What?

The International Standard on Quality Management 1 (ISQM 1) – Quality Management for Firms that Perform Audits or Reviews of Financial Statements, or Other Assurance or Related Services Engagements strengthens firms’ quality management systems by taking a robust, proactive, and effective approach to quality management.

The standard encourages firms to design a system of quality management that is adapted to the specific nature of the firm as well as the engagements that it undertakes.

ISQM 1 replaces the standard ISQC 1, Quality Control for Firms that Perform Audits and Reviews of Financial Statements and Other Assurance and Related Services Engagements.

Who needs to meet ISQM standards?

It applies to all firms that perform audits or reviews of financial statements or other assurance or related services engagements (i.e., if the firm performs any of these engagements, ISQM 1 applies to manage quality for those engagements).

ISQM 1 allows audit firms to review their existing quality control systems to determine the relevant risks that impact audit quality and devise and put into practice procedures that are most effective at addressing those risks.

ISQM 1 允许审计事务所审查其现有的质量控制体系,以确定影响审计质量的相关风险,并设计和实施最有效的程序来应对这些风险。

When?

Firms are required to have their system of quality management designed and implemented by December 15, 2022.

How?

ISQM 1 addresses, among other matters:

- The firm demonstrating a commitment to quality through its culture which exists throughout the firm – includes recognizing and reinforcing:

- The firm’s role in serving the public interest by consistently performing quality engagements

- The importance of quality in the firm’s strategic decisions and actions, including those related to the firm’s financial and operational priorities

- The roles, responsibilities and accountability of leadership, leadership’s qualifications, and undertaking performance evaluations of leadership annually

Components of ISQM 1

A quality management system should function in a way that is continuous and iterative, and it should be responsive to changes in the nature of the firm as well as the circumstances in which it is engaged.

In addition to this, its operations are not conducted in a linear way.

Nevertheless, for the purposes of ISQM 1, a system of quality management addresses the eight components as follows:

- The firm’s risk assessment process

- Governance and leadership

- Relevant ethical requirements

- Acceptance and continuance of client relationships and specific engagements

- Engagement performance

- Resources

- Information and communication

- The monitoring and remediation process

System of Quality Management (SOQM)

The SOQM is the mechanism that creates an environment that enables and supports engagement teams in performing quality engagements. It helps the firm achieve consistent engagement quality because it focuses on how the firm manages the quality of engagements performed.

Similar to any system of internal control, the SOQM needs to have a purpose. The purpose is important for designing the SOQM and determining whether the SOQM is effective (i.e., whether it achieved its purpose).

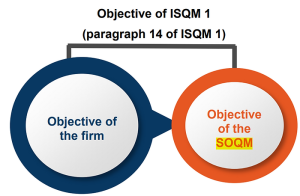

Therefore, paragraph 14 of ISQM 1 includes both the objective of the firm and the objective of the SOQM.

The objective of a Firm [paragraph 14 of ISQM 1]

Paragraph 14 of ISQM 1 includes the firm’s objective in managing quality, which is to design, implement and operate a SOQM. Similar to any system of internal control, the SOQM needs to have a purpose. The purpose is important for designing the SOQM and determining whether the SOQM is effective (i.e., whether it achieved its purpose).

The objective of the SOQM [paragraph 14 of ISQM 1]

is to provide the firm with reasonable assurance that:

- The firm and its personnel fulfil their responsibilities in accordance with professional standards and applicable legal and regulatory requirements, conduct engagements in accordance with such standards and requirements; and

- Engagement reports issued by the firm or engagement partners are appropriate.

Hence, the objective of the SOQM is explicitly used in the requirements of ISQM 1 as follows:

- The firm uses it to determine whether additional quality objectives need to be established (paragraph 24 of ISQM 1).

- It is used to conclude whether the SOQM provides the firm with reasonable assurance that its objectives of the SOQM have been achieved (paragraph 54 of ISQM 1).

In a forthcoming post, we will delve more into these standards and their implications on audit firms.

ISQM 1 explains that reasonable assurance is not an absolute level of assurance because there are inherent limitations of a SOQM. Such limitations include the fact that human judgment in decision-making can be faulty and that breakdowns in the SOQM may occur, for example, due to human error, behaviour, or failures in information technology (IT) applications.

Our website's articles, templates, and material are solely for you to look over. Although we make every effort to keep the information up to date and accurate, we make no representations or warranties of any kind, either express or implied, regarding the website or the information, articles, templates, or related graphics that are contained on the website in terms of its completeness, accuracy, reliability, suitability, or availability. Therefore, any reliance on such information is strictly at your own risk.

Keep in touch with us so that you can receive timely updates |

要获得即时更新,请与我们保持联系

1. Website ✍️ https://www.ccs-co.com/ 2. Telegram ✍️ http://bit.ly/YourAuditor 3. Facebook ✍

- https://www.facebook.com/YourHRAdvisory/?ref=pages_you_manage

- https://www.facebook.com/YourAuditor/?ref=pages_you_manage

4. Blog ✍ https://lnkd.in/e-Pu8_G 5. Google ✍ https://lnkd.in/ehZE6mxy

6. LinkedIn ✍ https://www.linkedin.com/company/74734209/admin/