“Section 19 – Error or Mistake” is read as follows:- Section 19(1) [Revision of assessment]

A person upon whom a notice of assessment is served may within five years after the end of the year of assessment in which the assessment was made, apply in writing to the Director General for a revision of the assessment on the ground that the assessment is excessive by reason of an error or mistake in a return or other statement made by that person for the purposes of the assessment.

Section 19(2) [Where no relief shall be given]

No relief shall be given under subsection (1) in respect of an error or mistake as to the basis on which the liability of the person concerned ought to have been computed where the return containing the error or mistake was in fact made on the basis of or in accordance with the practice of the Director General generally prevailing at the time when the return was made.

Section 19(3) [Application as notice of appeal]

An application under subsection (1) shall be, as nearly as may be, in the same form as a notice of appeal under section 18 (indicating as the grounds of appeal the error or mistake relied on), and shall be deemed to be, and shall be disposed of as if it were, an appeal under that section, the application itself being taken as the notice of appeal.

Basic Understanding

Section 19 of the Real Property Gains Tax Act 1976 provides a mechanism for persons who have received a notice of assessment to seek a revision of the assessment if they believe there is an error or mistake that has led to an excessive tax assessment.

Here’s a breakdown in simpler terms:

1. Revision of Assessment:

- If you receive a notice stating the amount of property gains tax you owe, you have the right to ask for a review or correction if you believe there is an error or mistake.

- You can make this request within five years after the end of the tax year in which the assessment was originally made.

2. Grounds for Revision:

- The grounds for requesting a revision are errors or mistakes in the information you provided in your tax return or any other statement that was used to calculate the property gains tax.

- The goal is to correct the assessment so that it accurately reflects your actual tax liability.

3. Limitations on Relief:

- There are certain situations where relief won’t be granted. Specifically, if the error or mistake in your return aligns with the practices of the tax authority at the time you submitted the return, you may not be eligible for a revision.

Example:

- Let’s say the standard practice at the time of your submission was to calculate tax based on the property’s selling price.

- However, you mistakenly used the property’s purchase price as the basis for your calculation, which was not in line with the prevailing practice.

- In this case, Section 19(2) would prevent you from seeking relief for this particular error because your return was made in accordance with the practices of the tax authority at that time.

4. Application Process:

- To seek a revision, you must submit a written application to the Director General. This application should outline the specific error or mistake you believe exists and led to the excessive assessment.

- The application process is similar to filing an appeal, and the grounds for the appeal are the errors or mistakes you’ve identified.

5. Dealing with the Application:

- Your application for revision is treated like an appeal under Section 18 of the Act. This means it will go through a process similar to that of an appeal.

- The application itself serves as the notice of appeal, and it will be handled as if it were an official appeal.

In summary, Section 19 provides a way for persons to correct property gains tax assessments if they believe errors or mistakes in their tax returns led to an excessively high assessment.

The process involves submitting a written application to the tax authority, outlining the specific issues you want to address.

Finance (No. 2) Bill 2023

Finance (No. 2) Bill 2023 proposes an amendment of section 19.

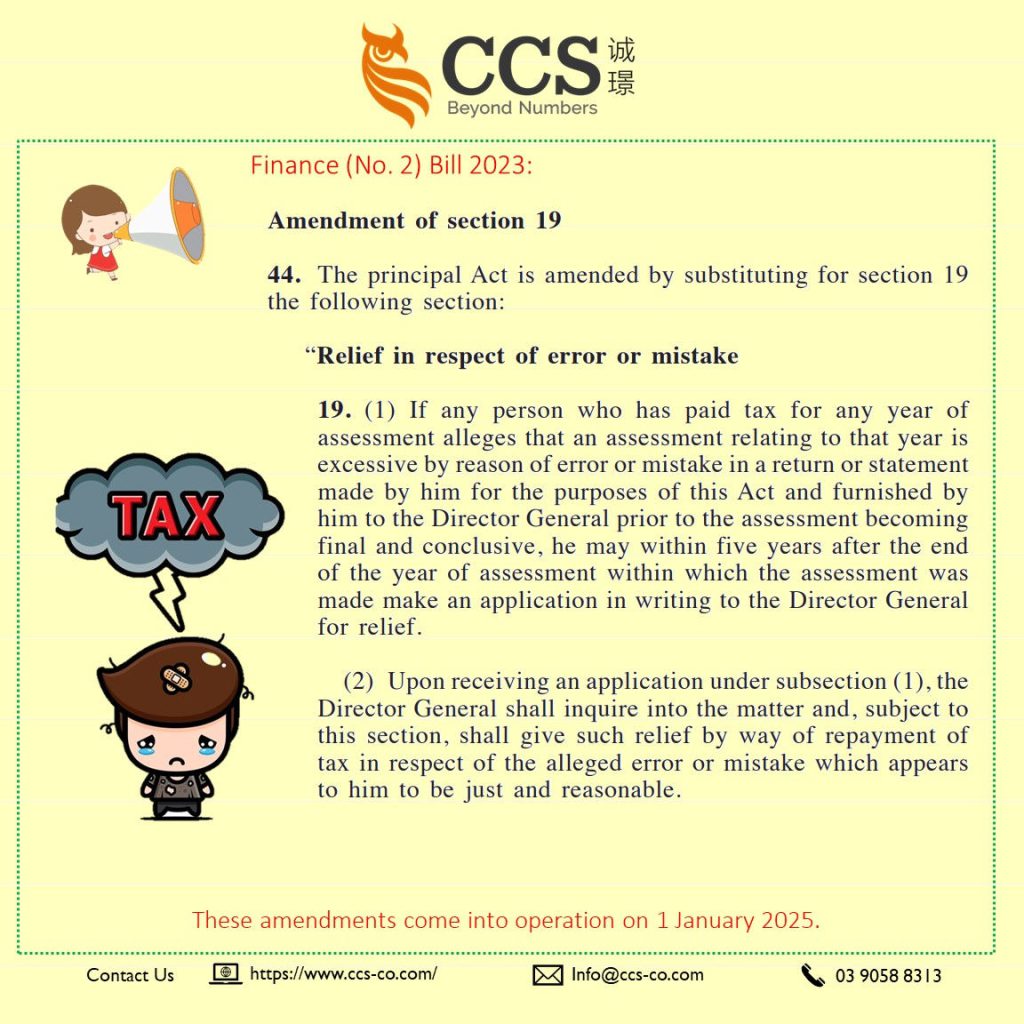

The Real Property Gains Tax Act 1976 is amended by substituting for section 19 the following section:

“Relief in respect of error or mistake

Section 19(1) If any person who has paid tax for any year of assessment alleges that an assessment relating to that year is excessive by reason of error or mistake in a return or statement made by him for the purposes of this Act and furnished by him to the Director General prior to the assessment becoming final and conclusive, he may within five years after the end of the year of assessment within which the assessment was made make an application in writing to the Director General for relief.

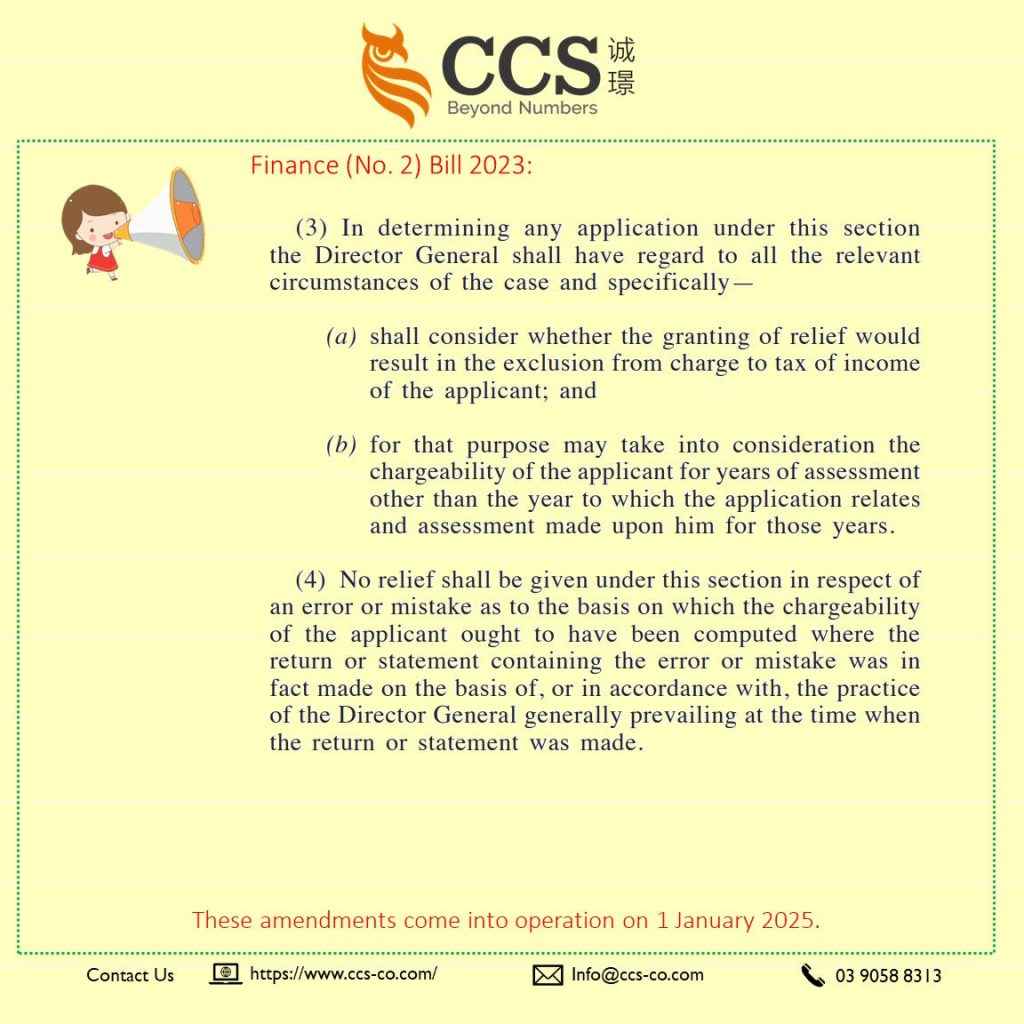

Section 19(2) Upon receiving an application under subsection (1), the Director General shall inquire into the matter and, subject to this section, shall give such relief by way of repayment of tax in respect of the alleged error or mistake which appears to him to be just and reasonable. Section 19(3) In determining any application under this section, the Director General shall have regard to all the relevant circumstances of the case and specifically:-

- shall consider whether the granting of relief would result in the exclusion from charge to tax of income of the applicant; and

- for that purpose may take into consideration the chargeability of the applicant for years of assessment other than the year to which the application relates and assessment made upon him for those years.

Section 19(4) No relief shall be given under this section in respect of an error or mistake as to the basis on which the chargeability of the applicant ought to have been computed where the return or statement containing the error or mistake was in fact made on the basis of, or in accordance with, the practice of the Director General generally prevailing at the time when the return or statement was made. Section 19(5) An application under subsection (1) shall be as nearly as may be in the same form as a notice of appeal under section 18, and, where the applicant is aggrieved by the Director General’s decision:-

- the applicant may, within six months after the decision is being informed, request in the prescribed form for the Director General to forward the application to the Special Commissioners;

- the Director General shall within three months after receiving the request send the application forward as if he were sending an appeal forward pursuant to section 102 of the Income Tax Act 1967; and

- the application shall thereupon be deemed to be an appeal and shall be disposed of accordingly.”.

The proposed amendment introduces a new Section 19 into the Real Property Gains Tax Act 1976, focusing on providing relief for errors or mistakes in returns or statements made by a taxpayer.

Here are the key points:

Application for Relief:

- A person who has paid tax for a particular year of assessment can allege that the assessment for that year is excessive due to errors or mistakes in a return or statement.

- The application for relief must be made within five years after the end of the year of assessment in which the assessment was made.

- The return or statement containing the alleged error or mistake must have been furnished to the Director General before the assessment became final and conclusive.

Director General’s Inquiry and Relief:

- Upon receiving the application, the Director General will inquire into the matter.

- The Director General has the authority to grant relief by repaying the tax in respect of the alleged error or mistake if it appears to be just and reasonable.

Considerations for Relief:

- The Director General, in determining the application, considers all relevant circumstances.

- Specific considerations include whether granting relief would exclude certain income from tax and the chargeability of the applicant for other years of assessment.

No Relief for Prevailing Practices:

- No relief shall be given if the error or mistake in the return or statement aligns with the practice of the Director General generally prevailing at the time of submission.

Appeal Process:

- If the applicant is aggrieved by the Director General’s decision, they can request, within six months of being informed, for the application to be forwarded to the Special Commissioners.

- Once forwarded, the application is deemed an appeal and will be disposed of accordingly.

Comparison with Existing Section 19:

The proposed amendment expands the scope and procedures for seeking relief due to errors or mistakes.

It introduces a more structured process, including considerations for relief and an avenue for appeal to the Special Commissioners.

Example for Illustration:

Suppose a taxpayer mistakenly undervalued the property in their property sale tax return.

Suppose this error is identified within five years of the assessment.

In that case, the taxpayer can apply for relief under the new Section 19, and the Director General may adjust the tax liability accordingly.

Tax Impact:

The amendment provides a mechanism for taxpayers to rectify errors or mistakes in their returns, potentially reducing tax liability.

However, relief won’t be granted if the error aligns with the prevailing practices at the time of submission.

The appeal process offers a further avenue for resolution if the taxpayer disagrees with the Director General’s decision.