“Section 81 – Review And Appeal” is read as follows:-

81(1) [Application for review]

Any person aggrieved by any decision of the Director General may apply to the Director General for review of any of his decision within thirty days from the date the person has been notified of such decision provided that no appeal has been made on the same decision to the Customs Appeal Tribunal or court.

81(2) [Prescribed form]

An application for review under subsection (1) shall be made in the prescribed form.

81(3) [Notification of decision]

Where an application for review has been made under subsection (1), the Director General shall make the review and notify the decision of the review to the person, where practicable, within sixty days from the date of the receipt of such application.

81(4) [Matters relating to compound]

No review may be made in any matter relating to compound.

81(5) [Appeal against Director General’s decision]

Any person aggrieved by any decision of the Director General under subsection (3) or any other provision of this Act, except any matter relating to compound, may appeal to the Customs Appeal Tribunal in writing within thirty days from the date of notification of the decision to the aggrieved person.

81(6) [Tax payable notwithstanding review or appeal]

Any service tax due and payable under this Act shall be paid notwithstanding any review or appeal has been made under this section.

81(7) [Exception to foreign registered person]

This section shall not apply to a foreign registered person.

Finance (No. 2) Bill 2023

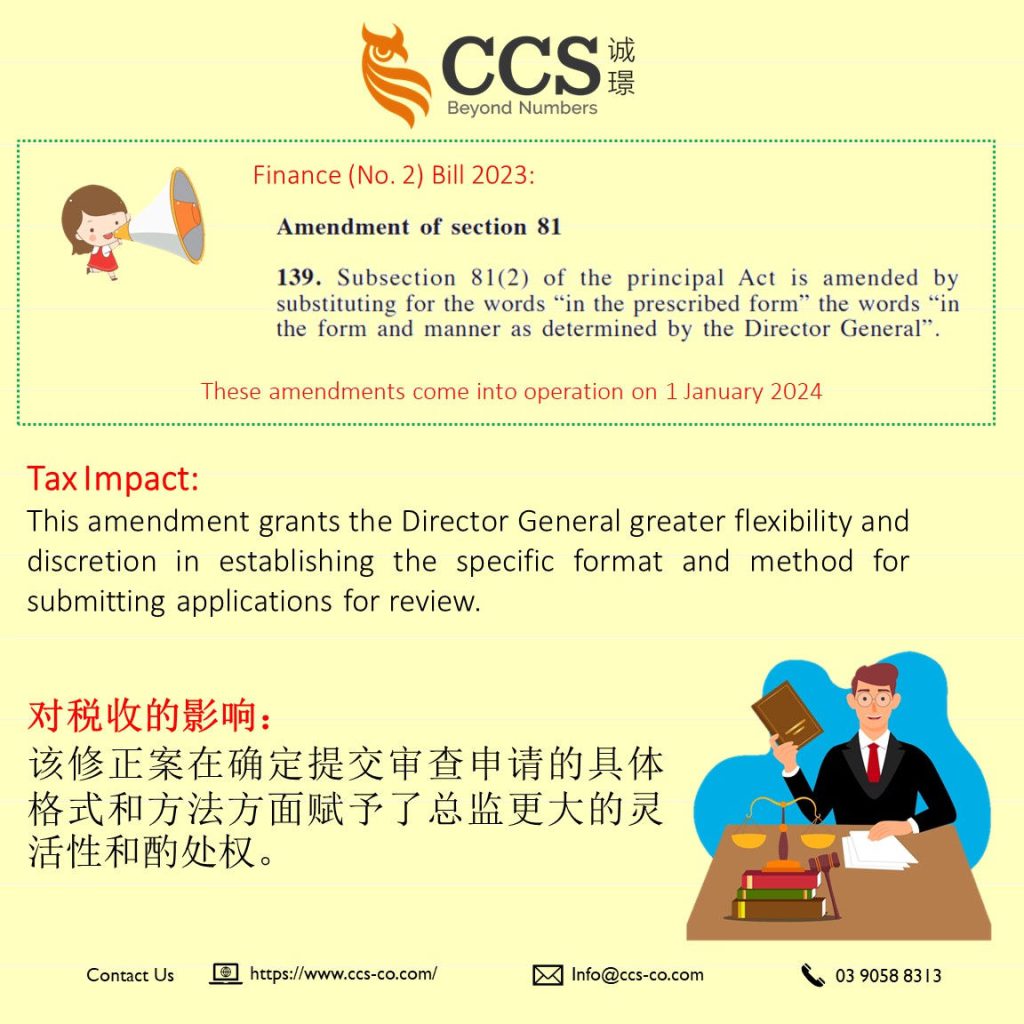

The Finance (No. 2) Bill 2023 proposes a crucial amendment to Section 81 of the Service Tax Act 2018, specifically focusing on the application process for review of decisions made by the Director General.

Currently, according to Section 81(2), an application for review must be made “in the prescribed form.”

The proposed amendment seeks to replace this requirement “in the form and manner as determined by the Director General.”

This amendment grants the Director General greater flexibility and discretion in establishing the specific format and method for submitting applications for review.

By empowering the Director General to determine the form and manner, the amendment aims to enhance procedural adaptability, potentially streamlining the application process and aligning it more closely with the evolving needs of the regulatory framework.

The impact of this change lies in facilitating a more responsive and efficient review process for individuals aggrieved by the decisions of the Director General, fostering a dynamic approach to regulatory procedures in the realm of service tax.