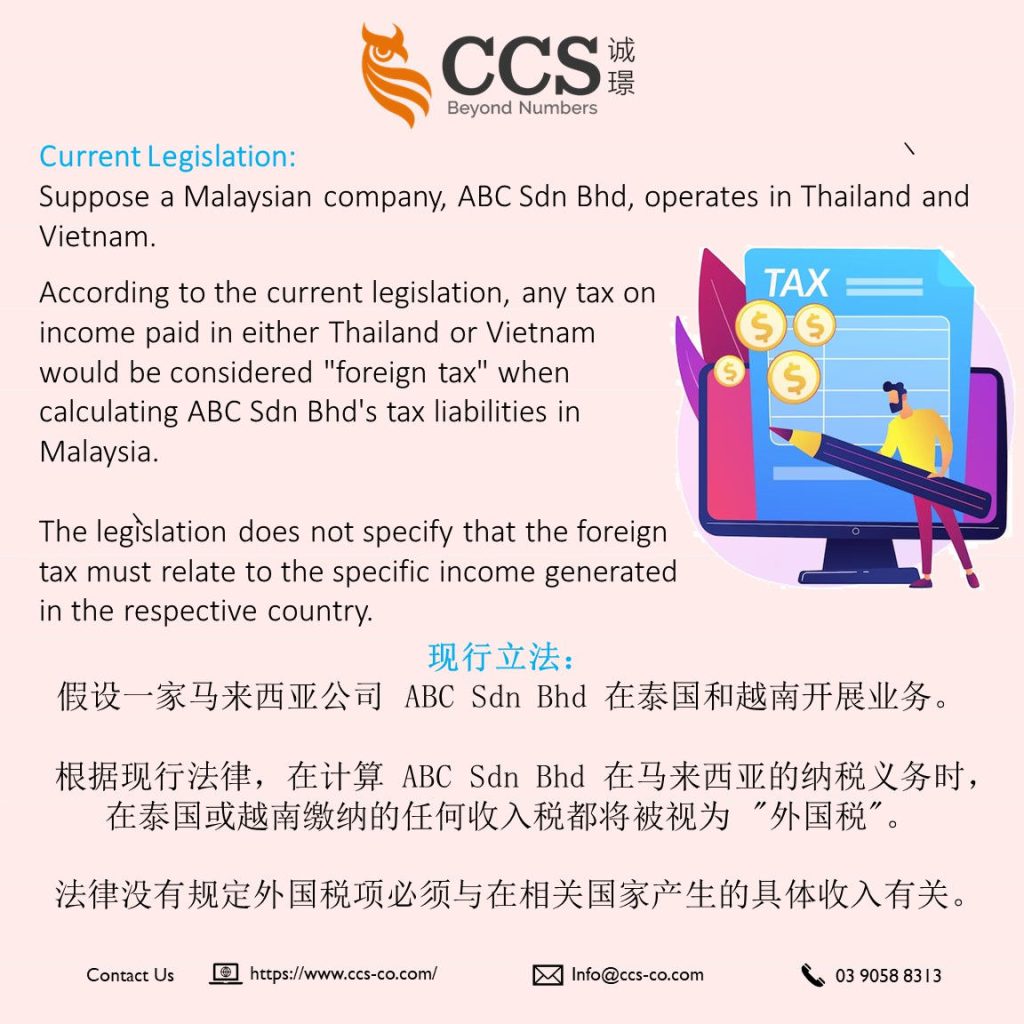

1) Specificity of Income Sources:

Businesses must meticulously identify and attribute income to the precise foreign territory where it is generated. This precision is foundational for calculating the applicable “foreign tax” under the revised definition.

2) Review of Tax Jurisdiction Rules:

Companies operating across multiple foreign territories should comprehensively review the tax jurisdiction rules in each country.

Understanding how income is taxed in these jurisdictions is imperative for aligning tax calculations with the proposed amendment.

3) Documentation and Record-Keeping:

Thorough documentation and record-keeping practices are non-negotiable.

Businesses need to maintain detailed records related to income generation in foreign territories, encompassing transaction specifics, revenue sources, and associated taxes paid.

4) Consultation with Tax Professionals:

Given the intricacies of international tax matters, businesses are strongly advised to engage with tax professionals specialising in cross-border taxation.

Their expertise will guide businesses in interpreting and applying the amended definition to their specific scenarios.

5) Impact on Tax Liabilities:

An assessment of how the proposed amendment may influence overall tax liabilities in Malaysia is crucial.

The clarification that foreign tax pertains to the territory where income arises can potentially impact the calculation of foreign tax credits or exemptions.

6) Stay Informed on Changes:

Tax laws are dynamic and subject to updates and changes. Staying informed about additional guidance or alterations related to the amended definition is essential. Regularly checking for updates from tax authorities is recommended.

Essentially, the focus is aligning tax calculations with the specific foreign territory where income is generated.

Proper documentation, a profound understanding of local tax laws, and seeking professional advice are indispensable for businesses navigating these changes effectively.

解读《2023 年财政(第 2 号)法案》的影响: 外国税收定义的重要修订

马来西亚《2023 年财政(第 2 号)法案》已正式公布,该法案长达 231 页,涉及税收各方面的重要修正案。

其中值得注意的修改包括对 《1967 年所得税法》第 2 条的修改,特别是对 “外国税 “定义的修改。

关键修正案: 重新定义 “外国税

拟议的修改强调,外国税应根据收入产生的地区来确定。作为企业,在处理国际收入和税款计算时,有必要采用战略性的细致方法。

企业的考虑因素:

1) 收入来源的具体性:

企业必须一丝不苟地确定收入并将其准确归属于产生收入的外国地区。这种精确性是根据修订后的定义计算适用的 “外国税 “的基础。

2) 审查税收管辖权规则:

在多个外国地区运营的公司(跨国企业)应全面审查每个国家的税收管辖规则。了解收入在这些司法管辖区的征税方式,对于使税收计算与修订建议保持一致至关重要。

3) 文件和记录保存:

详尽的文件和记录保存方法是不容商量的。企业需要保存与在外国地区创造收入有关的详细记录,包括交易的具体情况、收入来源和支付的相关税款。

4) 咨询税务专业人士:

鉴于国际税务问题错综复杂,强烈建议企业聘请专门从事跨境税务的税务专业人士。他们的专业知识将指导企业根据具体情况解释和应用修订后的定义。

5) 对税负的影响:

评估拟议修正案如何影响马来西亚的整体税负至关重要。明确外国税收与收入产生地有关可能会影响外国税收抵免或豁免的计算。

6) 随时了解变化:

税法是动态的,会不断更新和变化。随时了解与修订定义相关的额外指导或变更至关重要。建议定期查看税务机关的更新信息。

从本质上讲,重点在于使税收计算与产生收入的特定外国地区保持一致。适当的文件记录、对当地税法的深刻理解以及寻求专业建议是企业有效驾驭这些变化所不可或缺的。

Related-Article:

Finance (No.2) Bill 2023 – https://www.ccs-co.com/post/finance-no-2-bill-2023

Finance (No. 2) Bill 2023: Amendment of section 2 – https://www.ccs-co.com/post/finance-no-2-bill-2023-amendment-of-section-2