“Section 57A – Electronic Medium” s read as follows:-

57A(1) [Furnished in an electronic medium]

The Director General may allow any form prescribed under this Act to be furnished by any person or by any class of persons in an electronic medium or by way of an electronic transmission.

57A(2) [Determine by the Director General]

For the purposes of subsection (1), the conditions and specifications under which any prescribed form is to be furnished shall be determined by the Director General.

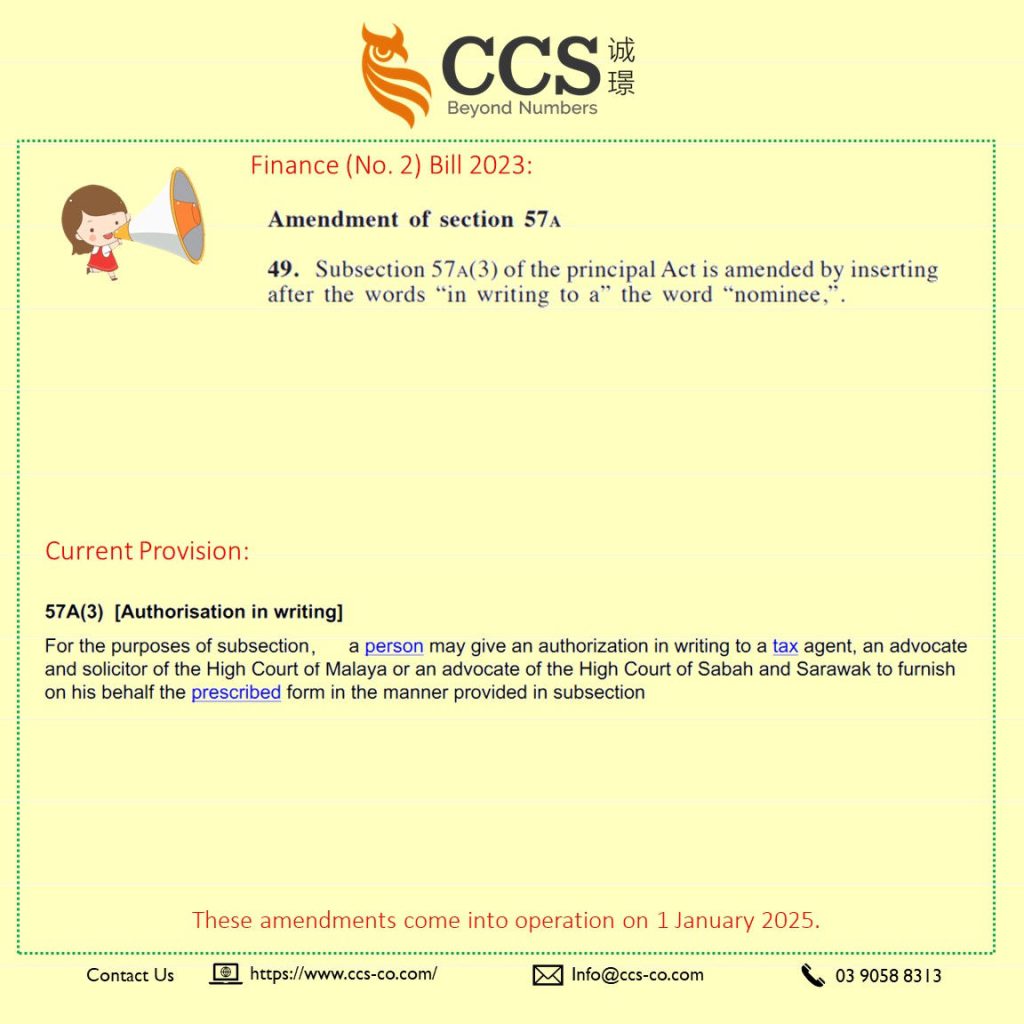

57A(3) [Authorisation in writing]

For the purposes of subsection (1), a person may give an authorization in writing to a tax agent, an advocate and solicitor of the High Court of Malaya or an advocate of the High Court of Sabah and Sarawak to furnish on his behalf the prescribed form in the manner provided in subsection (1).

57A(4) [Prescribed form furnished on authority]

The prescribed form which is furnished pursuant to subsection (3) on behalf of any person shall be presumed to have been furnished on that person’s authority until the contrary is proved, and that person shall be deemed to be cognizant of its contents.

57A(5) [Declaration]

Where subsection (3) applies—

- the person who gives the authorisation to the tax agent, advocate, and solicitor of the High Court of Malaya or advocate of the High Court of Sabah and Sarawak shall make a declaration in the prescribed form stating that—

- the tax agent, advocate and solicitor of the High Court of Malaya or advocate of the High Court of Sabah and Sarawak is authorised to furnish the form to the Director General on his behalf; and

- the information given by him to the tax agent, advocate and solicitor of the High Court of Malaya or advocate of the High Court of Sabah and Sarawak for the preparation of the form is true and correct;

- the tax agent, advocate and solicitor of the High Court of Malaya or advocate of the High Court of Sabah and Sarawak shall make a declaration in the form furnished in accordance with subsection (1) stating that—

- the form is prepared pursuant to the information given by the person who gives that authorization, and

- he has received the declaration made by the person who gives the authorisation under paragraph (a);

- the person who gives that authorisation shall keep and retain in safe custody the hard copy of the form so furnished and that a copy shall be made under processes and procedures which are designed to ensure that the information contained in the form shall be the only information furnished pursuant to this section;

- the hard copy referred to in paragraph (c) shall be signed by the person who gives that authorisation; and

- the hard copy referred to in paragraph (c) and the declaration made under paragraph (a) shall be kept and retained for a period of seven years from the end of the year of assessment in which the form is furnished.

57A(6) [Form deemed furnished to Director General] The form referred to in subsection (1) is deemed to have been furnished to the Director General by the person who gives that authorisation on the date on which an acknowledgement of receipt of the form transmitted electronically is given by the Director General to him.

Basic Understanding

In simple terms, Section 57A of the tax regulations deals with the electronic submission of prescribed forms.

Here’s an explanation:

Electronic Submission Authorization:

- Persons or classes of Persons can submit required forms electronically as permitted by the Director General.

Director General’s Determination:

- The Director General has the authority to set the conditions and specifications for electronic form submissions.

Authorisation by Third Parties:

- Persons can authorise tax agents, lawyers, or advocates to submit forms in writing on their behalf.

Presumption of Authorisation:

- Forms submitted through an authorised person are presumed to have been submitted with the Person’s permission unless proven otherwise.

Declaration Requirements:

- Persons providing authorisation must declare the truthfulness of the information given to the authorised person.

- Authorised persons must declare that the form is prepared based on the provided information and acknowledge receipt of the person’s declaration.

Document Retention:

- Persons providing authorisation must keep a hard copy of the submitted form for seven years.

- This hard copy must be signed by the person and stored securely.

- The acknowledgement of receipt and the person’s declaration must be retained for the same period.

Deemed Submission:

- The electronically transmitted form is considered submitted to the Director General on the date the acknowledgement of receipt is provided.

In summary, this section allows for the electronic submission of tax-related forms, provides a framework for third-party submissions, and outlines the necessary declarations and retention requirements for both individuals and authorised representatives.

Finance (No. 2) Bill 2023

The proposed amendment to Section 57A(3) of the tax regulations aims to include “nominee” as a category of persons authorised to submit prescribed forms electronically on behalf of another person.

Here’s an explanation:

Expansion of Authorisation:

- Currently, persons can authorise tax agents, lawyers, or advocates to submit forms electronically on their behalf.

- The proposed change includes “nominee” in the list of authorised persons.

Definition of Nominee:

- A nominee, in this context, refers to a person or entity appointed to act on behalf of another person, often for specific purposes such as managing assets or carrying out transactions.

Increased Flexibility:

- The amendment provides increased flexibility by allowing nominees to electronically submit prescribed forms electronically, streamlining the process for individuals who may prefer to designate a nominee for such tasks.

Effective Date:

- The amendment becomes effective on January 1, 2025.

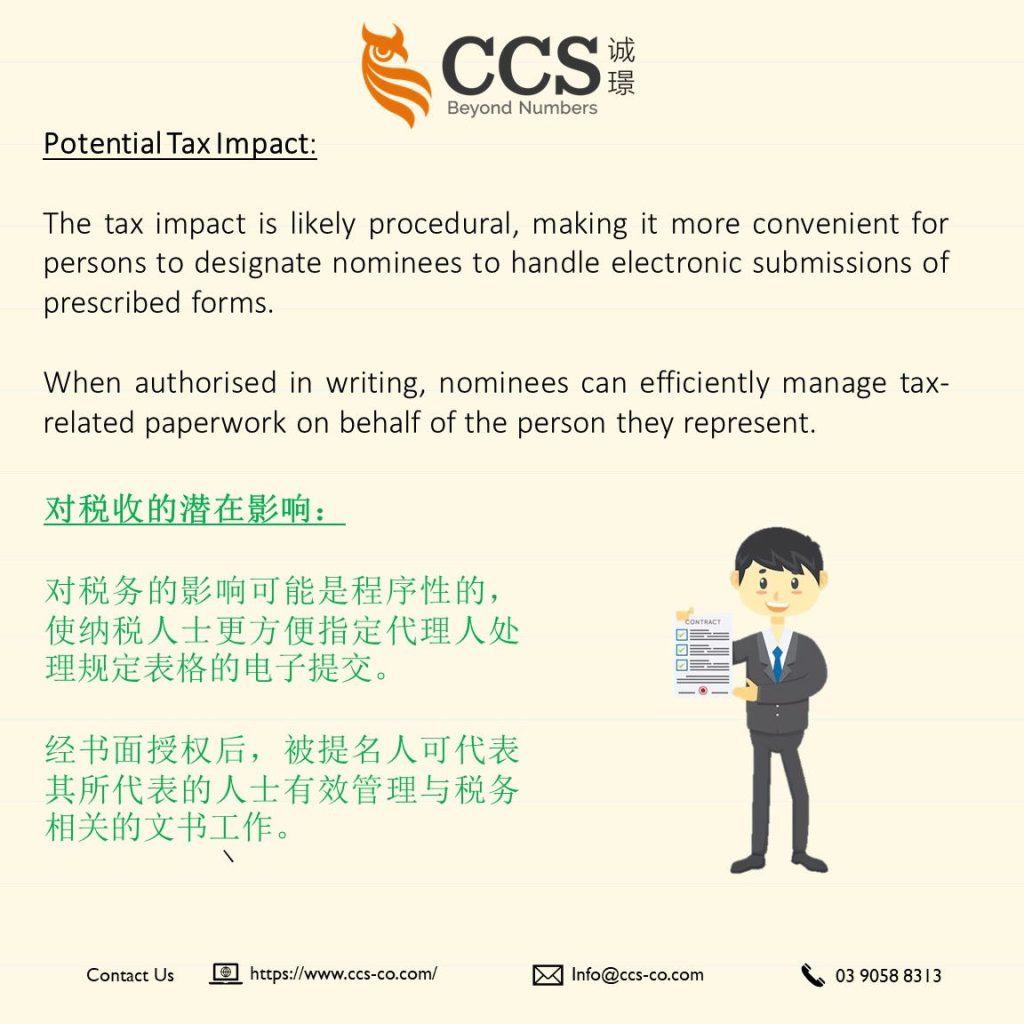

Tax Impact:

- The tax impact is likely procedural, making it more convenient for persons to designate nominees to handle electronic submissions of prescribed forms.

- When authorised in writing, nominees can efficiently manage tax-related paperwork on behalf of the individual they represent.

It’s important to note that the specific tax implications may depend on the nature of the submitted forms and the person’s tax situation.

The amendment primarily focuses on enhancing the options for persons to delegate the electronic submission process to nominees, potentially increasing efficiency and convenience in tax-related matters.