The Finance (No. 2) Bill 2023 introduces three new Sections—28A, 28B, and 28C—into the Real Property Gains Tax Act 1976.

These sections empower the Director General to gather specific information related to financial accounts and disposals of chargeable assets.

They also impose obligations on individuals to maintain and provide certain documents to determine chargeable gains and tax liabilities.

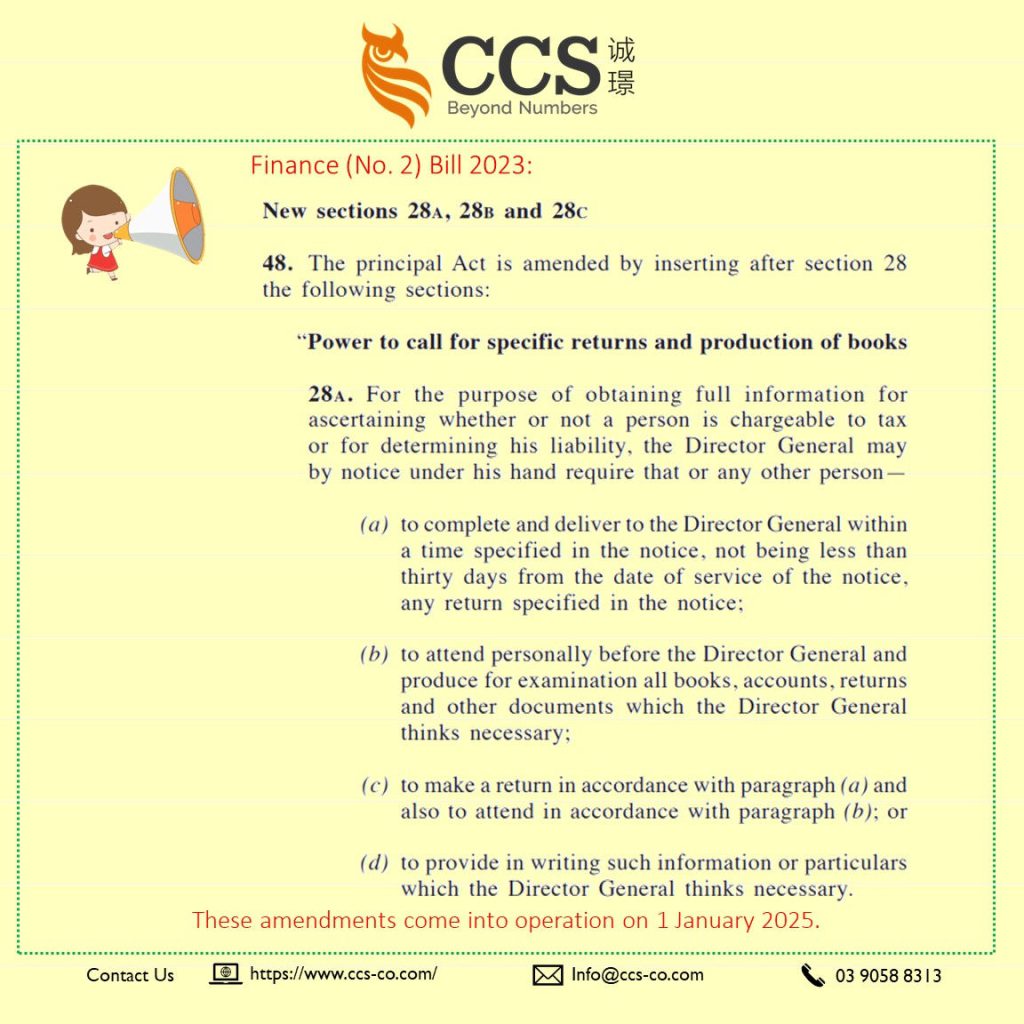

Section 28A is read as follows:-

“Power to call for specific returns and production of books”

28A. For the purpose of obtaining full information for ascertaining whether or not a person is chargeable to tax or for determining his liability, the Director General may by notice under his hand require that or any other person:-

- to complete and deliver to the Director General within a time specified in the notice, not being less than thirty days from the date of service of the notice, any return specified in the notice;

- to attend personally before the Director General and produce for examination all books, accounts, returns and other documents which the Director General thinks necessary;

- to make a return in accordance with paragraph (a) and also to attend in accordance with paragraph (b); or

- to provide in writing such information or particulars which the Director General thinks necessary.

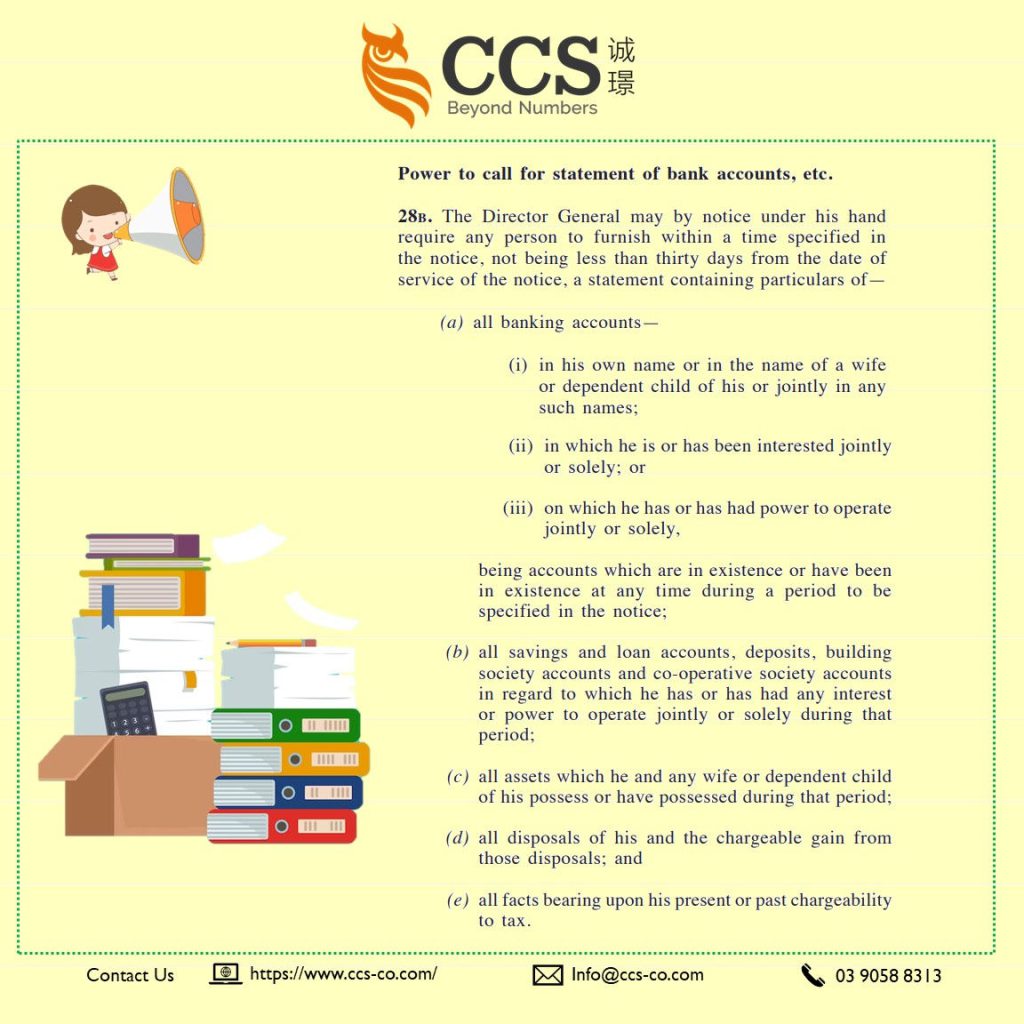

Section 28B is read as follows:-

“Power to call for statement of bank accounts, etc.”

28B. The Director General may by notice under his hand require any person to furnish within a time specified in the notice, not being less than thirty days from the date of service of the notice, a statement containing particulars of:-

- all banking accounts—

- in his own name or in the name of a wife or dependent child of his or jointly in any such names;

- in which he is or has been interested jointly or solely; or

- on which he has or has had power to operate jointly or solely, being accounts which are in existence or have been in existence at any time during a period to be specified in the notice;

- all savings and loan accounts, deposits, building society accounts and co-operative society accounts in regard to which he has or has had any interest or power to operate jointly or solely during that period;

- all assets which he and any wife or dependent child of his possess or have possessed during that period;

- all disposals of his and the chargeable gain from those disposals; and

- all facts bearing upon his present or past chargeability to tax.

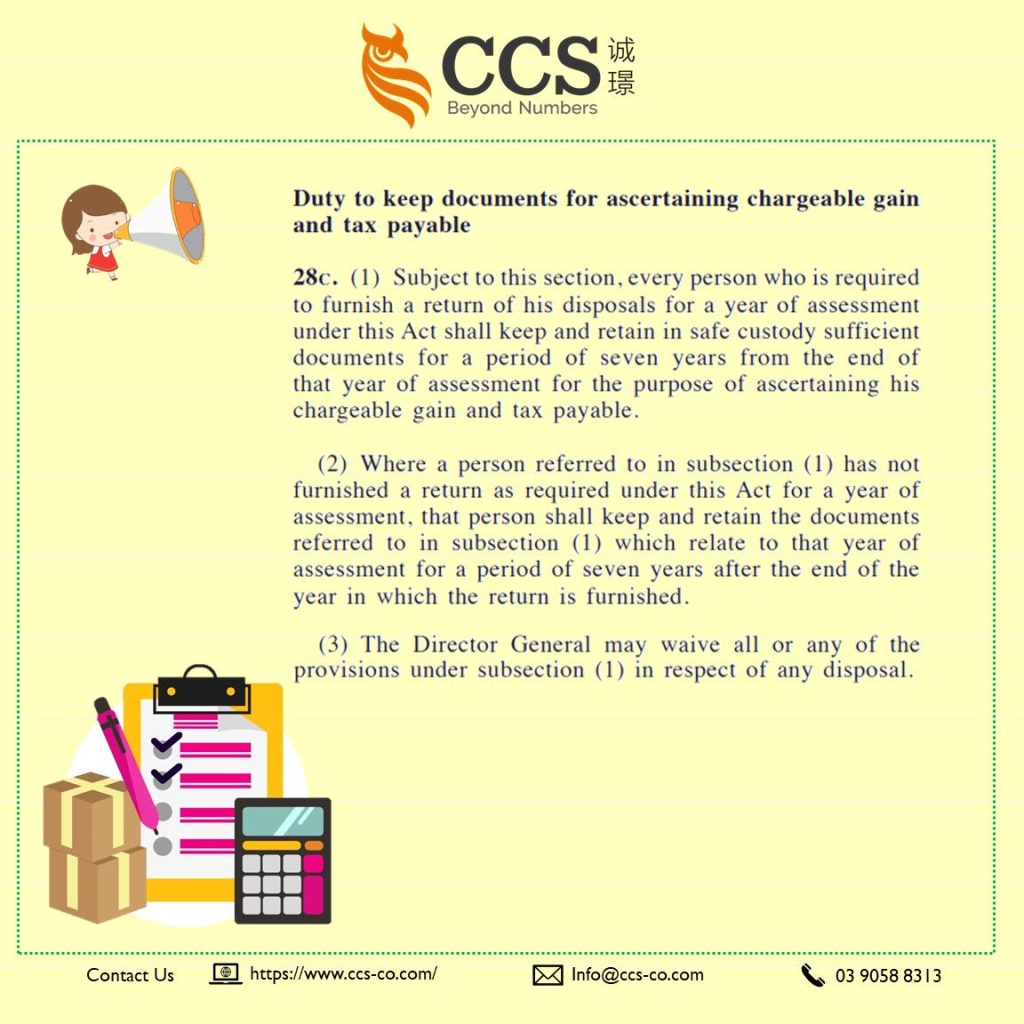

Section 28C is read as follows:-

“Duty to keep documents for ascertaining chargeable gain and tax payable”

28C. (1) Subject to this section, every person who is required to furnish a return of his disposals for a year of assessment under this Act shall keep and retain in safe custody sufficient documents for a period of seven years from the end of that year of assessment for the purpose of ascertaining his chargeable gain and tax payable.

(2) Where a person referred to in subsection (1) has not furnished a return as required under this Act for a year of assessment, that person shall keep and retain the documents referred to in subsection (1) which relate to that year of assessment for a period of seven years after the end of the year in which the return is furnished.

(3) The Director General may waive all or any of the provisions under subsection (1) in respect of any disposal.

(4) Any person who is required by this section to keep documents and—

- does so electronically, shall retain the documents in an electronically readable form and shall keep the documents in such a manner as to enable the documents to be readily accessible and convertible into writing; or

- has originally kept documents in a manual form and subsequently converts those documents into an electronic form, shall retain those documents prior to the conversion in their original form.

(5) All documents that relate to any disposal of chargeable assets situated in Malaysia shall be kept and retained in Malaysia. (6) For the purposes of this section, “documents” includes—

- statement of chargeable gains;

- statement of income and incidental cost; and

- invoices, vouchers, receipts and such other documents as are necessary to verify the particulars in a return.”.

Below is an explanation of each new section and its potential tax impact

Section 28A: Power to call for specific returns and production of books

- Explanation: This section grants the Director General the authority to issue notices requiring any person to complete specified returns, attend personally to produce relevant books and documents, or provide the necessary information. The purpose is to obtain comprehensive information for assessing a person’s liability to tax accurately.

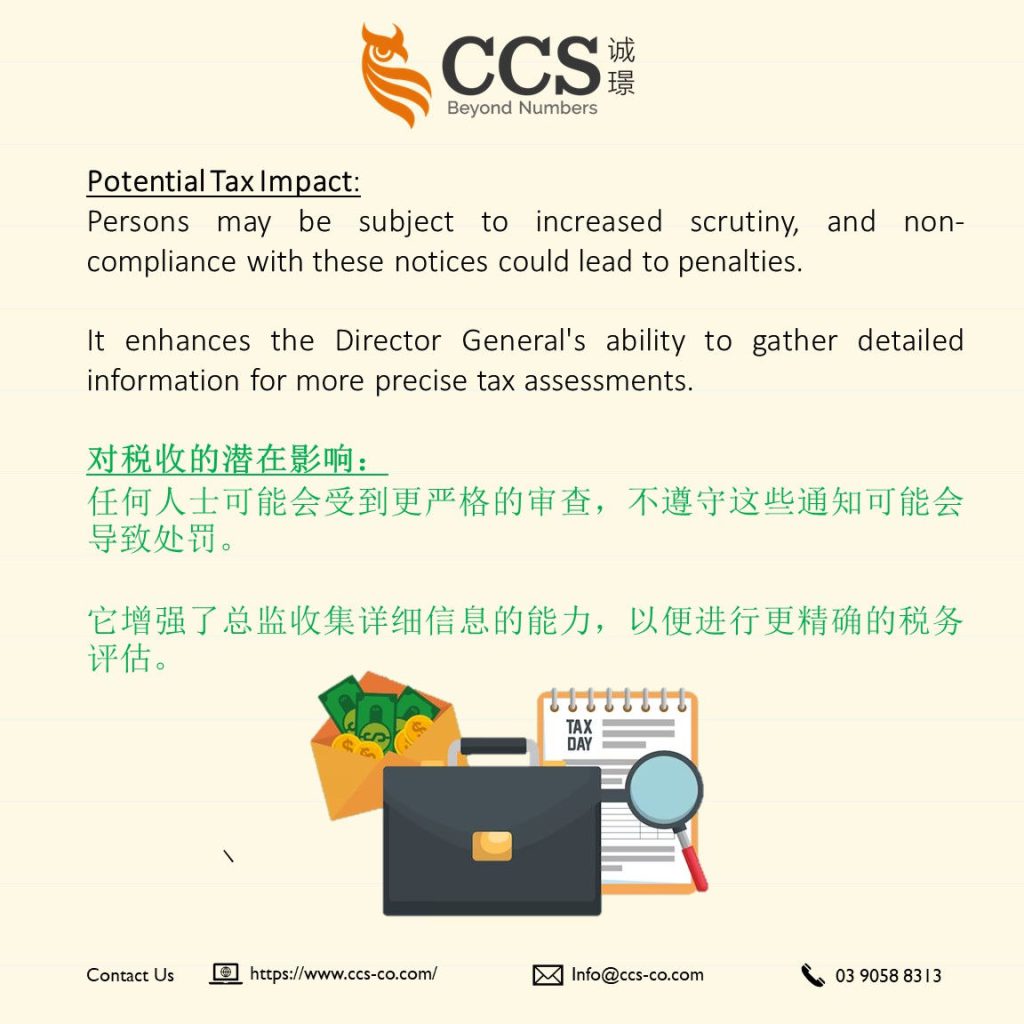

- Tax Impact: Persons may be subject to increased scrutiny, and non-compliance with these notices could lead to penalties. It enhances the Director General’s ability to gather detailed information for more precise tax assessments.

Section 28B: Power to call for a statement of bank accounts, etc.

- Explanation: This section empowers the Director General to request persons to furnish statements detailing various financial particulars, including banking accounts, savings and loan accounts, assets, disposals, and other facts relevant to tax liability.

- Tax Impact: This provision aims to improve transparency regarding financial affairs. Persons may need to provide detailed information on their financial transactions, allowing for a more accurate assessment of tax liability.

Section 28C: Duty to keep documents for ascertaining chargeable gain and tax payable

- Explanation: This section imposes an obligation on individuals to retain documents related to disposals for a period of seven years from the end of the assessment year. It also specifies the electronic retention of documents, waiver provisions, and the requirement to keep documents related to disposals in Malaysia.

- Tax Impact: Non-compliance with document retention obligations may result in penalties. However, the waiver provision allows for flexibility, and the electronic retention requirement reflects the modernisation of record-keeping practices.

Conclusion

These new sections aim to enhance the Director General’s authority to gather essential information for accurate tax assessments.

They also emphasise the importance of individuals maintaining comprehensive records related to disposals for the prescribed period.

Overall, the amendments contribute to a more robust and transparent tax assessment framework.