“Sections 56C – application for registration of foreign service provider” is read as follows:-

56C(1) Any foreign service provider who is liable to be registered under subsection 56B(2) shall apply to the Director General for registration in the prescribed form not later than the last day of the month following the month in which he is liable to be registered as referred in paragraph 56B(2)(a) or (b).

56C(2) Upon receipt of the application under subsection (1), the Director General may approve the registration from such date as he may determine and subject to such conditions as he deems fit.

56C(3) The Director General shall register the foreign service provider under subsection (1) with effect from the first day of the month following the month in which the application under subsection (1) is made or from such earlier date as the Director General may determine but such date shall not be earlier than the date the foreign service provider becomes liable to be registered.

56C(4) Any foreign service provider who contravenes subsection (1) commits an offence and shall, on conviction, be liable to a fine not exceeding thirty thousand ringgit or to imprisonment for a term not exceeding two years or to both.

“Section 56H – taxable period and accounting for service tax” is read as follows:-

56H(1) [Determination of taxable period]

The taxable period for a foreign registered person shall be a period of three months ending on the last day of any month of any calendar year.

56H(2) [Application to vary taxable period]

A foreign registered person may apply in writing to the Director General for a taxable period other than the period as determined under subsection (1).

56H(3) [Director General’s decision]

The Director General may, upon receiving any application under subsection (2)—

- allow the application and the taxable period shall be the period as applied for;

- refuse the application and the taxable period shall remain as determined under subsection (1); or

- vary the length of the taxable period.

56H(4) [Furnishing of return]

A foreign registered person shall, in respect of his taxable period, account for the service tax due in a return as may be prescribed and the return shall be furnished to the Director General in the prescribed manner not later than the last day of the month following the end of his taxable period to which the return relates.

56H(4A)

A foreign registered person who ceases to be liable to be registered under section 56D shall furnish a return not later than thirty days or such later date containing particulars as the Director General may determine in respect of that part of the last taxable period during which the foreign registered person was registered.

56H(5) [Furnishing of return with varied taxable period]

Where a taxable period has been varied under paragraph (3)(c) and notwithstanding subsection (4), the return shall be furnished not later than the last day of the month following the end of the varied taxable period.

56H(6) [Furnishing of return regardless of tax amount]

The return referred to in subsections (4), (4A) and (5) shall be furnished whether or not there is service tax to be paid.

56H(7) [Offence and penalty]

Any foreign registered person who—

- contravenes subsection (4), (4A) or (5); or

- furnishes an incorrect return,

commits an offence and shall, on conviction, be liable to a fine not exceeding fifty thousand ringgit or to imprisonment for a term not exceeding three years or to both.

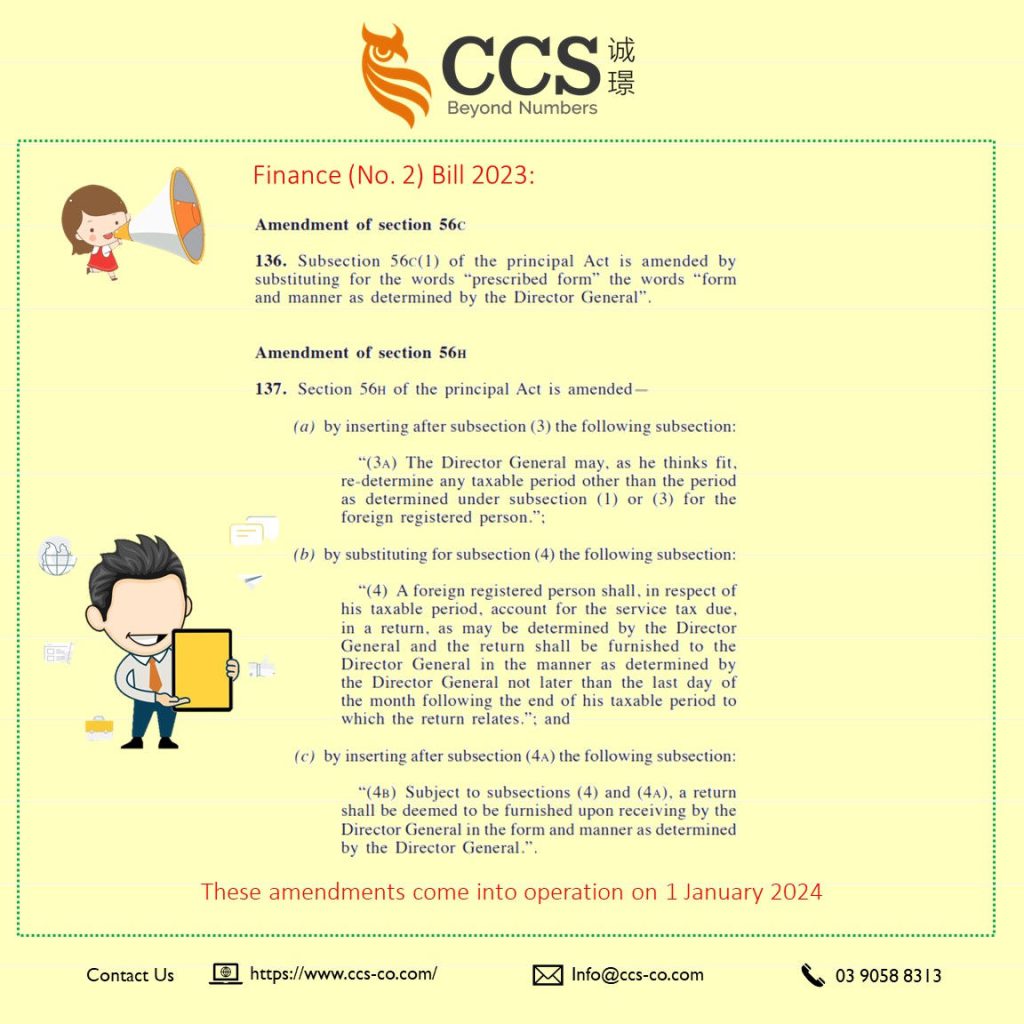

Finance (No. 2) Bill 2023

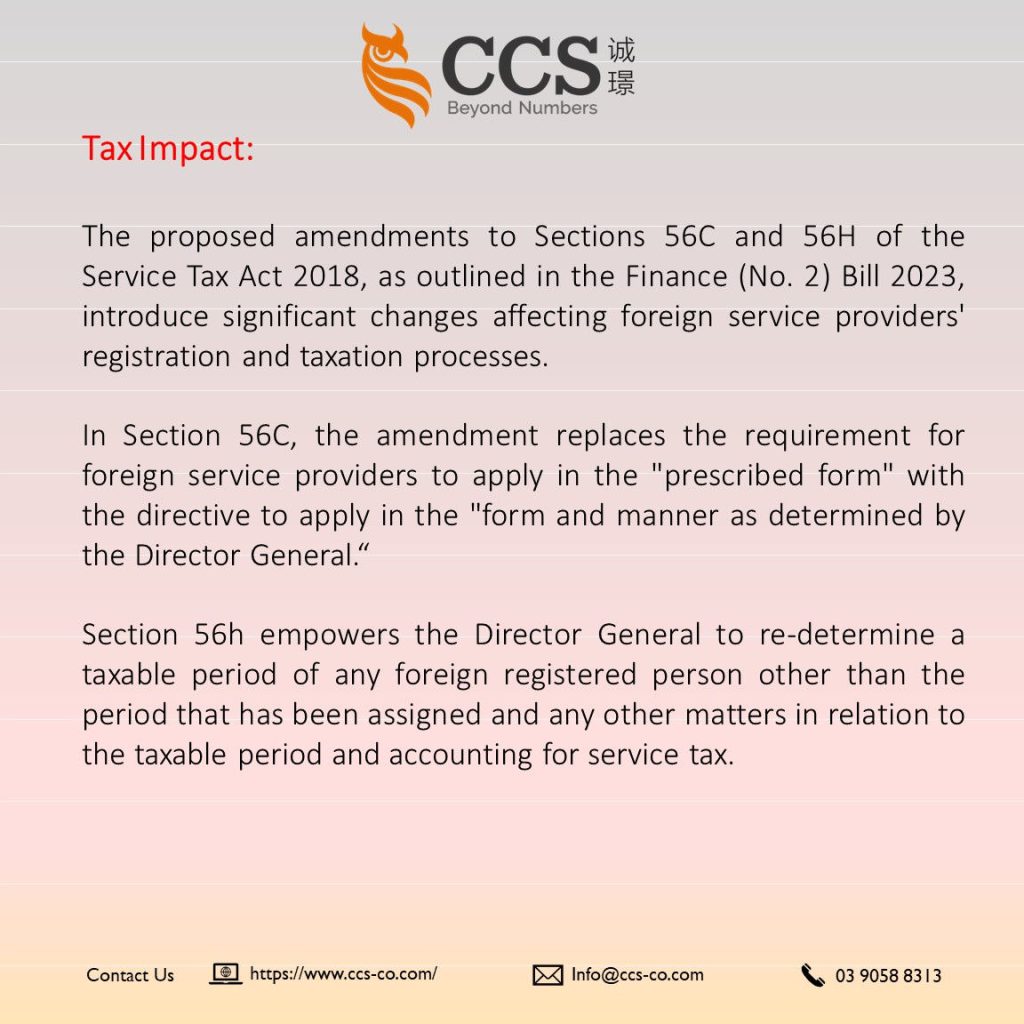

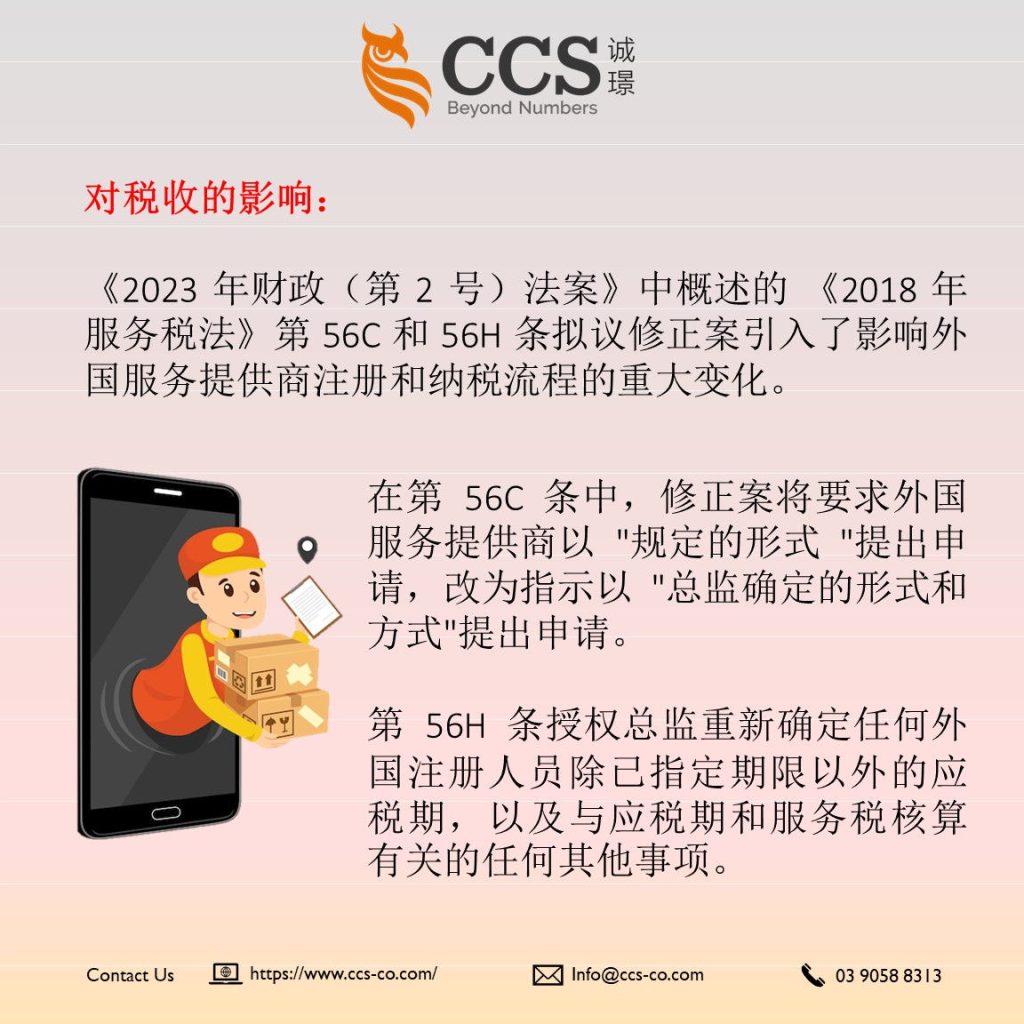

The proposed amendments to Sections 56C and 56H of the Service Tax Act 2018, as outlined in the Finance (No. 2) Bill 2023, introduce significant changes affecting foreign service providers’ registration and taxation processes.

In Section 56C, the amendment replaces the requirement for foreign service providers to apply in the “prescribed form” with the directive to apply in the “form and manner as determined by the Director General.”

This grants greater flexibility to the Director General in specifying the format for registration applications.

In Section 56H, several amendments are proposed.

Firstly, a new subsection (3A) empowers the Director General to re-determine taxable periods for foreign registered persons.

Secondly, subsection (4) is modified to emphasise that foreign registered persons must account for service tax “as determined by the Director General” and furnish returns in the manner specified by the Director General.

Lastly, subsection (4B) clarifies that a return is deemed furnished upon receipt by the Director General in the specified form and manner.

These changes provide the Director General with enhanced authority in determining taxable periods and regulating the process of tax accounting and return submission for foreign registered persons.

The impact of these amendments lies in streamlining procedures, ensuring compliance, and offering the Director General greater control over the regulatory framework for foreign service providers, thereby contributing to more effective tax administration.