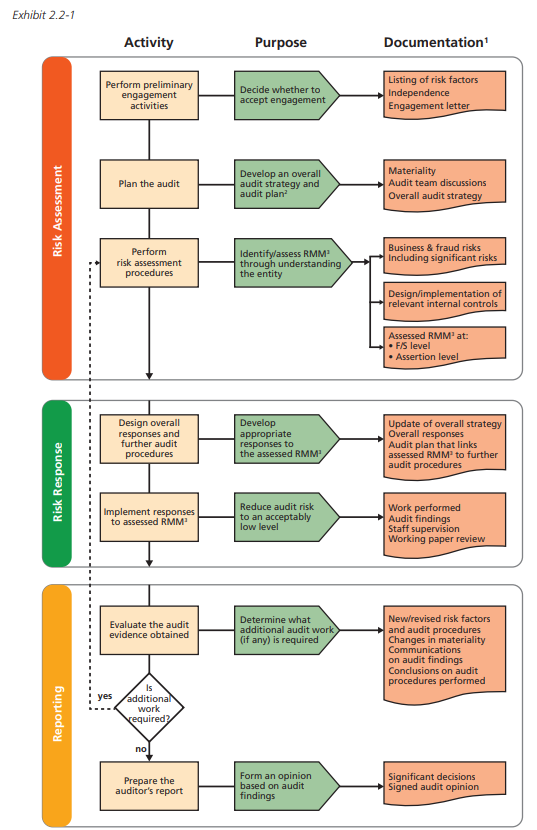

The audit approach outlined in Guide to Using International Standards on Auditing in the Audits of Small- and Medium-Sized Entities (the Guide) has been divided into:

- risk assessment,

- risk response, and

- reporting.

This is illustrated in Exhibit 2.2-1 in the Guide.

Notes: 1. Refer to ISA 230 for a complete list of documentation required. 2. Planning (ISA 300) is a continual and iterative process throughout the audit. 3. RMM = Risks of material misstatement.

The exhibit outlines the major activities, their purpose, and the documentation for each audit phase.

Additional information on the activities and documentation required in each of the three phases is outlined throughout the Guide, particularly in Volume 2, which follows a typical audit from start to finish.

审计风险评估程序 [Risk Assessment Procedures]

ISA 315 概述了审计师应该遵循的程序,以便用来进行审计风险评估,审计师在制定审计计划时必须考虑这些风险。ISA 315 要求审计师应执行风险评估程序,为判定和评估报表层次重大错报和判定层次重大错报提供依据。ISA 315确认以下三种风险评估程序:

询问管理层以及其他工作人员

审计人员必须与客户的管理层讨论审计的目标和期望,以及实现这些目标的计划。

分析性复核

分析性复核有助于审计师识别不同寻常的交易,帮助审计师发现一些未察觉到的地方,从而帮助风险评估,以便为设计和执行对风险的反应提供基础。

观察和检查

通过观察和检查可以获得关于客户和它所在环境的相关信息。相关例子可能涉及非常广泛的领域,包括观察和检查公司的经营,文件,管理层报告,公司的经营场所,机器设备等等。

ISA 315 要求风险评估程序至少应包含上述三种程序,并且还要求审计业务合伙人和其团队成员应对客户财报容易出现重大错报的可能性进行讨论。审计过程中任何阶段都可以确定重大风险,ISA 315 要求审计合伙人也应将这些事项传达给没有参与讨论团队成员。

对于评估的风险的回应 [Responses to Assessed Risks]

ISA 330 给出指导:根据风险评估结果,指导所需测试的性质和范围。

Audit Risk (AR) = Inherent Risk (IR) + Control Risk (CR) + Detection Risk (DR)

其中:

- AR 是指财务报表在审计前存在重大错报或漏报,而审计人员审计后发表不恰当审计意见的可能性;

- IR 是指会计报表存在重大错报或漏报,而审计人员审计后发表不恰当审计意见的可能性,无论该错报单独考虑,还是连同其他错报构成重大错报;

- CR 是指某项认定发生了重大错报,无论该错报单独考虑还是连同其他错报构成重大错报,而该错报没有被企业的内部控制及时防止、发现和纠正的可能性;

- DR 是指某一认定存在错报,该错报单独或连同其他错报是重大的,但审计师未能发现这种错报的可能性。

Inherent Risk

固有风险是指在不考虑内部控制结构的前提下,由于内部因素和客观环境的影响,企业的账户、交易类别和整体财务报表发生重大错误的可能性。固有风险是被审计单位经营过程中所固有的风险,审计师可以通过获取相关的信息,来评价被审计单位的固有风险,确定其对终极审计风险的影响。

Control Risk

控制风险是指被审计单位的业务和相应的会计处理发生重大错弊不能被内部控制防止和纠正的可能性。被审计单位建立内部控制的主要目的之一就是要防止错误和舞弊。如果被审计单位的内部控制制度存在重要的缺陷或者不能有效地工作,那么错误和舞弊就会进入被审计单位的财务报表系统,由此产生了控制风险。

Detection Risk

检查风险指审计师未能发现被审计单位会计报表上存在的某项重大错报或漏报可能性。

Our website's articles, templates, and material are solely for you to look over. Although we make every effort to keep the information up to date and accurate, we make no representations or warranties of any kind, either express or implied, regarding the website or the information, articles, templates, or related graphics that are contained on the website in terms of its completeness, accuracy, reliability, suitability, or availability. Therefore, any reliance on such information is strictly at your own risk.

Keep in touch with us so that you can receive timely updates |

要获得即时更新,请与我们保持联系

1. Website ✍️ https://www.ccs-co.com/ 2. Telegram ✍️ http://bit.ly/YourAuditor 3. Facebooks ✍

- https://www.facebook.com/YourHRAdvisory/?ref=pages_you_manage

- https://www.facebook.com/YourAuditor/?ref=pages_you_manage

4. Blog ✍ https://lnkd.in/e-Pu8_G 5. Google ✍ https://lnkd.in/ehZE6mxy

6. LinkedIn ✍ https://www.linkedin.com/company/74734209/admin/