Income Tax (Capital Allowance) (Development Cost for Customised Computer Software) Rules 2019

On 3 October 2019, the Minister, in the exercise of the powers conferred by paragraphs 154(1)(b), 33(1)(d) and paragraphs 10 and 15 of Schedule 3 to the Income Tax Act 1967 [Act 53], gazetted the Income Tax (Capital Allowance) (Development Cost for Customised Computer Software) Rules 2019 [P.U (A) 274/2019].

On April 9, 2020, the Malaysian Inland Revenue Board (also known as the “IRBM”/”LHDNM”) issued Practice Note No. 2/2020 (“Practice Note”) with a publication date of March 16, 2020.

The purpose of this Practice Note is to provide some direction on how these Rules should be put into practice.

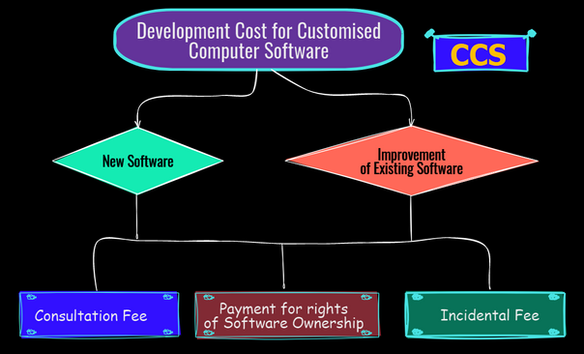

According to the Practice Note, the term “development cost” for customised computer software refers to:

- the expenses incurred in:

- producing new software; or

- improving the existing software

- for it to be used to conduct business.

Based on the Rules effective from YA 2018:

- a Malaysian resident who has incurred qualifying development costs for customised computer software

- will be eligible for CA claims at 20% Initial Allowance (IA) and 20% Annual Allowance (AA).

Qualifying Development Costs

- Consultation Fee

- Consultation fee incurred on the development of the software specifically to develop a new software system, modification or modernisation of the existing software, excluding consultation fees related to initial procedure or planning stage such as feasibility study or preliminary study.

- Payment for rights of software ownership

- Payment for the right to use the software exclusively.

- The incidental fee relating to the development of customised computer software

- Payment incurred, which enabled the use of the software in a business and capitalised such as change of requirement the software.

However, the Practice Note does not include a comprehensive list of examples of incidental expenses that may be seen as related to customised computer software production.

Withholding Tax Implications

Withholding tax (often known as “WHT”) may be applied to payments made to non-residents for the costs of developing customised computer software under either Section 109 or Section 109B of the Income Tax Act (ITA), depending on the specific circumstances of each transaction.

If the appropriate WHT is not withheld and remitted to the MIRB within one month after paying or crediting the non-resident:

- A penalty equal to 10% of the unpaid WHT will be assessed.

- In addition, a capital allowance would not be granted for any qualifying capital expenditures that were incurred but for which the WHT, if applicable, had not been paid or remitted to the MIRB. In this case, the expenditure would not be eligible for a capital allowance.

Capital allowance can be claimed in the basis period for a YA that the customised computer software can be used in a business.

Effective Date and Timing of Claim

The Practice Note provides:

- The Rules apply to development costs for customised computer software incurred in the basis period from YA 2018.

- The cost is considered/deemed to have been incurred when the customised software can be used for business purposes.

To better demonstrate the position of the IRBM on the conditions above, the following examples have been provided in Practice Note 2/2020.

* Y/A 2017’s cost of development does not qualify.

Non Application

The claim for capital allowance for the development cost of customised software provided under these Rules, however, will not be applicable if the person has claimed in respect of the customised software:

- Any incentive under the Promotion of Investment Act 1986

- Deduction under s 33 of the Income Tax Act 1967 (ITA)

- Deduction for research and development expenditure under s 34A of ITA

- Reinvestment allowance

- Investment allowance for the services sector

- Accelerated capital allowance under any Rules, or

- Any tax exemption which is equivalent to any part or the whole amount of the development cost incurred.

Response from the IRBM on 19 May 2022

On 19 May 2022, CTIM sought confirmation on whether the following constitute qualifying expenditure as development cost for customised computer software (CCS) under the P.U. (A) 274/2019:

- Cloud service charges incurred during the development phase;

- Staff costs were incurred explicitly during the development of the CCS;

- Data migration from legacy IT system to the new CCS as part of the implementation of the CCS before “go live”;

- Development of mobile application.

The following is a response from the IRBM to the points that CTIM made on 16 September 2021:

Cloud Service charges incurred during the Development Phase

Suppose cloud service payments are part of the expenses incurred while the CCS is being developed to enable the CCS to be used in business. In that case, the payment of the cloud service charges may be included as development costs for the CCS under the P.U. (A) 274/2019 on the assumption that the expenses are incurred during the CCS development period before the CCS can be fully utilised in business and capitalised.

After the CCS development period has ended and the CCS can be used in business, maintenance-related expenses can be claimed under S.33 of the ITA.

Staff Costs were incurred explicitly during the Development of the CCS

Staff cost may be included as development cost for the CCS under P.U.(A) 274/2019, subject to the following conditions: –

- The staff cost is not included in the salary payment to existing company employees. (Note: The staff is explicitly appointed to develop the CCS.)

- The job description of the staff is clearly and manifestly for CCS development.

Data Migration from legacy IT Systems to the new CCS as part of the implementation of the CCS before “go live.”

Based on the fact that payment of data migration from legacy IT systems needs to be incurred while the CCS is developed to enable it to be used in business, LHDNM is of the view that it can be included as a development cost for the CCS under the P.U.(A) 274/2019.

It is eligible to be claimed under the Incidental fee provided that the expenses are incurred during the CCS development period to enable the software to be used in business and not for routine data migration activities.

Expenditure for data migration from a legacy system that is usual/customary or routine and incurred in generating business income can be claimed under S.33 of the ITA.

Development of the Mobile Application

LHDNM agrees with CTIM’s view that this mobile application is part of the CCS developed.

Consequently, mobile application expenditure can be included as a development cost for the CCS under P.U.(A) 274/2019.

Response from the IRBM on 4 June 2020

Issue 1:

- CTIM urged IRBM to confirm that “customised computer software” refers to software other than commercial off-the-shelf software and includes tailor-made software, software developed from scratch that caters to specific requirements of the business. software customised from a base software module; and

- also to confirm that any subsequent enhancements or upgrades made to the customised computer software would qualify for capital allowance under the Rules.

Feedback from IRBM:

Based on P.U.(A) 274/2019, the development cost for software specifically refers to expenses incurred in developing new software or enhancing existing software for use in business purposes.

Please refer to Practice Note No. 2/2020 (“Practice Note”).

Issue 2:

‘Under rule 2, “development cost for customised computer software” means “consultation fee, payment for rights of software ownership and incidental fee relating to the development of customised computer software’.

CTIM urged IRBM to clarify the following:-

a. If “payment for rights of software ownership‘ is intended to cover all types of software licensing fees.

Feedback from IRBM:

Payment refers only to the right to exclusively use the software, where the payment enables the software to be used in business for the first time.

Periodic software licensing fees are eligible for income tax deduction under subsection 33(1) of the Income Tax Act 1967.

b. If “incidental fee relating to the development of customised computer software” would include testing and commissioning expenses, reimbursement/out-of-pocket expenses such as accommodation and travelling expenses.

Feedback from IRBM:

Please refer to Practice Note No. 2/2020 (“Practice Note”).

c. Based on the Public Ruling (PR) No. 12/2014 on ‘Qualifying Plant and Machinery for Capital Allowances’, the payment for developing software, such as consulting fees, right to use the software such as licence fees, and other incidental charges do not qualify as plant and hence not eligible for capital allowance.

CTIM suggested that:

- this PR be amended accordingly following the gazette of P.U. (A) 274/2019; and

- further clarification and examples should be provided in the PR to address the application of the Rules.

Feedback from IRBM:

This matter is duly noted.

However, the LHDNM believes that Practice Note No. 2/2020 (“Practice Note”) has already clarified tax treatments related to this issue.

Disclaimer:

The articles, templates, and other materials on our website are provided only for your reference.

While we strive to ensure that the information presented is current and accurate, we cannot guarantee the completeness, reliability, suitability, or availability of the website or its content, including any related graphics. Consequently, any reliance on this information is entirely at your own risk.

If you intend to use the content of our videos and publications as a reference, we recommend that you take the following steps:

- Verify that the information provided is current, accurate, and complete.

- Seek additional professional opinions, as the scope and extent of each issue, may be unique.

免责声明:

我们网站上的文章、模板和其他材料只供参考。

虽然我们努力确保所提供的信息是最新和准确的,但我们不能保证网站或其内容,包括任何相关图形的完整性、可靠性、适用性或可用性。因此,您需要承担使用这些信息所带来的风险。

如果你打算使用我们的视频和出版物的内容作为参考,我们建议你采取以下步骤:

- 核实所提供的信息是最新的、准确的和完整的。

- 寻求额外的专业意见,因为每个问题的范围和程度,可能是独特的。

Keep in touch with us so that you can receive timely updates

请与我们保持联系,以获得即时更新。

1. Website ✍️ https://www.ccs-co.com/ 2. Telegram ✍️ http://bit.ly/YourAuditor 3. Facebook ✍

- https://www.facebook.com/YourHRAdvisory/?ref=pages_you_manage

- https://www.facebook.com/YourAuditor/?ref=pages_you_manage

4. Blog ✍ https://lnkd.in/e-Pu8_G 5. Google ✍ https://lnkd.in/ehZE6mxy

6. LinkedIn ✍ https://www.linkedin.com/company/74734209/admin/