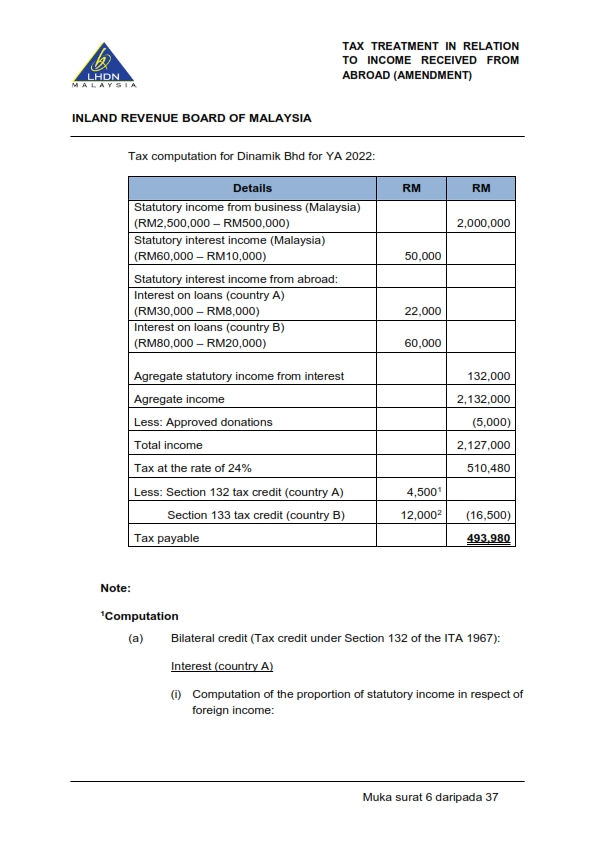

According to the Finance Act 2021, the income tax exemption on foreign-sourced income (FSI) received by any person (other than a resident company carrying on the business of banking, insurance, or sea or air transport) will be removed for all Malaysian-resident taxpayers beginning on January 1, 2022.

As a result of this:

- A flat income tax rate of 3% applies to the gross amount of FSI received in Malaysia between 1 January 2022 and 30 June 2022.

- Starting from 1 July 2022, the prevailing tax rate of the taxpayer applies to FSI received in Malaysia by Malaysian residents.

Exemption Orders Certain types of foreign-sourced income (FSI) for resident taxpayers will remain tax-exempt, as provided for in the following Orders gazetted on 19 July 2022, :

The Orders are effective from 1 January 2022 to 31 December 2026.

Both Orders emphasise that to be eligible for the tax exemption; the concerned taxpayers must adhere to the terms and conditions specified by the Ministry of Finance (MoF) as stated in the guidelines provided by the Inland Revenue Board (IRB).

These guidelines were issued on 29 September 2022. However, revisions to the Treatment Guidelines Tax Related to Income Received from Abroad were published on the HASiL Official Portal on December 29, 2022, while the guidelines dated September 29, 2022, are null and void. Media Release

On December 30, 2022, HASiL issued a media release titled “Tambahan syarat kelayakan pengecualian cukai bagi pendapatan dividen luar negara yang diterima di Malaysia mulai 1 Januari 2022 hingga 31 Disember 2026,” which pertains to the aforementioned revised guideline.

The release includes examples of economic substance in item 5 on pages 2 and 3.

Item 7 on page 3 of the release stipulates that for the Income Tax Return Form (ITRF) filed on or before December 29, 2022, taxpayers must file a modified ITRF if they fail to meet the economic substance conditions for dividend income received in Malaysia from abroad. No penalty will be levied.

The amended guideline includes changes in the following paragraphs:

Please access the Guideline for the full details.

Reference

10. HASiL – Technical Guideline on Tax Treatment in Relation to Income received from Abroad (Amendment)

10.1 Media Release – Tambahan syarat kelayakan pengecualian cukai bagi pendapatan dividen luar negara yang diterima di Malaysia mulai 1 Januari 2022 hingga 31 Disember 2026

10.2 HASiL – Technical Guidelines on Tax Treatment in relation to Income which is received from Abroad (29 Sep 2022)

10.3 P.U. (A) 234_2022 – Income Tax (Exemption) (No. 5) Order 2022

10.4 P.U. (A) 235_2022 – Income Tax (Exemption) (No. 6) Order 2022

5 games to keep employees of CCS & Co Plt – Chartered Accountants and Bispoint Group of Accountants connected.

We put a lot of emphasis on ensuring that our team members enjoy a balanced life outside work.

Hence, our firm’s Sports and Social Committee is responsible for actively organising an exciting variety of events, such as the Annual Dinner, Annual Trips and Inter-accounting Firm Tournament.

These events are planned so that our professionals can take some time off to relax and, more importantly, come together to strengthen their sense of community and teamwork.

This year’s Inter-Accounting Firm Tournament will be held on February 25 and 26, 2023 (Saturday and Sunday). We welcome your support!

5项活动让 CCS 特许会计师 和 Bispoint Group of Accountants 的员工保持联系。

我们非常重视我们的团队成员享受工作以外的平衡生活。

有鉴于此,我们公司的康乐委员会积极举办各种令人兴奋的活动,如年度晚宴、年度旅行和会计师事务所之间的比赛。

这些活动的策划是为了让我们的专业人员可以抽出一些时间来放松,更重要的是,他们可以聚在一起加强社区意识和团队精神。

今年的会计师事务所之间的比赛将于2023年2月25日和26日(星期六和星期日)举行。我们欢迎你前来支持!

Our website's articles, templates, and material are solely for you to look over. Although we make every effort to keep the information up to date and accurate, we make no representations or warranties of any kind, either express or implied, regarding the website or the information, articles, templates, or related graphics that are contained on the website in terms of its completeness, accuracy, reliability, suitability, or availability. Therefore, any reliance on such information is strictly at your own risk.

Keep in touch with us so that you can receive timely updates |

要获得即时更新,请与我们保持联系

1. Website ✍️ https://www.ccs-co.com/ 2. Telegram ✍️ http://bit.ly/YourAuditor 3. Facebook ✍

- https://www.facebook.com/YourHRAdvisory/?ref=pages_you_manage

- https://www.facebook.com/YourAuditor/?ref=pages_you_manage

4. Blog ✍ https://lnkd.in/e-Pu8_G 5. Google ✍ https://lnkd.in/ehZE6mxy

6. LinkedIn ✍ https://www.linkedin.com/company/74734209/admin/