“Section 10 – Rate Of Sales Tax” is read as follows:-

Section 10(1) Sales tax shall be charged and levied at the rate fixed in accordance with subsection (2) on the low-value goods sold by reference to the sale value of the low-value goods as determined under section 9.

Section 10(2) The Minister may, by order published in the Gazette—

- fix the rate of sales tax to be charged and levied under this Act; and

- vary or amend the rate of sales tax fixed under paragraph (a).

Section 10(3) Any order made under subsection (2) shall—

- be laid before the Dewan Rakyat at the next meeting of the Dewan Rakyat; and

- at the expiration of one hundred and twenty days from being laid under paragraph (a) or of such extended period as the Dewan Rakyat may, by resolution, direct, cease to have effect in whole if the order is not confirmed, or in part in so far as the order is not confirmed, by a resolution passed by the Dewan Rakyat within the said one hundred and twenty days or, if such period has been extended, within such extended period.

Section 10(4) (Deleted by Act 806 of 2018, Sch. item 2)

Section 10(5) (Deleted by Act 806 of 2018, Sch. item 2)

Section 10(6) (Deleted by Act 806 of 2018, Sch. item 2)

Section 10 of the Sales Tax Act 2018 outlines how sales tax is determined and regulated.

- Charging Sales Tax: This section establishes that sales tax is applied to the sale of low-value goods. The amount of tax is based on the sale value of these goods, as determined by the guidelines set in section 9.

- Rate Fixing Authority: Through an official order published in the Gazette (an official government publication), the Minister has the authority to set the rate at which the sales tax is charged. This rate can be initially fixed, altered, or amended.

- Parliamentary Approval: Any changes to the sales tax rate made by the Minister must be presented to the Dewan Rakyat (the lower house of the Parliament of Malaysia) during its next meeting. If not confirmed by the Dewan Rakyat within 120 days (or any extended period they may decide), the order ceases to have effect.

- Repealed Sections: Some subsections (10(4), 10(5), and 10(6)) have been deleted as per the provisions of Act 806 of 2018.

In simpler terms, this section outlines the process of determining and adjusting the rate of sales tax on low-value goods. The Minister can set or change the rate, but Parliament must approve it within a specified time frame for the changes to be effective.

Finance (No. 2) Bill 2023

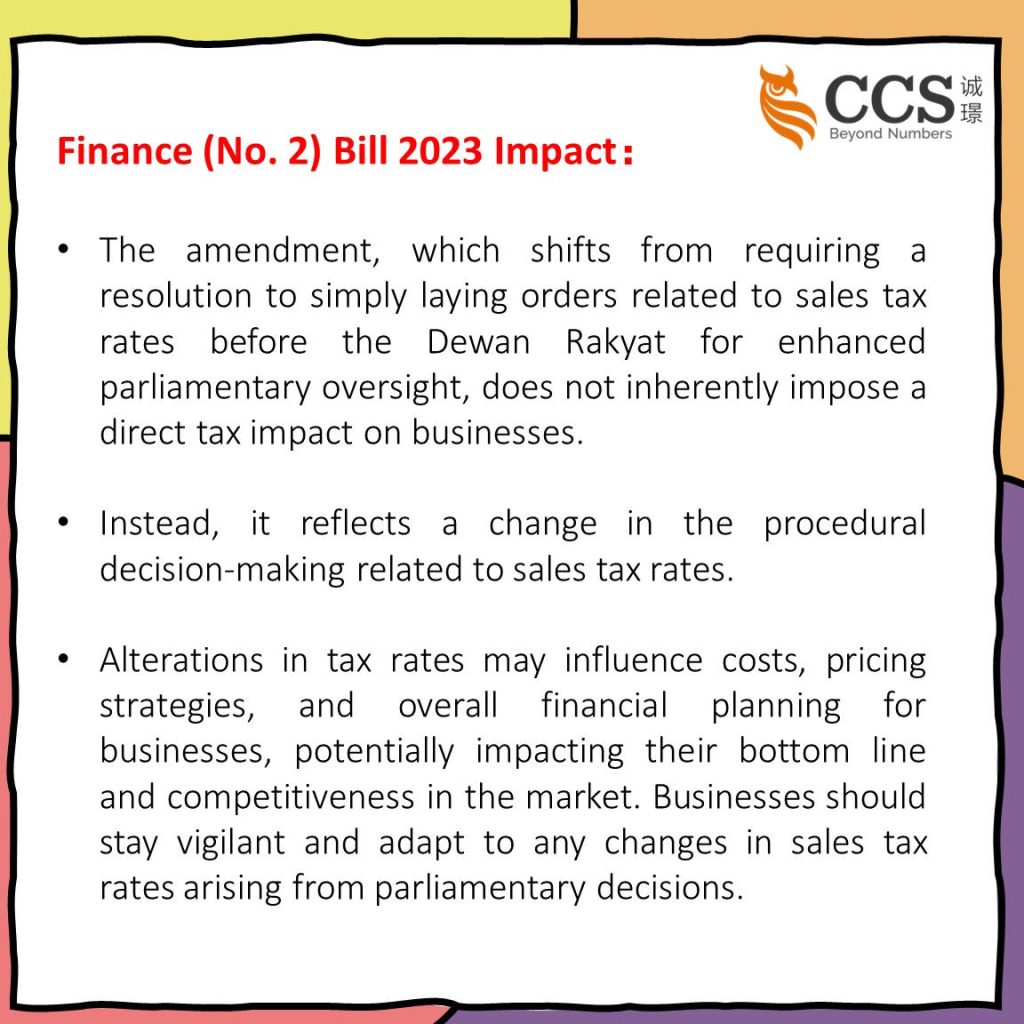

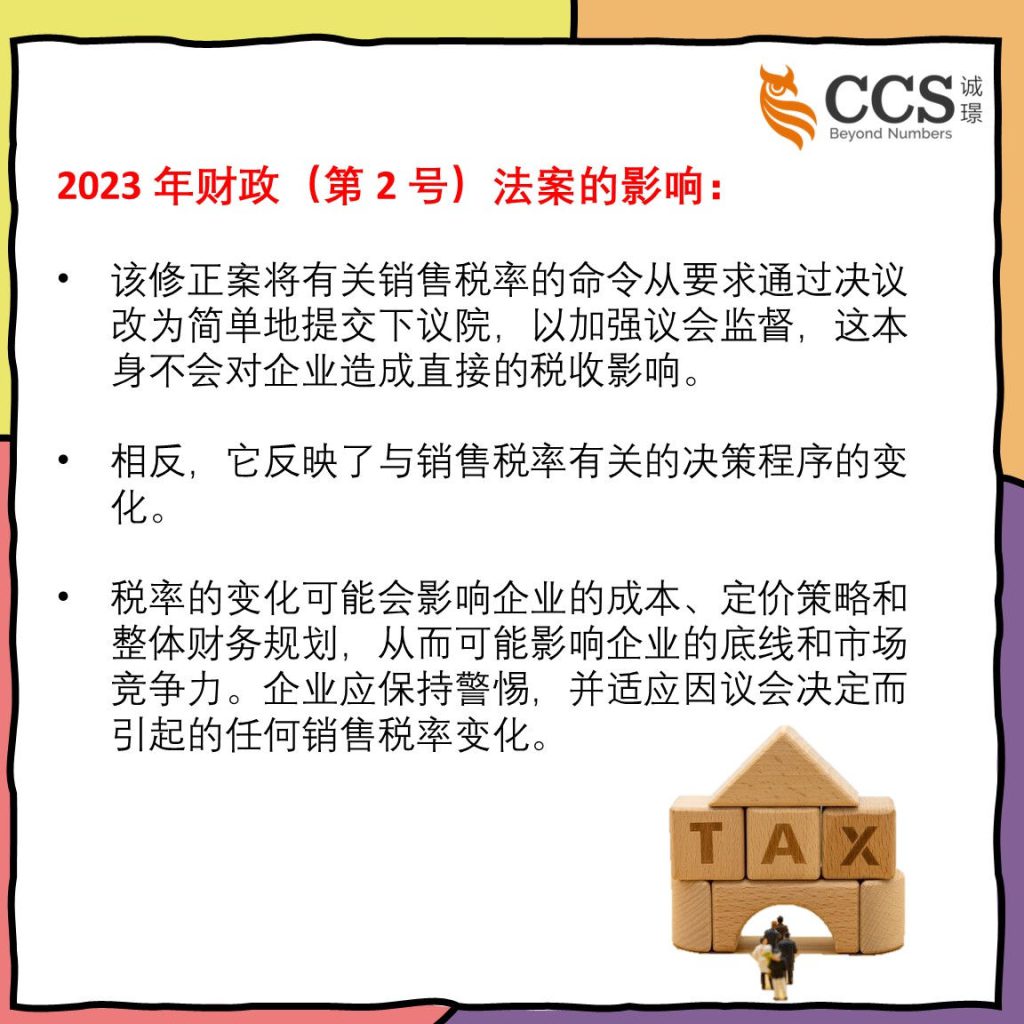

The proposed amendment to section 10 of the Sales Tax Act 2018, as outlined in the Finance (No. 2) Bill 2023, involves changes to the parliamentary approval process for orders related to the sales tax rate.

Here’s an explanation and potential tax impact:

Substitution of Subsection (3):

- Current Provision: Subsection (3) of section 10 requires any order made under subsection (2) (related to fixing or amending the sales tax rate) to be laid before the Dewan Rakyat (the lower house of the Parliament of Malaysia).

- Proposed Amendment: The amendment suggests substituting the existing subsection (3) with a new provision emphasising the requirement for laying the order before the Dewan Rakyat.

Deletion of Subsections (4), (5), and (6):

- Current Provisions: Subsections (4), (5), and (6) of section 10, which are being proposed for deletion, are likely related to provisions that have become obsolete or are no longer deemed necessary.

- Proposed Amendment: The amendment seeks to remove these subsections from the Sales Tax Act 2018.

Reason for Amendment:

- As stated in the amendment, the proposed changes are to replace the requirement of obtaining a resolution from the Dewan Rakyat for any order made under section 10 with the simpler requirement of laying the order before the Dewan Rakyat.

- This amendment streamlines the process for parliamentary approval by eliminating the need for a resolution.

Tax Impact:

- The direct tax impact of this amendment may not be substantial. Instead, it focuses on procedural changes in obtaining parliamentary approval for orders related to the sales tax rate.

- Streamlining the process could lead to quicker decision-making regarding sales tax rates, providing more flexibility for timely adjustments based on economic conditions.

Effective Date:

- The amendment specifies that these changes come into operation on the coming into effect of the Finance (No. 2) Act 2023.

In summary, the proposed changes aim to simplify the parliamentary approval process for orders related to the sales tax rate, with the potential benefit of increased efficiency in decision-making.