A partnership agreement is a legal agreement that dictates the Partnership’s operations.

合伙协议是合伙企业规定运作的一项法律协议。

While this is not mandatory by the Partnership Act 1961, avoiding a partnership agreement can lead to significant complications in the future.

Contents in Partnership Agreement

Since a formal agreement is not required, there is no clear list of what it should include, but it usually covers the followings:-

- Contribution to capital

- Management of the business

- Distribution of profits

- Apportionment of losses

- Remuneration for acting in the partnership business

- Introduction of the new partner

- Change in the nature of the partnership business

- Partnership property

If the partnership agreement is silent or in the absence of a partnership agreement, then the rights of the partners are implied from the provisions of the Partnership Act 1961.

虽然这不是《1961年合伙企业法令》的强制性规定,但对合伙协议视而不见是有可能会导致未来产生麻烦的问题。

合伙协议的内容

- 对资本的贡献

- 企业的管理

- 利润的分配

- 损失的分担

- 从事合伙业务的报酬

- 引入新合伙人

- 合伙业务性质的改变

- 合伙财产

如果合伙协议未作规定,又或者是没有合伙协议,那么合伙人的权利就隐含在《1961年合伙企业法令》的规定中。

Therefore, it is recommended that the terms agreed upon by the partners be spelt out in a partnership agreement.

It can lessen the likelihood of costly and contentious issues in the future.

因此,建议在合伙协议中详细说明合伙人商定的条款。

这可以减少将来出现昂贵和有争议的问题的可能性。

The partnership agreement is frequently quite intricate but, in practice, it generally will not go beyond the following:-

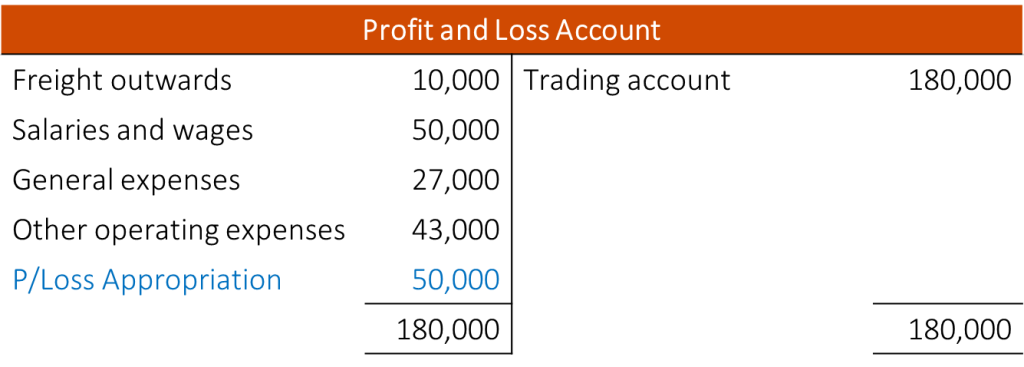

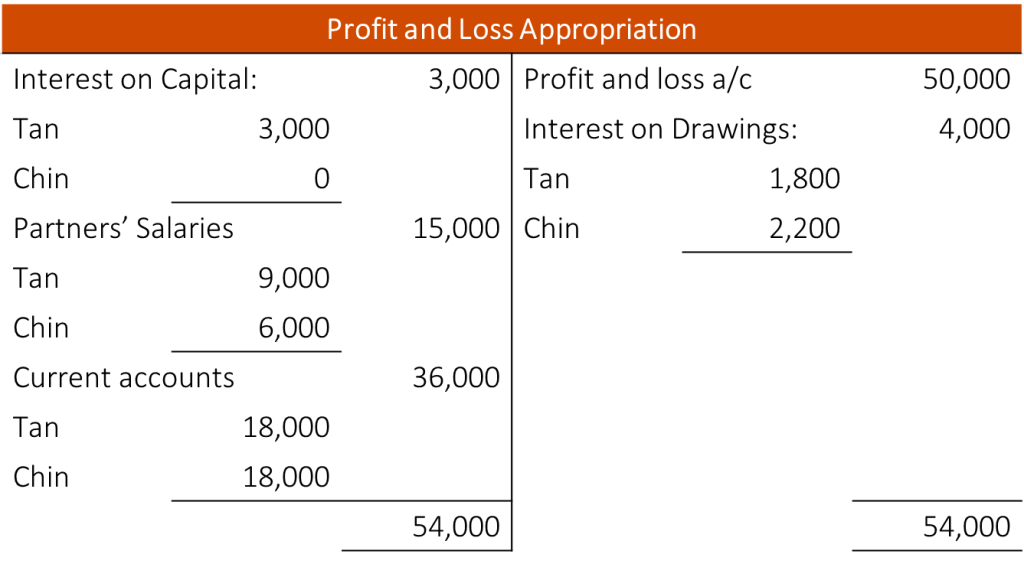

Appropriations of Profit

The proprietor’s share of a sole proprietorship’s profit for the year is credited to the capital account at the end of the year (the double entry is completed by a debit entry in the profit or loss account, resulting in a nil balance on that account).

A partnership needs an additional accounting account known as an “Appropriation Account.”

The partnership’s Profit and Loss Account will still be debited, but the profit will now be credited to the Appropriation Account rather than the capital account.

Illustration:

合伙协议往往相当复杂,但在实践中一般不会超过以下内容:-

拨款账户

对于独资企业的经营者来说,在该年度(一般在年底)结帐时,将利润份额记入资本账户(通过在损益账户中的借方分录完成双重分录,从而使该账户的余额为零)。

然而合伙企业却需要一个额外的会计账户,称为 “拨款账户”。

合伙企业的损益账户仍将被借记 (Debit),然后把利润记入拨款账户(而不是资本账户)。

示例:

Partners’ Salaries

The term salaries are in some senses a misunderstanding.

Employee salaries are business expenses that are deducted just from the profit or loss account, consequently reducing annual profit.

However, because partners are the business’s owners, any sums paid to them pursuant to the partnership agreement are included in their share of the profit.

As the amount is guaranteed, it must be handled via a credit entry in the partner’s account (often the current account) prior to the distribution of the residual profit.

A debit entry to the Appropriation Account completes the double entry.

Illustration:

In the absence of a Partnership Agreement

According to the Partnership Act 1961, in the absence of a partnership agreement, partners are not entitled to interest on capital or salaries

合伙人的薪金

薪金一词在某种意义上是一种误解。

雇员的薪金是商业支出,是从损益表中扣除,从而减少年度利润。

然而,由于合伙人是企业的所有者,根据合伙协议支付给他们的任何款项都包括在他们的利润份额中。

由于该金额是有保证的,因此在分配剩余利润之前,必须通过合伙人账户(通常是往来账户)的贷方分录来处理。

拨款账户的借方分录完成了双重分录。

示例:

在没有合伙协议的情况下

根据《1961年合伙企业法令》,在没有合伙协议的情况下,合伙人无权获得资本利息或薪金

Interest on Capital

By choosing to invest their money in the partnership rather than pursuing other investment opportunities, partners are rewarded with interest payments on the cash they contribute.

As a result, the amount of profit that is available to be shared following the profit and loss sharing ratio is decreased after interest is paid,

Illustration:

Because of this, the Appropriation Account will require a debit entry to be made in it.

A credit entry in the Current Account of the partner to whom the interest is paid completes the double-entry by transferring money into that account.

Illustration:

In the absence of a Partnership Agreement

According to the Partnership Act 1961, in the absence of a partnership agreement, partners are not entitled to interest on capital or salaries

Even though the balances on the current accounts are technically a part of the total capital balance, it is common practice to exclude them from the amount of capital that is entitled to interest payments.

The partners’ capital balances are the only ones subject to the calculation and payment of interest. However, most partners in partnerships in Malaysia are not in the habit of charging interest on their capital to the company.

资本利息

通过选择将他们的钱投资于合伙企业,而不是追求其他投资机会,合伙人享有为相关资金支付利息的回报。

因此,在支付了利息后,合伙企业按照损益分担比例可供分享的利润数额将会减少。

示例:

因此,拨款帐户将需要在其中进行借记分录。 向其支付利息的合作伙伴的往来账户中的贷方分录通过将资金转入该账户来完成复式分录。

示例:

在没有合伙协议的情况下

根据《1961年合伙企业法令》,在没有合伙协议的情况下,合伙人无权获得资本利息或薪金

尽管从技术上讲,往来账户的余额是总资本余额的一部分,但通常的做法是将它们从享有支付利息的资本额中排除。

合伙人的资本余额才是唯一需要计算和支付利息的,然而一般上,马来西亚大部分合伙企业的合伙人都没有向公司收取资本利息的习惯。

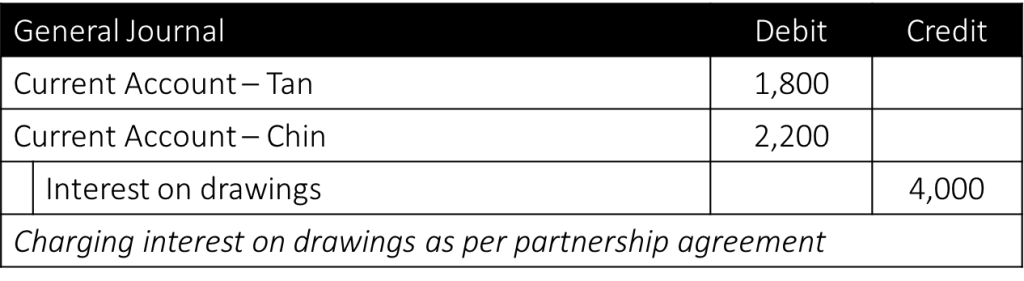

Interest on Drawings

By charging interest on drawings, business partners can be dissuaded from drawing out excessive amounts of money from the company.

Given this information, it is reasonable to conclude that the interest on drawings should be recorded as a debit entry in the partners’ current accounts and as a credit entry in the appropriation account.

Illustration:

Illustration:

It is important to keep in mind that each of these appropriations must be resolved before the residual profit can be divided among the partners.

提款的利息

通过对提款收取利息,可以防止阻商业伙伴从公司提取过多的资金。

鉴于这些信息,我们有理由得出结论,提款利息应该作为借方分录记录在合伙人的往来账户中,作为贷方分录记录在拨款账户中。

示例:

示例:

重要的是要记住,在剩余的利润可以在合伙人之间分配之前,这些拨款必须逐一解决。

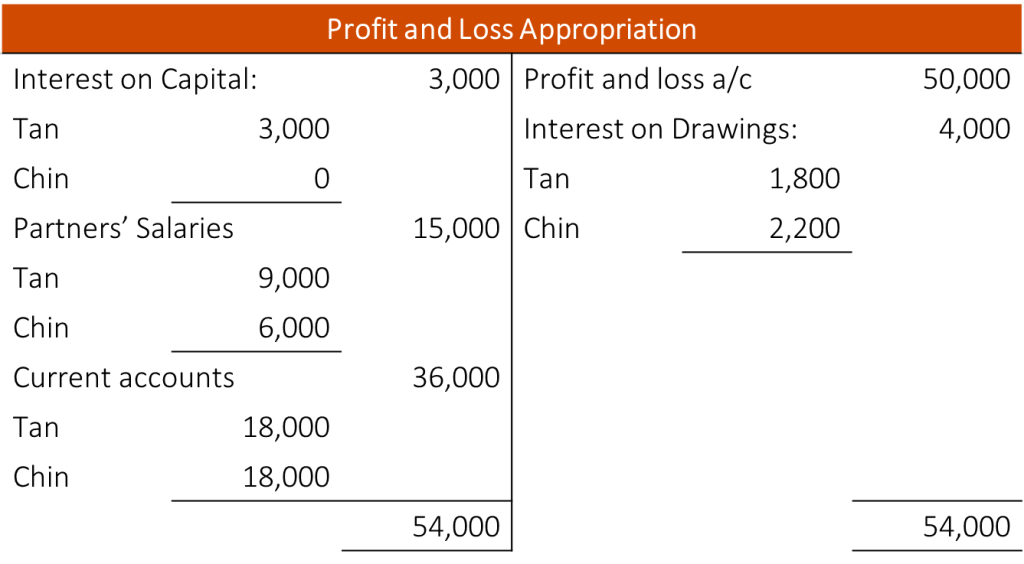

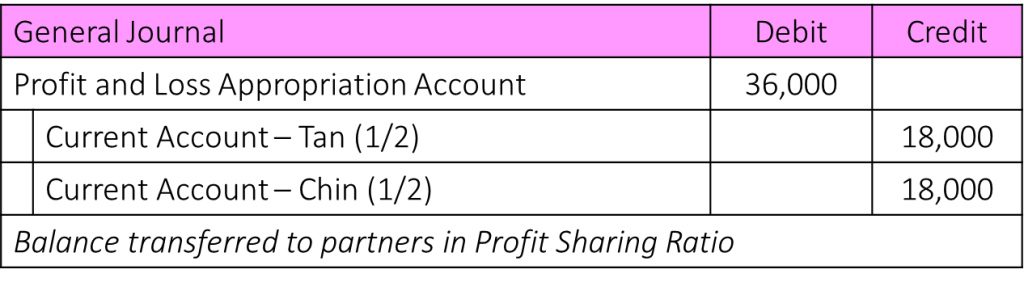

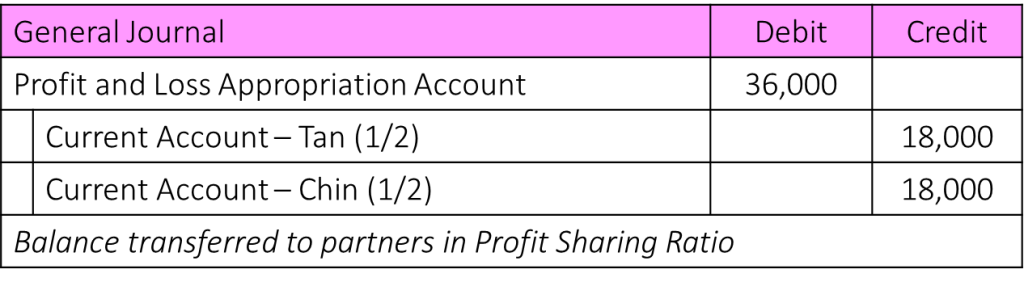

Share of Residual Profit

Once all other appropriations have been made, this is the amount of profit that is still available to be split among the partners according to the predetermined profit and loss sharing ratio.

Accountants need to be aware that there is a distinction to be made between the profit for the year (income minus expenses), which is determined in the exact same way as for a sole proprietorship, and the residual profit (the remaining profit after profit for the year has been adjusted by the appropriations in accordance with the partnership agreement).

剩余利润

一旦所有其他拨款都已完成,这就是可根据预先确定的损益分担比例在合伙人之间分配的利润数额。

会计师需要注意的是,当年的利润(收入减去支出)和剩余利润(当年的利润按照合伙协议的拨款调整后的剩余利润)之间是有区别的,后者的确定方式与独资企业完全相同。

Example:

As each appropriation is processed, entries are made in both the Appropriation Account and the partner’s Current Account to complete the double-entry (if the partnership does not maintain Current Accounts, the entries will be made in the Capital Accounts).

Illustration:

Illustration:

在处理每笔拨款时,拨款账户和合伙人的往来账户都要有分录,以完成复式记账(如果合伙企业不保持往来账户,分录将在资本账户中进行)。

示例:

示例:

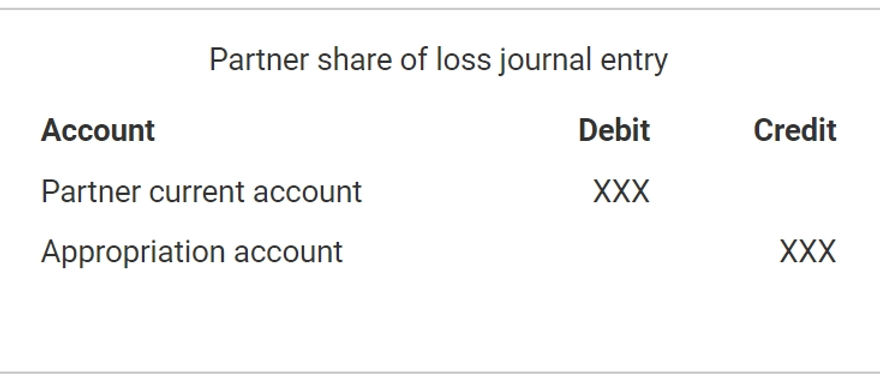

One last thing to consider in this scenario is that the profit that is supposed to be shared among the partners will become a loss if the overall amount of the appropriations is more than the profit for the year.

Because of this, the entries made for the partner’s portion of the residual profit will be credits in the appropriation account (which will result in the account having a zero balance) and debits in the partners’ current accounts.

在这种情况下需要考虑的最后一件事是,如果拨款总额超过当年的利润,那么本应由合伙人分享的利润将成为亏损。

正因为如此,合伙人剩余利润部分的分录将是拨款账户的贷方(这将导致该账户的余额为零)和合伙人经常账户的借方。