“Section 21 – Payment of the Tax” is read as follows:-

Section 21(1) [Tax due upon service of notice]

Subject to this section, the tax payable under an assessment shall, on the service of the notice of assessment on the person assessed, be due and payable at the place specified in that notice whether or not that person appeals against the assessment.

Section 21(2) [Additional tax due upon service of notice]

Where the tax payable under an assessment is increased on appeal the additional tax payable by virtue of the increased assessment shall, on the service of the notice of the increased assessment on the person assessed, be due and payable at the place specified in that notice.

Section 21(3) [Tax payable by instalments]

Where any tax is payable in accordance with subsection (1) or (2) the Director General may allow the tax to be paid by instalments in such amounts and on such dates as he may determine.

Section 21(4) [Increase on unpaid tax]

Subject to subsection (3), where any tax due and payable on the service of a notice in accordance with subsection (1) or (2) has not been paid within thirty days after the service of that notice (or within such longer period as may be allowed by the Director General), so much of the tax as is unpaid upon the expiration of those days or that period, as the case may be, shall without any further notice being served on him be increased by a sum equal to ten per cent of the tax so unpaid, and that sum shall be recoverable as if it were tax due and payable under this Act:

Provided that—

- if the tax payable is reduced on appeal or otherwise, the sum paid or payable by way of increase shall be reduced proportionately; and

- the Director General may in his discretion for any good cause shown remit the whole or any part of any increase in the tax payable under this subsection.

Section 21 outlines the timing and conditions for the payment of tax under different circumstances, including regular assessments, appeals, and the possibility of paying in instalments.

It also addresses the consequences of not paying the tax within the specified timeframe, with provisions for an increase and the Director General’s discretionary power to remit such increases under certain circumstances.

Finance (No. 2) Bill 2023

Finance (No. 2) Bill 2023 proposes an amendment of section 21

Section 21 of the Real Property Gains Tax Act 1976 is amended:

- in subsection (1), by substituting for the words “Subject to this section” the words “Except as provided in subsections (1A) and (1B)”; and

- by inserting after subsection (1) the following subsections:

“(1A) Where an assessment on a return has been made under subsection 14(1), the tax or additional tax payable under the assessment shall be due and payable within the period of sixty days from the date of disposal whether or not that person appeals against the assessment or additional assessment.

(1B) Where an assessment on an amended return has been made under section 15A, the tax or additional tax payable under the assessment shall be due and payable on the day the amended return is furnished whether or not that person appeals against the assessment or additional assessment.”.

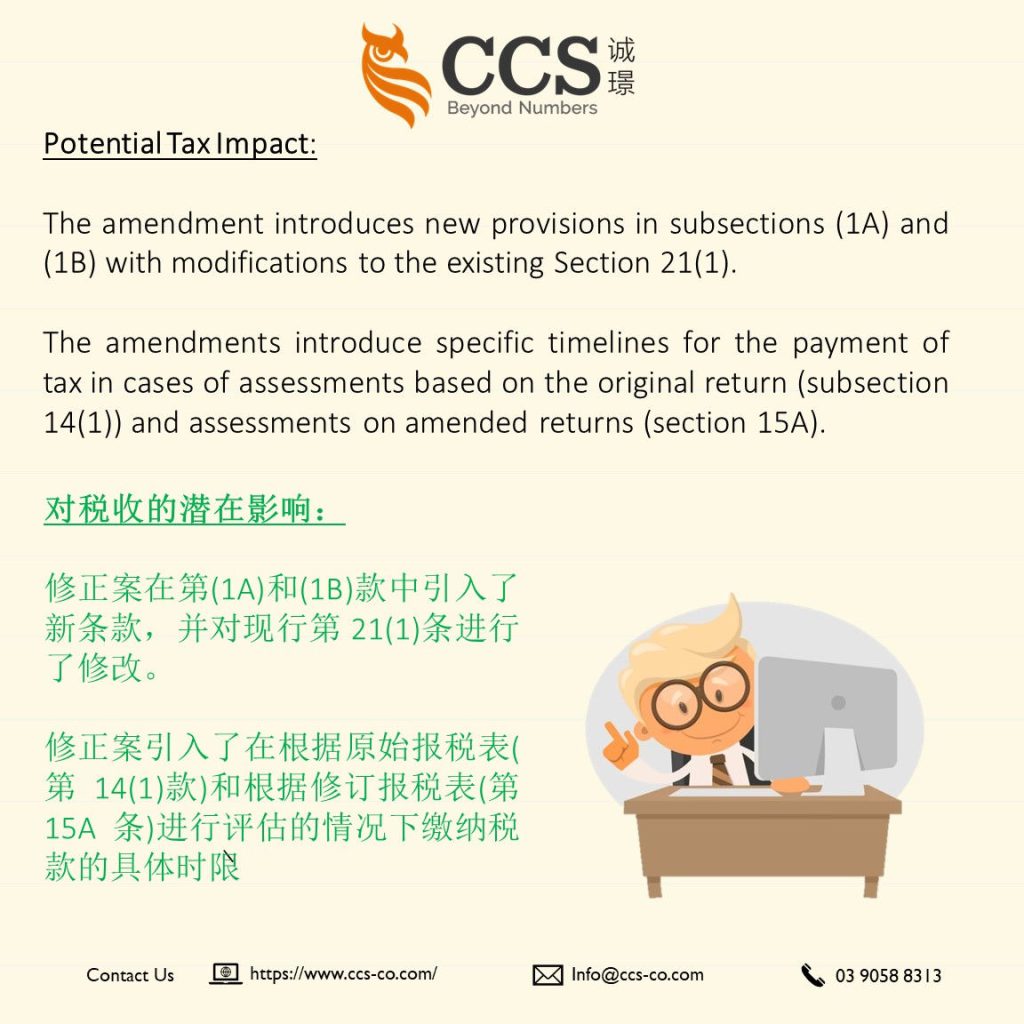

The amendment introduces new provisions in subsections (1A) and (1B) with modifications to the existing Section 21(1).

Subsection (1A) specifies that when an assessment is made based on a return under subsection 14(1), the tax or additional tax becomes due and payable within a period of sixty days from the date of disposal. This due date is irrespective of whether the person assessed decides to appeal against the assessment or additional assessment.

Subsection (1B) states that in the case of an assessment made on an amended return under section 15A, the tax or additional tax becomes due and payable on the day the amended return is furnished.

Like subsection (1A), the due date is irrespective of whether the person assessed decides to appeal against the assessment or additional assessment.

Summary of Amendments:

The amendments introduce specific timelines for the payment of tax in cases of assessments based on the original return (subsection 14(1)) and assessments on amended returns (section 15A).

These timelines are distinct from the general provision in subsection (1) and clarify when the tax becomes due and payable in these scenarios.

These changes aim to streamline the payment timelines based on the type of assessment, bringing more specificity to the payment requirements and ensuring timely compliance with tax obligations.