Update: The Ismail Sabri Government Budget is no longer applicable.

Malaysia’s national budget for 2023 was re-tabled again in February 2023; for more info, please visit – https://www.ccs-co.com/post/budget-2023-malaysia-madani

This tax incentive included in Budget 2023, tabled in Parliament on 7 October 2022, was not included in Budget 2023 (Re-tabled) on 24 February 2023.

Current Position

Income tax relief is given on medical treatment expenses of up to RM8,000 as follows:

- serious illness for taxpayer, spouse or child;

- fertility treatment for taxpayer or spouse;

- vaccination for taxpayer, spouse or child limited to RM1,000; and

- full medical check-up, mental health check-up or consultation, COVID-19 detection test including the purchase of self-test kit for taxpayer, spouse or child limited to RM1,000.

Proposal [This tax incentive included in Budget 2023, tabled in Parliament on 7 October 2022, was not included in Budget 2023 (Re-tabled) on 24 February 2023]

It is proposed that the scope of tax relief be expanded to cover:

- dental examination and treatment expenses of up to RM1,000 from dental practitioners registered with the Malaysian Dental Council.

This would support the implementation of the National Dental Health Policy, which aims to increase access to dental care for the Rakyat.

Effective Date

From the year of assessment 2023.

Footnotes – Are All Dental Expenses Qualified For the Tax Relief?

In general, dental expenses include:

- Examination,

- Routine dental care; and

- Non-routine dental treatments.

Routine dental care includes:

- fillings

- scaling or cleaning

- tooth extraction

- providing or repairing artificial teeth or dentures.

Non-routine dental treatments includes:

- crowns

- veneers or Rembrandt type etched fillings

- tip replacing

- gold posts or fibreglass posts

- inlays (a smaller version of a gold crown).

- endodontics (root canal treatment)

- periodontal treatment for gum disease such as:

- root planning (including curettage and debridement) and gum flaps

- chrome cobalt splints (but not if it contains teeth)

- implants (including bone grafting and bone augmentation)

- orthodontic treatment (provision of braces and related treatments)

- surgical extraction of impacted wisdom teeth

- bridgework (an enamel-retained bridge or a tooth-supported bridge).

- 牙冠

- 贴面或伦勃朗式的蚀刻补牙

- 更换牙尖

- 金柱或石英玻璃柱

- 嵌体(金冠的缩小版)。

- 牙髓病学(根管治疗)

- 牙周治疗牙龈疾病,如。

- 根管治疗(包括刮治和清创)和牙龈瓣治疗

- 铬钴夹板(但如果含有牙齿,则不需要)。

- 植入物(包括骨移植和骨增生)。

- 正畸治疗(提供牙套和相关治疗)。

- 手术拔除受影响的智齿

- 桥接(珐琅质固定桥或牙齿支持的桥)。

We do not believe that all of the costs associated with dental care will be eligible for a tax deduction.

In our opinion and based on our research, the only dental services that are eligible for a tax deduction of up to RM1,000 are dental examinations and non-routine dental treatments.

We believe the Dentist will advise you if any of your treatment qualifies for tax relief

Example

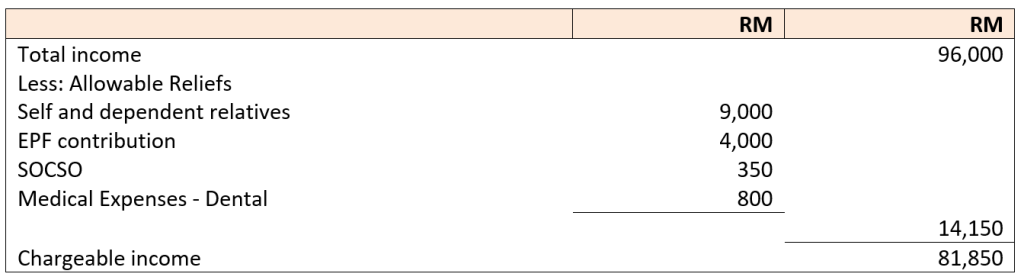

Nadia, who is resident in Malaysia for the year 2023, as a Finance Director.

She has employment income of RM96,000 for the year ended 31.12.2023.

In that year, she made the following contributions to :

- EPF – RM 10,560

- SOCSO – RM 297

- EIS – RM 97.20

Additional information:

- Dental examination and treatment – RM 800

Computation of Nadia’s Chargeable Income for YA 2023

As Nadia –

- is resident in Malaysia;

- is entitled to a deduction for self and dependent relatives under paragraph 46(1)(a) of the ITA; and

- has chargeable income exceeding RM35,000

she is not entitled to the personal rebate of RM400 for YA 2023.

Income Tax Payable by Nadia for YA 2023

If Nadia goes to the dentist for her examination and treatment in 2021, she will not be able to take advantage of the tax relief.

Footnotes

Paragraph 46(1)(g) of the ITA provides that a deduction of up to RM6,000 is allowed on the amount expended by the individual for treatment of serious diseases on himself, his or her spouse or his or her child.

The maximum amount allowed as a deduction prior to the YA 2015 is RM5,000.

For the purpose of this deduction, “Serious Disease” means acquired immunity deficiency syndrome, Parkinson’s disease, cancer, renal failure, leukaemia or other similar diseases.

With effect from the YA 2020, the medical expenses are extended to include the expenses expended or deemed expended by the individual for undergoing fertility treatment to have a baby, on himself or on his wife, or in the case of a wife on herself or on her husband.

The claim for fertility treatment is only eligible for married individual.

“Fertility Treatment” means intrauterine insemination or in vitro fertilization treatment or any other fertility treatment. Besides that, consultation fees and medicines are also part of the fertility treatment for the purpose of claiming this deduction.

The claim for medical expenses has to be evidenced by a receipt and certification issued by a medical practitioner registered with the MMC that the serious disease treatment was provided to that individual, spouse or child; or fertility treatment was provided to the individual or the spouse.

The total amount of deduction for the medical expenses for serious disease treatment and fertility treatment under paragraph 46(1)(g) is limited to a maximum amount of RM6,000.

Effective Y/A 2023, the scope of the relief is expanded to cover expenses on dental examination and treatment from dental practitioners registered with the Malaysian Dental Council of up to RM1,000.

Our website's articles, templates, and material are solely for reference. Although we make every effort to keep the information up to date and accurate, we make no representations or warranties of any kind, either express or implied, regarding the website or the information, articles, templates, or related graphics that are contained on the website in terms of its completeness, accuracy, reliability, suitability, or availability. Any reliance on such information is therefore strictly at your own risk.

Keep in touch with us so that you can receive timely updates |

要获得即时更新,请与我们保持联系

1. Website ✍️ https://www.ccs-co.com/ 2. Telegram ✍️ http://bit.ly/YourAuditor 3. Facebook ✍

- https://www.facebook.com/YourHRAdvisory/?ref=pages_you_manage

- https://www.facebook.com/YourAuditor/?ref=pages_you_manage

4. Blog ✍ https://lnkd.in/e-Pu8_G 5. Google ✍ https://lnkd.in/ehZE6mxy

6. LinkedIn ✍ https://www.linkedin.com/company/74734209/admin/