“Section 38 – Refund of Service Tax, etc., Overpaid or Erroneously Paid” is read as follows:-

38(1) [Claim for refund]

Any person who—

- has overpaid or erroneously paid any service tax, surcharge, penalty, fee or other money; or

- is entitled to the refund under subsection 34(6) or 40(3),

may make a claim for refund in the prescribed form.

38(2) [Timeframe]

A claim for refund under subsection (1) shall be made to the Director General within one year from the time—

- such overpayment or erroneous payment occurred; or

- such entitlement of the refund under subsection 34(6) or 40(3) occurred.

38(3) [Director General may make refund]

The Director General may make such refund in respect of the claim under subsection (1) after being satisfied that the person has properly established the claim.

38(4) [Reduction or disallowance of tax refund]

The Director General may reduce or disallow any refund due in respect of the claim under subsection (1) to the extent that the refund would unjustly enrich the person referred to in subsection (1).

38(5) [Evidence]

A claim for refund under this section shall be supported by such evidence as required by the Director General.

“Section 39 – Deduction from Return of Refunded Service Tax” is read as follows:-

39(1) [Deduction from return of refunded tax]

The Director General may approve, subject to such conditions as he deems fit, an application by any registered person to deduct from time to time from his return referred to in section 26 the amount of service tax paid but subsequently refunded to his customer by reason of—

- cancellation of taxable service;

- termination of taxable service; or

- such other reasons as may be approved by the Director General.

39(2) [Timeframe]

The registered person shall make the deduction referred to in subsection (1) within one year after the payment was made, or such extended period as may be approved by the Director General.

39(3) [Exception to foreign registered person]

This section shall not apply to a foreign registered person.

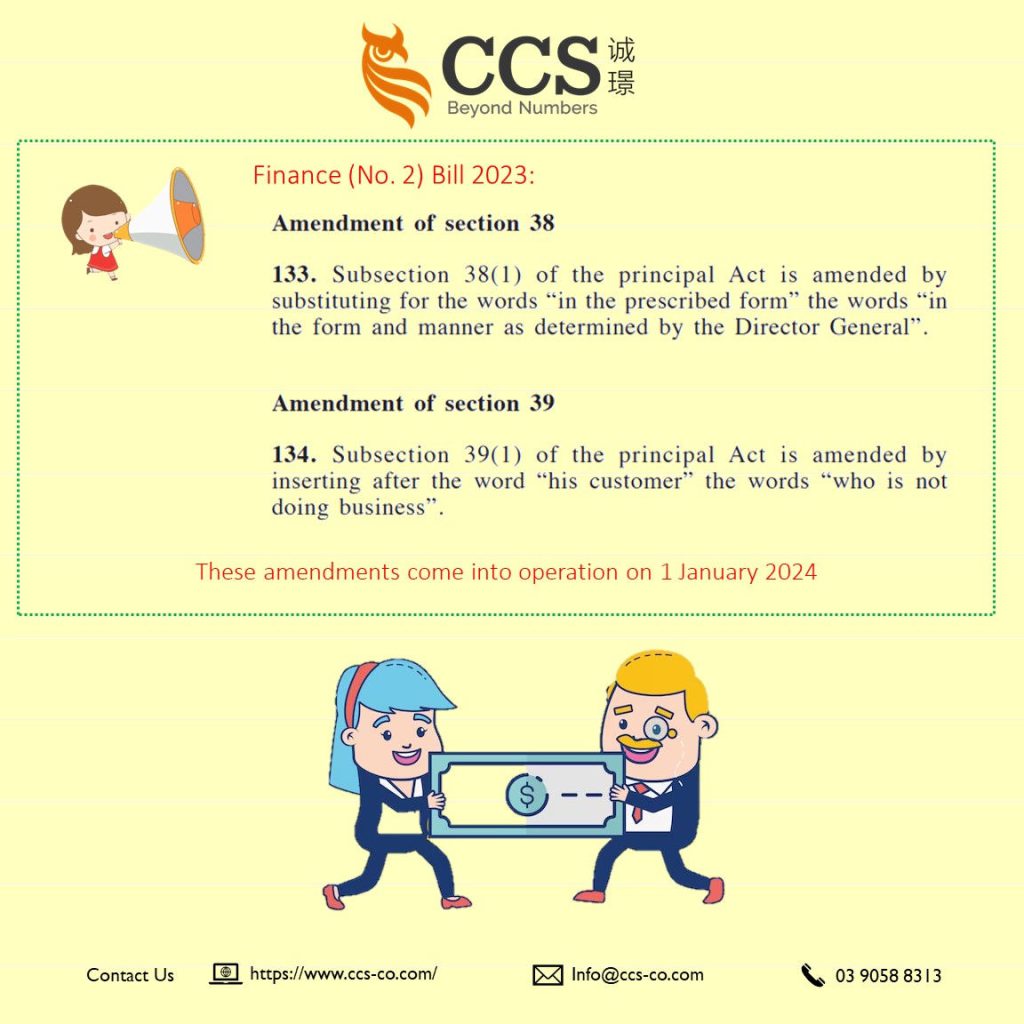

Finance (No. 2) Bill 2023

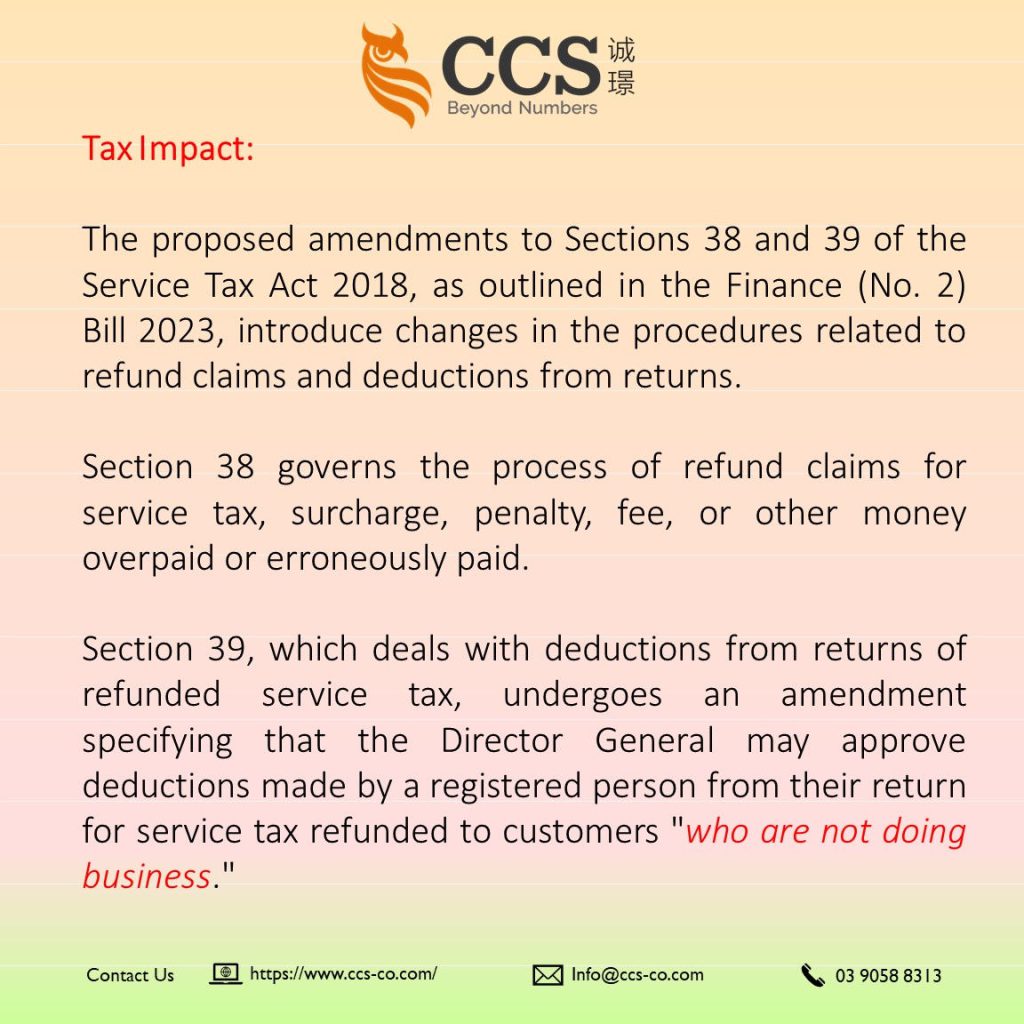

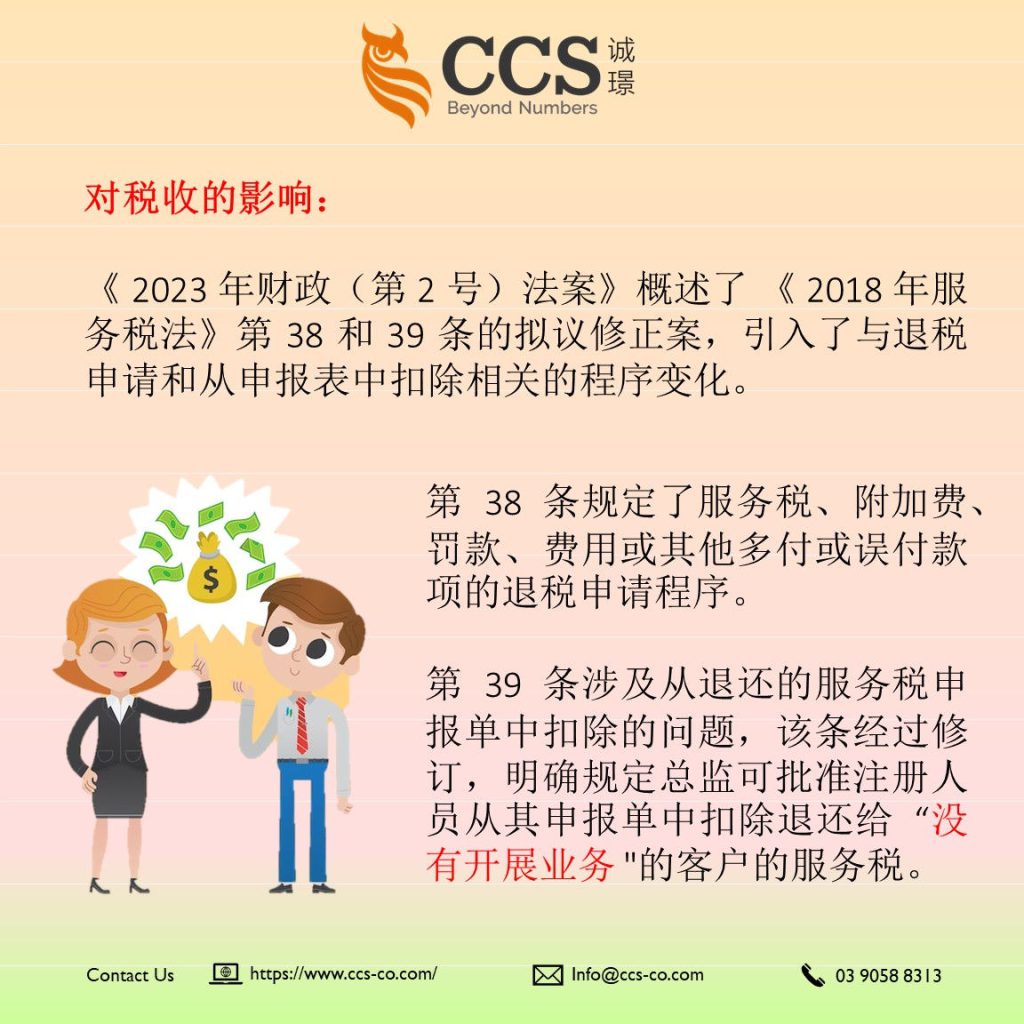

The proposed amendments to Sections 38 and 39 of the Service Tax Act 2018, as outlined in the Finance (No. 2) Bill 2023, introduce changes in the procedures related to refund claims and deductions from returns.

Section 38 governs the process of refund claims for service tax, surcharge, penalty, fee, or other money overpaid or erroneously paid.

The amendment emphasises the necessity for such claims to be made “in the form and manner as determined by the Director General,” providing the Director General with the authority to define specific requirements for the submission of refund claims.

Section 39, which deals with deductions from returns of refunded service tax, undergoes an amendment specifying that the Director General may approve deductions made by a registered person from their return for service tax refunded to customers “who are not doing business.”

This amendment introduces a condition that restricts the approval of deductions to customers not engaged in business activities.

These amendments aim to enhance clarity and precision in the refund and deduction processes, potentially impacting the eligibility criteria for deductions and ensuring a more streamlined compliance framework.