“Section 75 – Transaction Of Business On Behalf Of Any Person” is read as follows:-

75(1) [Transaction on behalf of taxable person]

Subject to section 74, no person shall transact any business in relation to this Act on behalf of any taxable person, or any person other than a taxable person who, in carrying on his business, acquires any imported taxable service, or any foreign registered person except on matters with regard to any refund, remission, exemption, or any other matters as approved by the Director General, under this Act.

75(2) [Letter of authorisation and prescribed form]

The person who transacts business on any of the matters stated in subsection (1) on behalf of the person referred to in that subsection shall—

- produce a letter of authorisation from the person whom he represents; and

- where any prescribed form is required to be submitted for the purposes of the matters being transacted, submit the form that has been signed by the person, except where otherwise allowed by a senior officer of service tax.

75(3) [Offence]

Any person who contravenes subsection (1) commits an offence.

Finance (No. 2) Bill 2023

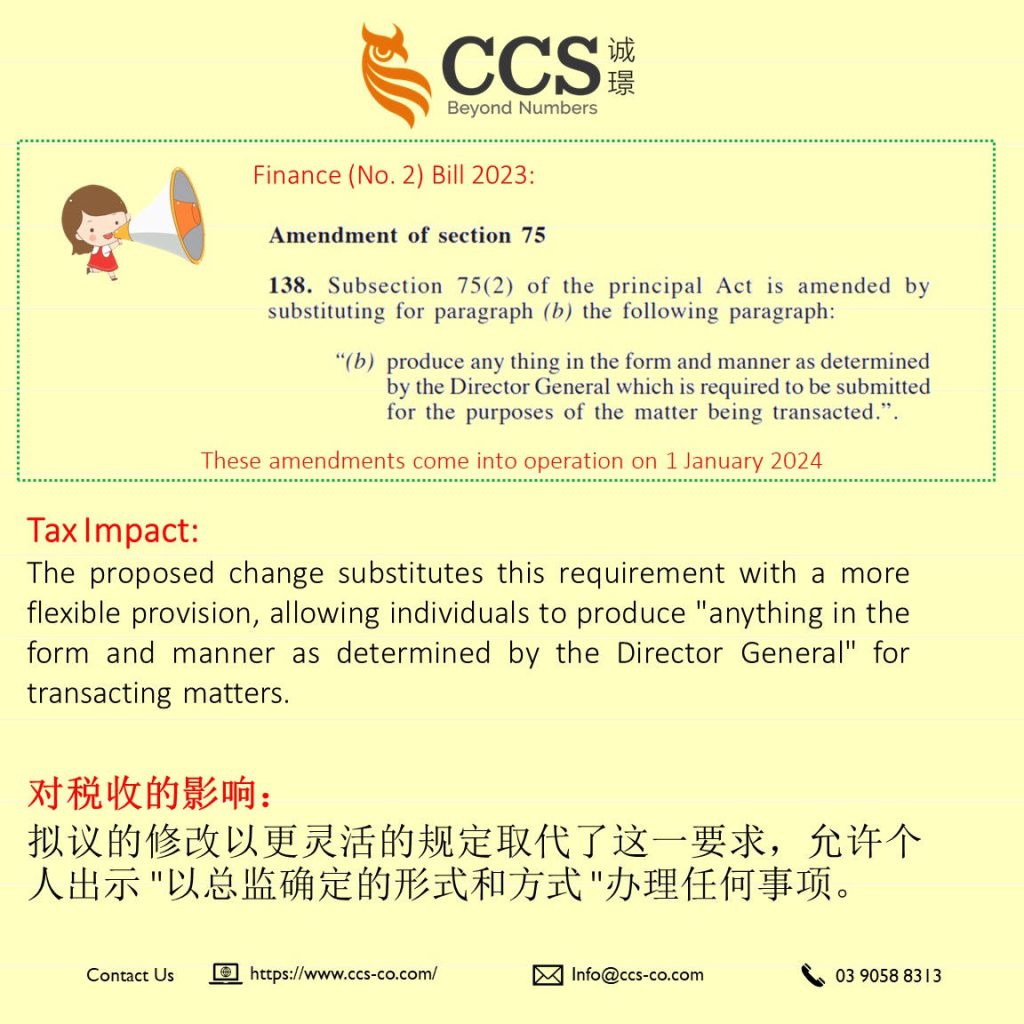

The proposed amendment to Section 75 of the Service Tax Act 2018, as outlined in the Finance (No. 2) Bill 2023, focuses on enhancing the procedural requirements for individuals transacting business on behalf of taxable persons under the Act.

Section 75 regulates the authorisation and submission of necessary documentation when conducting transactions related to the Act.

The amendment specifically targets subsection 75(2)(b), where the current provision requires the submission of a form signed by the represented person.

The proposed change substitutes this requirement with a more flexible provision, allowing individuals to produce “anything in the form and manner as determined by the Director General” for transacting matters.

This amendment grants the Director General greater authority to specify the format and content of the documentation required for transactions, thereby offering increased adaptability in regulatory procedures.

The impact of this amendment lies in promoting a more dynamic and responsive approach to documentation standards, potentially streamlining processes and improving the efficiency of business transactions conducted on behalf of taxable persons.