“Section 20 – Finality of Assessment” is read as follows:-

Section 20(1) [When assessment becomes final and conclusive]

Subject to this section, an assessment shall become final and conclusive for all the purposes of this Act as regards the amount of the tax assessed under it or the allowable losses indicated in it, as the case may be:-

- on the expiry of the time for appeal against the assessment; or

- where an appeal is made, on the appeal being finally disposed of.

Section 20(2) [Director General’s assessment revision]

Subsection (1):

- shall not apply to an assessment made under section 14(3) until it is adopted as the assessment for the year of assessment to which it relates;

- shall not prevent the Director General from making in respect of any year of assessment—

- an assessment under section 15(1) or (2); or

- a revision under section 19(1).

Overview

Section 20 of the Real Property Gains Tax Act 1976 outlines when an assessment becomes final and conclusive for the purposes of the Act.

It specifies the circumstances under which the tax assessment or allowable losses indicated in the assessment are considered settled and cannot be further appealed or revised.

Key Points:

When Assessment Becomes Final:

- An assessment becomes final and conclusive for all purposes of the Act regarding the amount of tax assessed or allowable losses indicated when:

- The time for appeal against the assessment expires, or

- If an appeal is made, when the appeal is finally disposed of.

Exceptions to Finality:

- The finality mentioned above does not apply under certain circumstances:

- For an assessment made under section 14(3), finality is deferred until it is adopted as the assessment for the relevant year of assessment.

- The Director General is not prevented from making assessments under section 15(1) or (2) or a revision under section 19(1) for any year of assessment.

Practical Implications:

- Once the time for appeal has passed or an appeal is resolved, the assessment is considered settled and final.

- However, certain assessments and revisions, such as those under section 14(3) or section 19(1), may have different timelines for finality.

Example for Illustration:

Suppose a taxpayer receives an assessment for the sale of a property.

They have a limited time to appeal the assessment.

If they do not appeal within that timeframe, or if the appeal is resolved, the assessment becomes final and conclusive.

However, if the Director General needs specific assessments or revisions under certain sections, finality may be subject to different conditions.

Significance:

Understanding when an assessment becomes final is crucial for both taxpayers and tax authorities, providing clarity on the resolution of tax matters and the limitations on further appeals or revisions.

Finance (No. 2) Bill 2023

Finance (No. 2) Bill 2023 proposes an amendment to section 20

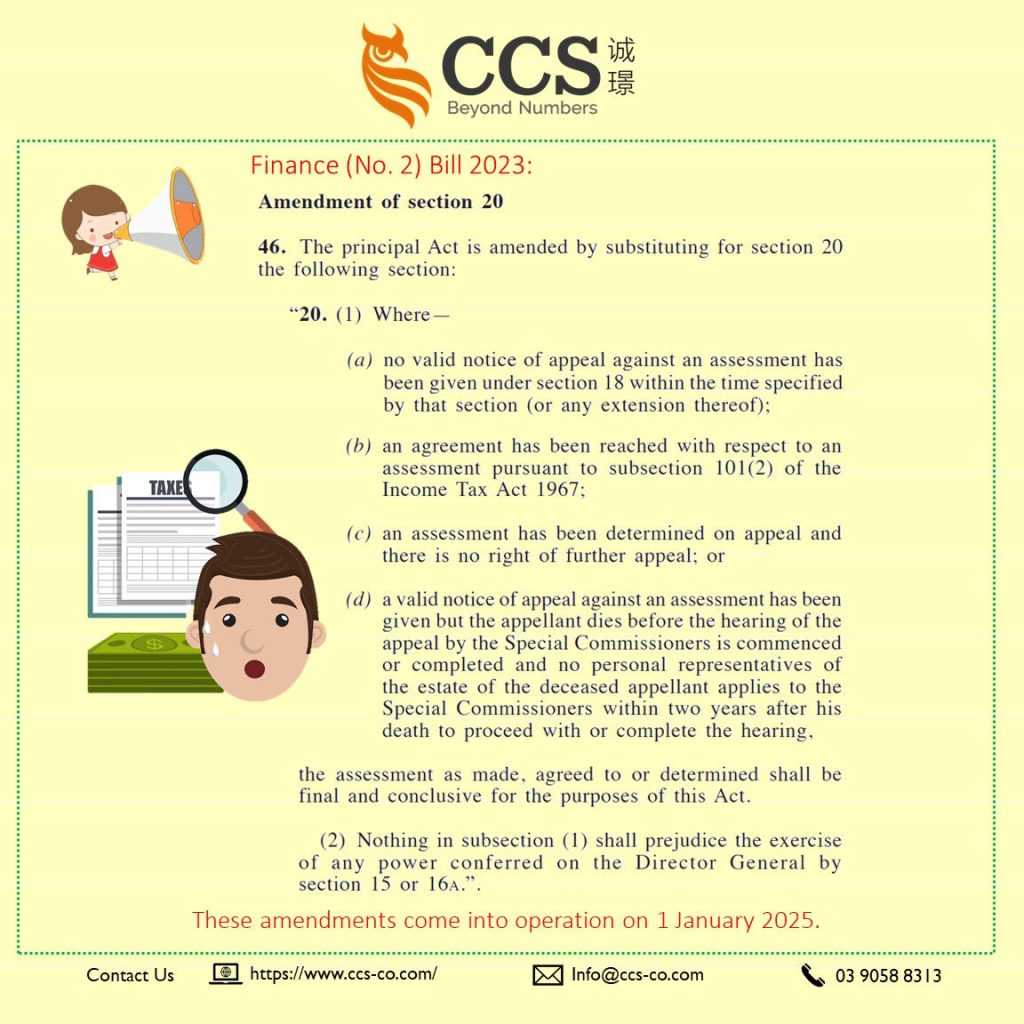

The Real Property Gains Tax Act 1976 is amended by substituting for section 20 the following section:

“Section 20. (1) Where:-

- no valid notice of appeal against an assessment has been given under section 18 within the time specified by that section (or any extension thereof);

- an agreement has been reached with respect to an assessment pursuant to subsection 101(2) of the Income Tax Act 1967;

- an assessment has been determined on appeal and there is no right of further appeal; or

- a valid notice of appeal against an assessment has been given but the appellant dies before the hearing of the appeal by the Special Commissioners is commenced or completed and no personal representatives of the estate of the deceased appellant applies to the Special Commissioners within two years after his death to proceed with or complete the hearing,

the assessment as made, agreed to or determined shall be final and conclusive for the purposes of this Act.

Section 20(2) Nothing in subsection (1) shall prejudice the exercise of any power conferred on the Director General by section 15 or 16A.

The proposed amendment to Section 20 of the Real Property Gains Tax Act 1976 outlines specific circumstances under which an assessment becomes final and conclusive for the purposes of the Act.

The amendment aims to standardise these circumstances, particularly in the context of a self-assessment system for disposing chargeable assets.

Key Points:

Circumstances for Finality:

- The assessment becomes final and conclusive when:

- No valid notice of appeal is given within the specified time.

- An agreement is reached regarding the assessment under subsection 101(2) of the Income Tax Act 1967.

- The assessment is determined on appeal, and there is no further right of appeal.

- A valid notice of appeal is given, but the appellant dies before the hearing is commenced or completed, and no personal representatives of the estate apply to the Special Commissioners within two years after the appellant’s death.

Finality in Specific Situations:

- The assessment, as made, agreed to, or determined in the mentioned circumstances, is considered final and conclusive for the purposes of the Real Property Gains Tax Act.

Limitations on Prejudice:

- The proposed amendment specifies that nothing in this section shall prejudice the exercise of powers conferred on the Director General by Section 15 or 16A.

Practical Implications:

- The amendment clarifies when an assessment is deemed final and conclusive, streamlining the circumstances across various scenarios, including situations involving self-assessment for the disposal of chargeable assets.

Tax Impact:

- Taxpayers and tax authorities will have clear guidelines on when an assessment becomes final, reducing uncertainty and providing a standardised approach to finality in different situations.

Difference Between Proposed Amendment and Current Provision under Section 20:

Current Provision (Before Amendment)

The current Section 20 of the Real Property Gains Tax Act 1976 outlines when an assessment becomes final and conclusive.

However, the specific circumstances leading to finality are not explicitly detailed in the existing provision.

Proposed Amendment:

The proposed amendment to Section 20 introduces clarity and specificity regarding the circumstances under which an assessment becomes final and conclusive. It delineates four distinct situations:

- No valid notice of appeal within the specified time.

- Agreement reached regarding the assessment.

- The assessment determined on appeal with no further right of appeal.

- The appellant dies before the hearing is completed, and no personal representatives apply within two years.

Key Differences:

Clarity and Specificity:

- The amendment provides a clearer and more detailed description of the circumstances leading to the finality of an assessment. It explicitly lists the scenarios, offering greater transparency.

Inclusion of Self-Assessment System:

- The proposed amendment is designed to align with introducing a self-assessment system for disposing of chargeable assets. It ensures consistency and standardisation in finalising assessments in the context of self-assessment.

Explicit Mention of Death of Appellant:

- The amendment explicitly addresses the situation where an appellant dies before the appeal hearing is commenced or completed. It sets a specific timeframe (two years) for the personal representatives to apply to the Special Commissioners.

Reference to Other Sections:

- The proposed amendment includes a provision stating that nothing in Section 20 shall prejudice the exercise of powers conferred on the Director General by Sections 15 or 16A.

Significance of the Amendment:

The proposed amendment brings more precision and coherence to Section 20, particularly in light of the changes related to the self-assessment system. It enhances understanding and consistency in determining when an assessment reaches finality under various circumstances.

Overall, the amendment serves to streamline the finalisation of assessments and contributes to a more robust and standardised tax framework.