Today we will discuss an interesting topic related to the Income Tax Act of 1967 and a specific exemption order.

This may be relevant if you’re a business owner or interested in tax matters! Let’s dive right in.

Our question for today is: What is the Income Tax (Exemption) (No. 6) Order 2019 [P.U. (A) 162/2019]?

We need to refer to the Income Tax Act 1967, specifically paragraph 127(3)(b) to answer this question. But before we proceed, let’s clarify a few key points.

The Income Tax (Exemption) (No. 6) Order 2019 is an order made by the Minister, exercising the powers conferred by paragraph 127(3)(b) of the Income Tax Act 1967, which was gazetted on 7 June 2019.

The order is deemed to have come into operation from the year of assessment 2016.

This means that the provisions and exemptions outlined in the order apply to the income derived from export sales during the basis period for the year of assessment 2016 and onwards.

Exemption

Now that we have a general understanding of the Order, let’s explore the exemptions mentioned within it.

Paragraph 3(1) of the Order highlights that the Minister exempts a qualifying company from paying income tax.

However, this exemption is specifically granted to a qualifying company that achieves an increase in export sales of agricultural produce or product from manufacturing. Certain conditions must be met to be eligible for this exemption, as specified in Paragraph 3(2) of the order. Firstly, at least 60% of the issued share capital of the qualifying company must be owned directly by Malaysian citizens. This condition ensures that the benefits of the exemption primarily go to companies with significant local ownership and involvement.

Secondly, the agricultural produce must be planted, reared, or caught by the qualifying company itself. This requirement ensures that the exemption applies to companies involved in producing and cultivating agricultural products. Lastly, the product from manufacturing must be manufactured by the qualifying company. This condition ensures that the exemption applies to companies engaged in the manufacturing sector.

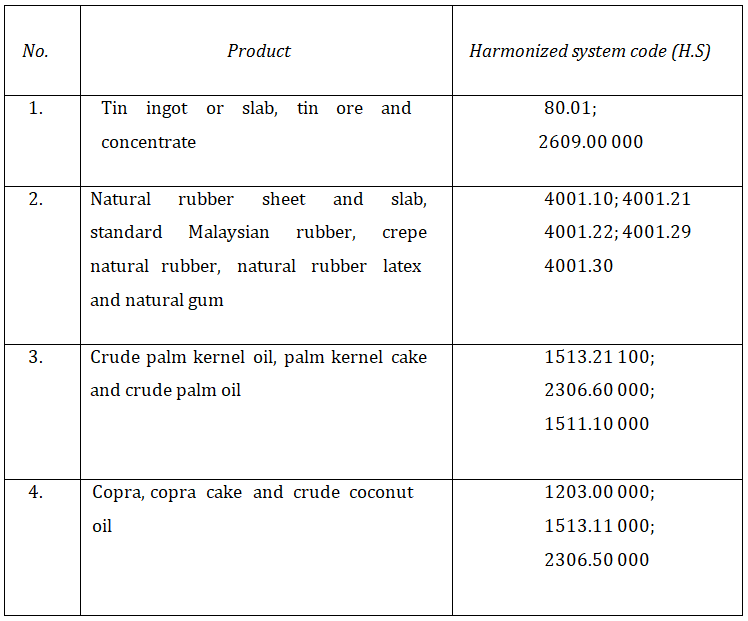

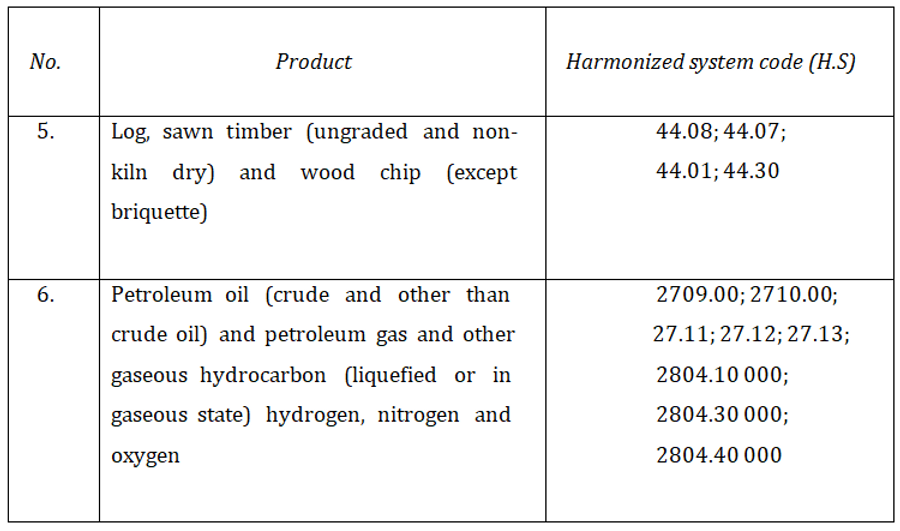

However, I would like to point out that the exemption under Paragraph 3(1) does not apply to the export of certain products as below:-

- product from manufacturing which is subject to the prohibition of exports under the Customs Act 1967; and

- product from manufacturing which is listed in the Schedule below:-

Amount of income to be exempted

The amount of income to be exempted depends on certain conditions and percentages related to increased exports of manufacturing products and agricultural produce.

Here’s a breakdown of the criteria:

- For manufacturing products:

- If the manufacturing product exported attains at least 30% of the value added, 10% of the value of increased exports will be exempted.

- If the manufacturing product exported attains at least 50% of the value added, 15% of the value of increased exports will be exempted.

- For agricultural produce:

- 10% of the value of increased exports of agricultural produce will be exempted.

However, it’s important to note that the amount of income exempted should not exceed 70% of the statutory income of the qualifying company for a year of assessment.

These exemptions and incentives are part of Malaysia’s export incentives regime to encourage exporting manufactured products and agricultural produce.

Determination of the value of increased exports

The determination of the value of increased exports for the purpose of calculating the exemptions is outlined as follows:

- If both basis periods of the qualifying company are twelve months and end on the same date:

- The value of increased exports is calculated as the difference between the free-on-board (FOB) value of export sales in the current basis period and the FOB value of export sales in the immediately preceding basis period.

- If the basis periods of the qualifying company are not twelve months and do not end on the same date due to a change in the basis period or the company being newly incorporated:

- The value of increased exports is the difference between the average FOB value of export sales in the current basis period and the average FOB value of export sales in the immediately preceding basis period.

Notably, the value of FOB export sales in a basis or immediately preceding basis period should not be equal to zero.

Interpretation

In this Order—

“export” means direct export from Malaysia of agricultural produce or product from manufacturing but does not include:-

- sales to any company in an area declared as free zones under the Free Zones Act 1990 [Act 438];

- sales to any company which is granted a licence for warehousing or a licence to carry on any manufacturing process under section 65 or 65A of the Customs Act 1967 [Act 235], as the case may be; and

- sales to any company within Langkawi, Labuan or Tioman;

“agricultural produce” means fresh and dried fruits, fresh and dried flowers, and ornamental plants, and includes ornamental fish, frozen raw prawns, frozen cooked and peeled prawns, frozen raw cuttlefish and frozen raw squid;

“manufacturing” has the meaning assigned to it in paragraph 9 of Schedule 7A to the Act;

“qualifying company” means a company incorporated under the Companies Act 2016 [Act 777] and resident in Malaysia.

Insufficiency of income

If a qualifying company cannot be granted full exemption or any exemption in a specific year of assessment due to the absence or insufficiency of statutory income, there are provisions for granting exemptions in subsequent years. Here are the key points:

- If the exemption cannot be granted or can only be partially granted in the current year of assessment due to insufficient statutory income, the unexempted portion of the statutory income can be carried forward to the first subsequent year of assessment.

- In the first subsequent year of assessment and subsequent years, the unexempted portion of the statutory income can be exempted until the total exemption granted under paragraph 3 (presumably referring to the applicable exemption scheme) is reached.

- The exemption granted in each subsequent year of assessment should not exceed seventy percent of the statutory income for that particular year of assessment.

This provision allows for the deferral of exemption when there is an absence or insufficiency of statutory income, ensuring that the qualifying company can still receive exemptions once its income meets the necessary criteria.

It is important to consult the specific tax regulations and guidelines applicable in the relevant jurisdiction to fully understand the implications and procedures related to the insufficiency of income and subsequent exemptions.

Revocation

The Income Tax (Allowance for Increased Exports) Rules 1999 [P.U. (A) 128/1999] is revoked.

P.U.(A) 128/1999 is applicable to the exemptions claimed until June 7, 2019, which are relevant. Meanwhile, P.U.(A) 162/2019 is applicable to exemptions claimed after June 7, 2019.

Conclusion

The Order state that at least 60% of the issued share capital of the qualifying company is to be owned directly by Malaysian citizen.

Even though the previous exemption orders do not preclude companies with corporate shareholders from enjoying these incentives, for example, P.U. (A) 128/1999 only requires the claimant company to be a tax resident in Malaysia, and P.U. (A) 158/2005 requires the claimant company to be at least 60% Malaysian-owned (without precluding companies with Malaysian corporate shareholders).

But based on the criteria stated on the Oder, a company which is indirectly owned by Malaysian citizens (at least 60% of the shares through another company) would not qualify for the claim of allowance for increased exports.

We’d like to encourage readers to read the full context of the Income Tax (Exemption) (No. 6) Order 2019 to better understand its implications.

The order can be downloaded by clicking the attachment below:

P.U. (A) 162/2019

By reviewing the full context, readers can gain understanding provisions outlined in the order and how they may apply to their situation.

This Order is part of Malaysia’s export incentives regime aimed at incentivising the increase in export volume and improving the quality of exports.

You should seek advice from a qualified tax professional for specific details and calculations related to your qualifying company.

Disclaimer:

The articles, templates, and other materials on our website are provided only for your reference.

While we strive to ensure that the information presented is current and accurate, we cannot guarantee the completeness, reliability, suitability, or availability of the website or its content, including any related graphics. Consequently, any reliance on this information is entirely at your own risk.

If you intend to use the content of our videos and publications as a reference, we recommend that you take the following steps:

- Verify that the information provided is current, accurate, and complete.

- Seek additional professional opinions, as the scope and extent of each issue, may be unique.

免责声明:

我们网站上的文章、模板和其他材料只供参考。

虽然我们努力确保所提供的信息是最新和准确的,但我们不能保证网站或其内容,包括任何相关图形的完整性、可靠性、适用性或可用性。因此,您需要承担使用这些信息所带来的风险。

如果你打算使用我们的视频和出版物的内容作为参考,我们建议你采取以下步骤:

- 核实所提供的信息是最新的、准确的和完整的。

- 寻求额外的专业意见,因为每个问题的范围和程度,可能是独特的。

Keep in touch with us so that you can receive timely updates

请与我们保持联系,以获得即时更新。

1. Website ✍️ https://www.ccs-co.com/

2. Telegram ✍️ http://bit.ly/YourAuditor

3. Facebook ✍

- https://www.facebook.com/YourHRAdvisory/?ref=pages_you_manage

- https://www.facebook.com/YourAuditor/?ref=pages_you_manage

4. Blog ✍ https://lnkd.in/e-Pu8_G

5. Google ✍ https://lnkd.in/ehZE6mxy

6. LinkedIn ✍ https://www.linkedin.com/company/74734209/admin/