The Inland Revenue Board of Malaysia (HASiL) has given a response to the letter that CTIM sent them on June 16th, 2023.

The letter addressed the issues that were brought up on the TAeF Portal for the Special Voluntary Disclosure Programme (SVDP) 2.0.

1. TAeF portal has no option for SVDP 2.0

in view of the above, CTIM sought clarification from HASiL:-

a) How can tax agents submit the voluntary disclosure (VD) within the SVDP 2.0 implementation period on behalf of their clients for existing taxpayers?

Feedback from HASiL:

Based on the PKPS 2.0 Frequently Asked Questions, the following are relevant categories of taxpayers that are eligible:

1) Existing taxpayers who have previously declared income to IRBM but have not submitted ITRF/ RPGTRF for any other assessment year.

Tax agents are required to submit the BNCP via e-Filing through TAeF. 2) Existing taxpayers who have previously declared income to IRBM but still have unreported additional income.

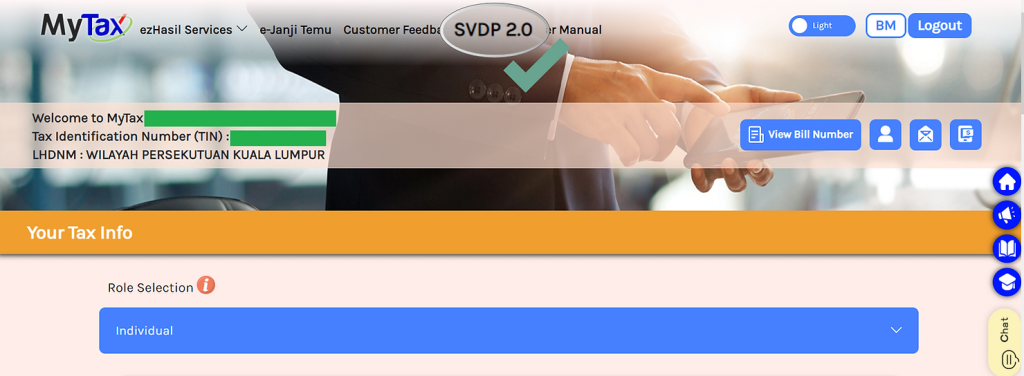

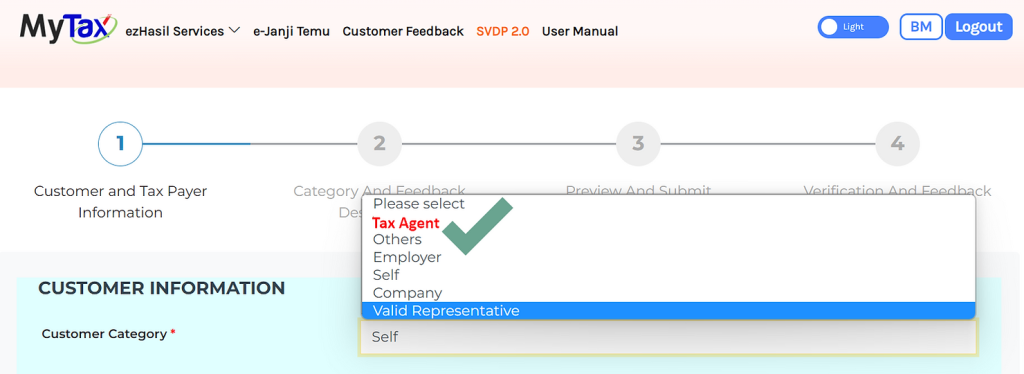

The submission of PKPS 2.0 for additional income should be made through the MyTax system, where tax agents need to log in to MyTax using their Individual ID and select the PKPS 2.0 menu under the Tax Agent category.

Tax agents must enter the correct taxpayer information and then upload the PKPS 2.0 Additional Income Reporting Form and tax computation.

Tax computation must only be submitted by taxpayers in the company, business, and partnership filing categories.

The following is a screen display for PKPS 2.0 through MyTax:

Step 1: IC No

Step 2: Password

Step 3: Click “SVDP 2.0”

Step 4: Select “Tax Agent”

b) CTIM would like to request HASiL to update the TAeF portal to include the option for submission of the SVDP 2.0 form via TAeF portal.

Feedback from HASiL:

This matter has been considered in the development of TAeF 2.0 and is expected to be available in November 2023.

C) Meanwhile, CTIM would like to request that tax agents be allowed to submit the VD to HASiL manually for new and existing taxpayers through HASiL‘s branches while HASiL updates the TAeF portal accordingly.

Feedback from HASiL:

This matter has been taken into consideration in the development of TAeF 2.0. The submission of PKPS 2.0 through e-tax agents is as follows:

New taxpayers:

Tax agents need to submit the BNCP via e-Filing through TAeF.

Existing taxpayers who have previously reported income to LHDNM but have unsubmitted BNCP for any other assessment year:

Tax agents need to submit the BNCP via e-Filing through TAeF.

Existing taxpayers who have previously reported income to LHDNM but have additional unreported income:

The submission of PKPS 2.0 for additional income needs to be done through the MyTax System. Tax agents must log in to MyTax, select the PKPS 2.0 menu, and choose the Tax Agent category as explained in answer to question 1(a) above.

2. Proposed amendment to the Operational Guidelines No. 2/2023 (GPHDN 2/2023) dated 2 June 2023 on SVDP 2.0

CTIM would like to request for HASiL‘s consideration to amend the above paragraph 5.3.5 accordingly to state that SVDP 2.0 can be submitted via the MyTax portal and the TAeF portal (and the TAeF portal to be updated accordingly).

In the meantime, to please allow manual submissions through the various HASiL branches. Feedback from HASiL: Feedback is as per question 1C. LHDNM will upload the amendment of Frequently Asked Questions on the Official Portal of LHDNM in the near future.

Disclaimer:

The articles, templates, and other materials on our website are provided only for your reference.

While we strive to ensure that the information presented is current and accurate, we cannot guarantee the completeness, reliability, suitability, or availability of the website or its content, including any related graphics. Consequently, any reliance on this information is entirely at your own risk.

If you intend to use the content of our videos and publications as a reference, we recommend that you take the following steps:

- Verify that the information provided is current, accurate, and complete.

- Seek additional professional opinions, as the scope and extent of each issue, may be unique.

免责声明:

我们网站上的文章、模板和其他材料只供参考。

虽然我们努力确保所提供的信息是最新和准确的,但我们不能保证网站或其内容,包括任何相关图形的完整性、可靠性、适用性或可用性。因此,您需要承担使用这些信息所带来的风险。

如果你打算使用我们的视频和出版物的内容作为参考,我们建议你采取以下步骤:

- 核实所提供的信息是最新的、准确的和完整的。

- 寻求额外的专业意见,因为每个问题的范围和程度,可能是独特的。

Keep in touch with us so that you can receive timely updates

请与我们保持联系,以获得即时更新。

1. Website ✍️ https://www.ccs-co.com/ 2. Telegram ✍️ http://bit.ly/YourAuditor 3. Facebook ✍

- https://www.facebook.com/YourHRAdvisory/?ref=pages_you_manage

- https://www.facebook.com/YourAuditor/?ref=pages_you_manage

4. Blog ✍ https://lnkd.in/e-Pu8_G 5. Google ✍ https://lnkd.in/ehZE6mxy

6. LinkedIn ✍ https://www.linkedin.com/company/74734209/admin/