This is a stamp duty appeal under s 39(1) of the Stamp Act 1949 (“the Act”) made by way of a Case Stated under s 39(2) of the Act.

Plaintiff is seeking for inter alia a declaration that the Notice of Stamp Duty Assessment dated 13 February 2019 issued by Defendant (“the assessment”) is erroneous, null and void.

Stamp Act

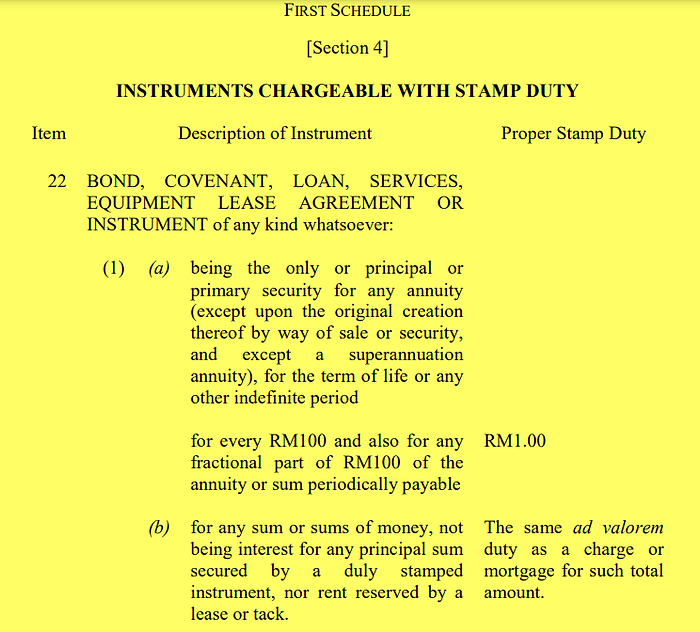

Sub-item 22(1) of the First Schedule of the Act, upon being amended by the Finance Act 2018, states the following:

[Emphasis Added]

The Remission Order

Paragraph 2 of the Stamp Duty (Remission) (No 2) Order 2012 (the “Remission Order”) states that:

The amount of stamp duty that is chargeable under sub-subitem 22(1)(b) of the First Schedule to the Act upon a loan agreement or loan instrument without security for any sum or sums of money repayable on demand or in single bullet payment under that sub-subitem which is in excess of zero point one per cent (0.1%) is remitted.

The Court has been asked to provide its opinion under section 39(1) of the Act on whether the Letter of Offer, signed between the Plaintiff and the financial institution on 27 December 2018, is covered by the Remission Order.

Brief Facts

The Plaintiff received a Letter of Offer from a Bank on 27 December 2013, which offered a credit of RM105,000,000.00.

When Plaintiff submitted the Letter of Offer to Defendant on 31 January 2019, they were informed that the document did not qualify for remission of stamp duty under the Remission Order.

Shortly thereafter, on 13 February 2019, Plaintiff received a Notice of Stamp Duty Assessment from Defendant. Unhappy with the assessment, Plaintiff paid the stamp duty under protest under section 38A(7) of the Act on 14 February 2019 and 11 February 2019.

Finally, on 28 February 2019, Plaintiff’s previous solicitors filed a notice of objection against the assessment under section 38A of the Act.

Letter of Offer

The specific condition for repayment is stated in the Letter of Offer as follows:

“SPECIFIC CONDITIONS FOR TF

i) Repayment Notwithstanding any other provisions herein stated related to the availability of the Facility or any part thereof, the Bank reserves the right to recall/cancel the facility or any part thereof at any time it deems fit without assigning any reason thereto by giving written notice of the same, whereupon the facility of such part thereof shall be cancelled and the whole indebtedness or such part thereof be repayable on demand.

………….

2. Forward Foreign Exchange (“Forex”)

Specific Condition: Repayment

Notwithstanding any other provisions herein stated related to the availability of the Facility or any part thereof, the Bank reserves the right to recall/cancel the facility or any part thereof at any time it deems fit without assigning any reason thereto by giving written notice of the same, whereupon the facility of such part thereof shall be cancelled and the whole indebtedness or such part thereof be repayable on demand.”

[Emphasis Added]

The Defendant’s Contentions

Defendant takes the position that there is no error in the assessment and the Letter of Offer was correctly charged to stamp duty under Item 22(1)(a) of the First Schedule of the Act, and the Remission Order is therefore not applicable to the Letter of Offer.

It is contended that the Letter of Offer does not spell out the sums of money that must be paid by way of demand or single bullet payment and is, therefore, liable to stamp duty as a loan agreement or loan instrument under Item 22(1)(a) First Schedule of the Act.

The Plaintiffs Contentions

The plaintiff assumes that the Letter of Offer clearly states that the loan instrument has no security and must be repayable on demand or in a single bullet payment.

They believed that the Letter of Offer they had accepted from the Bank was eligible for remission of the stamp duty in excess of 0.1%.

It is contended that the correct approach to be adopted in interpreting a taxing statute is that it should be given a strict interpretation by giving their plain, natural and ordinary meaning, and no intendment can be made in favour of tax liability.

The Decision of the High Court

The defendant ought to give the Remission Order its plain and ordinary meaning as it is trite law that strict interpretation of taxing statutes must be given.

In National Land Finance Co-operative Society Ltd v. Director General of inland Revenue [1993], the Supreme Court had held that:

“…in a taxing Act, one has to look merely at what is clearly said. There is no room for any intendment. There is no equity in a tax. There is no presumption as to a tax.

Nothing is to be read, nothing is to be implied. One can only look fairly at the language used… ”

It means that when interpreting a legal document or statute, one should only consider the plain and explicit meaning of the words used without inferring any additional meaning or intent beyond what is stated in the document’s language.

This approach requires a strict and literal interpretation of the document without considering any contextual or extraneous information or assumptions about the situation or intent of the parties involved. Essentially, the statement emphasises the importance of sticking to the text of a document and avoiding any subjective or speculative interpretations.

The Court finds that the Letter of Offer and the Remission Order are clear, and there is no room for this Court to re-write and change the meaning of the Letter of Offer and the Remission Order, which are clear and unambiguous.

The High Court is making a distinction between two different items in the First Schedule of the Act, specifically item 22(1)(a) and item 22(1)(b).

The court notes that the material difference between these two items is that item 22(1)(a) applies to bonds, covenants, or instruments within a specific and defined period of time, which allows the total amount payable to be determined.

On the other hand, item 22(1)(b) applies to bonds, covenants, or instruments that have an indefinite period of time, such as for the term of life.

The High Court is highlighting this distinction to provide clarity and guidance in the interpretation and application of the relevant provisions of the Act.

The Court has examined the Letter of Offer in question and has identified a clause that gives the Bank the right to recall or cancel the facility or any part of it at any time.

Suppose the Bank decides to exercise this right. In that case, the relevant facility or part of it will be cancelled, and the borrower will be required to repay the entire indebtedness or the relevant part thereof on demand.

This clause effectively means that the loan is repayable on demand or in a single bullet payment, as there is no definite or certain period for repayment. This finding is relevant to the interpreting Stamp Duty (Remission) (No. 2) Order 2012, which provides for the remission of stamp duty for certain loan instruments.

The High Court found no definite or certain period of time prescribed under the LO for the TF and Forex. It held that the LO fell under item 22(1)(b), thus qualifying for the remission of stamp duty under the Remission Order.

It is considered that Defendant has no legal or factual basis in contending that the Letter of Offer is subject to sub-item 22(1)(a) First Schedule of the Act.

As a result, the High Court rejected the defendant’s contention that the LO did not contain any specific provision on how the loan repayment would be made in the ordinary course.

Reference

5 games to keep employees of CCS & Co Plt – Chartered Accountants and Bispoint Group of Accountants connected.

We put a lot of emphasis on ensuring that our team members enjoy a balanced life outside work.

Hence, our firm’s Sports and Social Committee is responsible for actively organising an exciting variety of events, such as the Annual Dinner, Annual Trips and Inter-accounting Firm Tournament.

These events are planned so that our professionals can take some time off to relax and, more importantly, come together to strengthen their sense of community and teamwork.

This year’s Inter-Accounting Firm Tournament will be held on February 25 and 26, 2023 (Saturday and Sunday). We welcome your support!

5项活动让 CCS 特许会计师 和 Bispoint Group of Accountants 的员工保持联系。

我们非常重视我们的团队成员享受工作以外的平衡生活。

有鉴于此,我们公司的康乐委员会积极举办各种令人兴奋的活动,如年度晚宴、年度旅行和会计师事务所之间的比赛。

这些活动的策划是为了让我们的专业人员可以抽出一些时间来放松,更重要的是,他们可以聚在一起加强社区意识和团队精神。

今年的会计师事务所之间的比赛将于2023年2月25日和26日(星期六和星期日)举行。我们欢迎你前来支持!

Our website's articles, templates, and material are solely for you to look over. Although we make every effort to keep the information up to date and accurate, we make no representations or warranties of any kind, either express or implied, regarding the website or the information, articles, templates, or related graphics that are contained on the website in terms of its completeness, accuracy, reliability, suitability, or availability. Therefore, any reliance on such information is strictly at your own risk.

Keep in touch with us so that you can receive timely updates |

要获得即时更新,请与我们保持联系

1. Website ✍️ https://www.ccs-co.com/ 2. Telegram ✍️ http://bit.ly/YourAuditor 3. Facebook ✍

- https://www.facebook.com/YourHRAdvisory/?ref=pages_you_manage

- https://www.facebook.com/YourAuditor/?ref=pages_you_manage

4. Blog ✍ https://lnkd.in/e-Pu8_G 5. Google ✍ https://lnkd.in/ehZE6mxy

6. LinkedIn ✍ https://www.linkedin.com/company/74734209/admin/