Before we get into the details of paragraph 7, let’s first understand the context of these income tax exemption orders.

The orders, namely P.U. (A) 161/2019, 162/2019, and 163/2019, were gazetted on 7th June 2019. They provide income tax exemptions for companies that promote exporting certain manufactured products and agricultural produce.

Now, let’s focus on paragraph 7 of these orders. Paragraph 7 introduces the concept of separate sources and separate accounts for qualifying companies engaged in activities related to exporting agricultural produce or products from manufacturing.

Separate Source

According to subparagraph (1) of paragraph 7, when a qualifying company carries out multiple activities, such as exporting agricultural produce or products from manufacturing and other unrelated activities, each activity is treated as a separate and distinct source of income.

In other words, the income generated from each activity is considered independent of each other for tax purposes. This separation helps maintain clarity and transparency in the company’s financial records.

Separate Account

In subparagraph 7(2), a qualifying company granted an exemption under paragraph 3 of the orders must maintain a separate account for the income derived from each activity mentioned in subparagraph (1).

By maintaining separate accounts, companies can ensure that the income from each activity is accurately tracked and reported.

This allows for better monitoring, auditing, and compliance with the income tax regulations.

Questions

On maintaining a separate account for income derived from each activity referred to in paragraph 7(1), i.e., activity related to the export of agricultural produce or product from manufacturing and other activity:

- What is meant by ‘each activity;

- If a company manufactures and exports Product A and Product B, is the export of Products A and B treated as two separate activities?

- If the company ceases the production of Product A in year 2, does the company still need to maintain separate accounts for Product A? Would the exemption for the export of Product A that could not be granted or could not be granted in full in year 1 due to insufficiency of statutory income be disregarded in year 2?

PU. A 161/2019

A separate account means preparing accounts based on the category of exported activities/products and non-exported activities/products.

This condition does not mean preparing separate accounts for each exported product.

Therefore, preparing accounts based on this category still needs to be maintained even if the company no longer produces Product A.

PU A 162/2019 and P.U A 163/2019

A separate account means preparing separate accounts for each exported product to determine the value added of each product to meet the requirements in paragraph 4(1)(a).

If, in part of the second year, Product A is still produced, separate accounts need to be prepared.

However, if there is no production of Product A in the second year, separate accounts do not need to be prepared.

However, any amount of exception for Product A that cannot be absorbed will be disregarded in both scenarios.

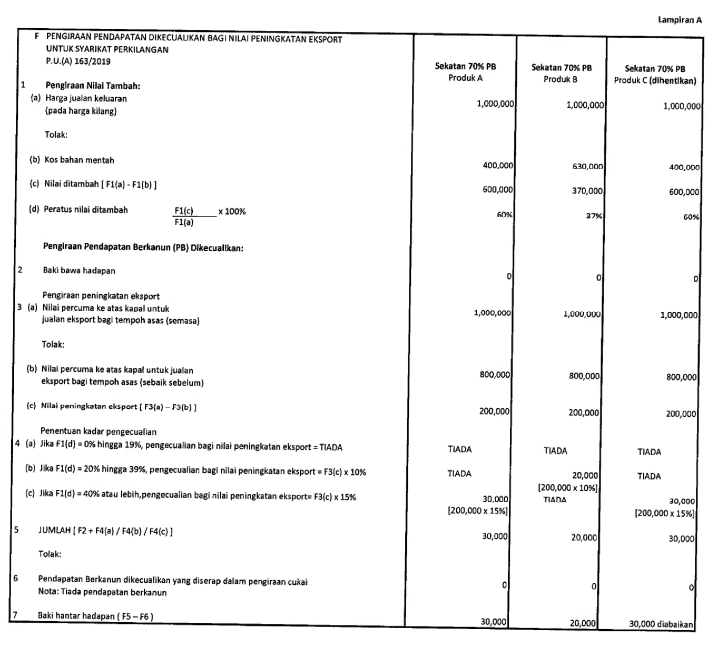

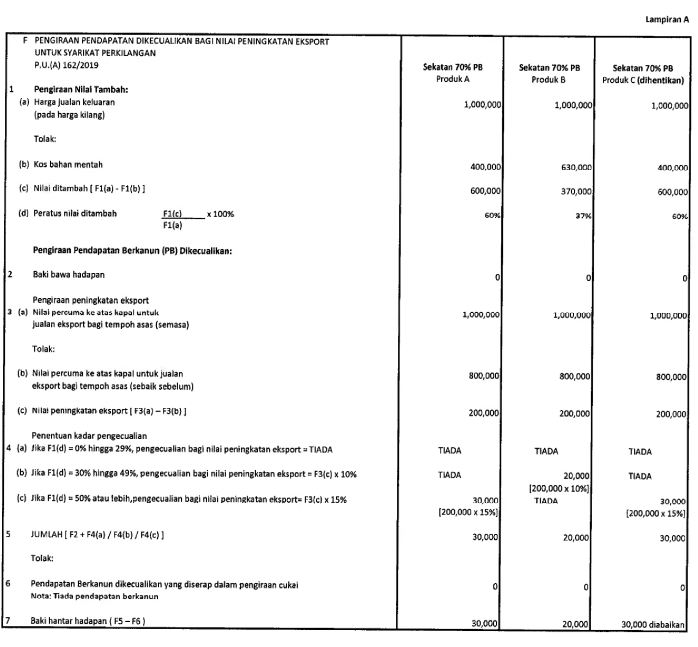

Calculation Example

Please refer to Appendix A for calculation examples under P.U.(A) 162/2019 and P.U.(A) 163/2019.

CONCLUSION

And there you have it!

The purpose of paragraph 7 of the P.U. (A) 161/2019, 162/2019, and 163/2019 is to establish separate and distinct sources of income for qualifying companies engaged in activities related to the export of agricultural produce or products from manufacturing.

Additionally, these companies are required to maintain separate accounts for the income derived from each activity.

References:-

P.U. (A) 161/2019

P.U. (A) 162/2019

P.U. (A) 163/2019

Disclaimer:

The articles, templates, and other materials on our website are provided only for your reference.

While we strive to ensure that the information presented is current and accurate, we cannot guarantee the completeness, reliability, suitability, or availability of the website or its content, including any related graphics. Consequently, any reliance on this information is entirely at your own risk.

If you intend to use the content of our videos and publications as a reference, we recommend that you take the following steps:

- Verify that the information provided is current, accurate, and complete.

- Seek additional professional opinions, as the scope and extent of each issue, may be unique.

免责声明:

我们网站上的文章、模板和其他材料只供参考。

虽然我们努力确保所提供的信息是最新和准确的,但我们不能保证网站或其内容,包括任何相关图形的完整性、可靠性、适用性或可用性。因此,您需要承担使用这些信息所带来的风险。

如果你打算使用我们的视频和出版物的内容作为参考,我们建议你采取以下步骤:

- 核实所提供的信息是最新的、准确的和完整的。

- 寻求额外的专业意见,因为每个问题的范围和程度,可能是独特的。

Keep in touch with us so that you can receive timely updates

请与我们保持联系,以获得即时更新。

1. Website ✍️ https://www.ccs-co.com/ 2. Telegram ✍️ http://bit.ly/YourAuditor 3. Facebook ✍

- https://www.facebook.com/YourHRAdvisory/?ref=pages_you_manage

- https://www.facebook.com/YourAuditor/?ref=pages_you_manage

4. Blog ✍ https://lnkd.in/e-Pu8_G 5. Google ✍ https://lnkd.in/ehZE6mxy

6. LinkedIn ✍ https://www.linkedin.com/company/74734209/admin/