Who should prepare Transfer Pricing Documentation?

The Transfer Price Guidelines 2012 provide additional clarification that the requirements for the preparation of contemporaneous transfer pricing documentation that the TP Rules mandate would be limited to the following:

- for a person carrying on a business, where the gross income exceeds RM25 million, and the total amount of related party transactions exceeds RM15 million; or

- in relation to financial assistance, where such financial assistance exceeds RM50 million (the Guidelines do not apply to transactions involving financial institutions).

Any person who falls outside the scope above

- may opt to fully apply all relevant guidance as well as fulfil all Transfer Pricing Documentation requirements in the Guidelines; or

- alternatively may opt to comply with TP Documentation requirements under paragraphs 25.4(a), (d) and (e) only:-

- organisational structure;

- Controlled transactions; and

- Pricing policies.

In this regard, the person can apply any method other than the five described in the Guidelines, provided it results in or best approximates arm’s length outcomes.

Guide on How to prepare a Simple Limited Transfer Pricing Document

Today we’ll look at how to prepare a simplified or limited transfer pricing document.

You are the accountant of Ever Bright Sdn. Bhd. and the Group CFO has asked you to prepare a transfer pricing document for the company.

You understand that this group comprises three companies, i.e. Ever Bright Sdn. Bhd., Everlasting Pte Ltd and Whatever Corporation Ltd.

Step 1:

You first need to determine whether the relationship between the three companies is an associated company under s 140A of the Income Tax Act 1967 or not.

You find that Whatever Corporation Ltd has the power to appoint one or more directors or BODs in Everlasting Pte Ltd and Ever Bright Sdn. Bhd.

Whatever Corporation Ltd also directs Everlasting Pte Ltd to buy finished goods from Ever Bright Sdn. Bhd.

Therefore you conclude that they are associated persons.

Step 2:

You are going to need to recognise several terms right now:

Transfer price is the price at which related parties transact with each other,

Transactions between related parties (more specifically known as associated persons) are referred to as “controlled” transactions“, as distinct from “uncontrolled” transactions between independent companies.

According to the arm’s length principle, a transfer price is acceptable if all transactions between associated parties are conducted at the arm’s length price. Arm’s length price is the price which would have been determined if such transactions were made between independent entities under the same or similar circumstances.

Step 3:

Next, you need to determine whether you need to prepare a detailed transfer pricing document as required by Rule 4(2) of the Income Tax (Transfer Pricing) Rules 2012 or whether you can choose to prepare a simplified version of the transfer pricing document as provided by the Transfer Pricing Guidelines 2012.

As a result of your inquiry, you discover the sale of Ever Bright Sdn. Bhd. is RM9,578,571, and the transaction with a related party is RM9,177,141; consequently, following the transfer pricing guidelines, you have the option of preparing a simplified version of the transfer pricing document.

Step 4: Get Ready

What you need to prepare are:-

- Organisational Structure;

- Controlled Transactions; and

- Pricing Policies.

1. Organisational Structure

It would help if you described Ever Bright Sdn. Bhd.’s worldwide organisational and ownership structure (including a global organisation chart and any substantial changes to the relationship, if any), covering all associated persons whose transactions directly or indirectly affect the pricing of the documented transactions.

It would help if you also described Ever Bright Sdn. Bhd.’s Company organisation chart.

Even though a product description does not need to be included in the simplified transfer pricing documentation for it to be legitimate, a description of the product can make it much simpler for an Inland Revenue officer to comprehend what the company is selling.

2. Controlled Transactions

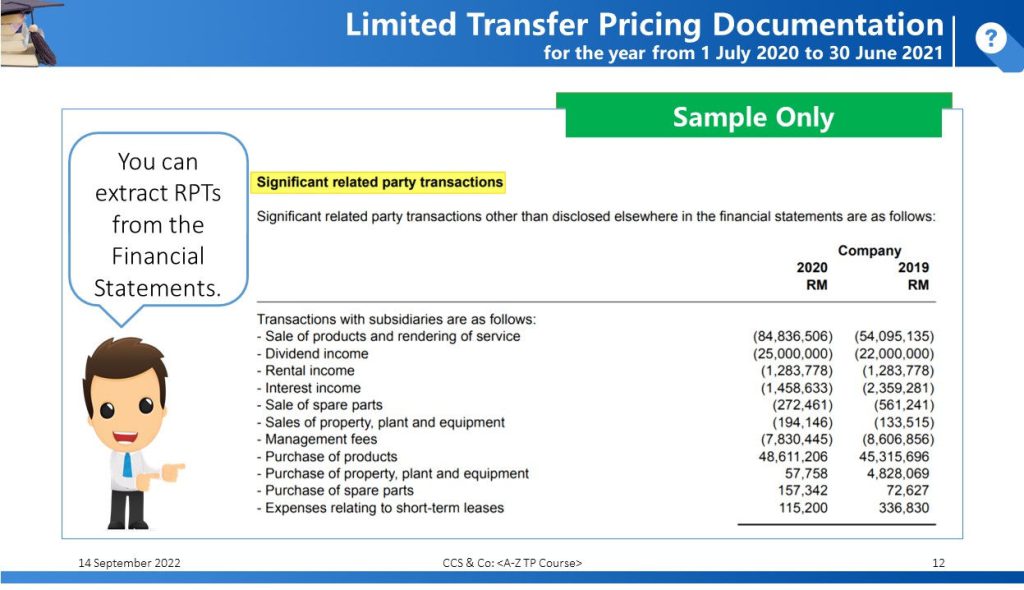

- Description of details of the property or services to which the international/domestic transaction relates; any intangible rights or property attached to it, the participants, the scope, timing, frequency, type and value of the controlled transactions (including all relevant related party dealings in relevant geographic markets);

- Names and addresses of all associated persons, with details of the relationship with each such associated person;

- The nature, terms (including prices) and conditions of international transactions (where applicable) entered into with each associated person and the quantum and value of each transaction;

- An overview description of the business, as well as a functional analysis of all associated persons with whom the taxpayer has transacted;

- All commercial agreements setting forth the terms and conditions of transactions with associated persons as well as with third parties;

- A record of any forecasts, budgets or other financial estimates prepared by the person for the business and each division or product separately.

FAR Analysis

Functions performed

Ever Bright Sdn. Bhd. supplying the manufacturing services provides the plant, machinery and labour necessary to manufacture the relevant product. Everlasting Pte Ltd (the ‘principal’) supplies the relevant raw materials and owns all the intellectual property relating to the products, such as patents and trademarks.

Under the tolling arrangement between Ever Bright Sdn. Bhd. and Everlasting Pte Ltd, raw materials for manufacturing are entirely consigned by Everlasting Pte Ltd and Ever Bright Sdn. Bhd. does not own these raw materials.

The manufacturing team of Ever Bright Sdn. Bhd. is mainly engaged in the following key activities:

- Particleboard, Furniture, and value-added wood-based products manufacturing,

- Production Planning,

- Quality Control,

- Packaging and Logistics,

- Technical Services,

- Environmental, Health and Safety

- HR and IT

- Finance

Assets employed

Ever Bright Sdn. Bhd. own assets: factory buildings, plant and machinery, furniture and fixtures, office equipment and motor vehicles.

Everlasting Pte Ltd holds all the material intellectual property rights. Accordingly, as a toll manufacturer, Ever Bright Sdn. Bhd. does not own any significant intangible assets.

No Risk, No Reward: The Risks Assumed

Ever Bright Sdn. Bhd. is not responsible for any risks caused by macroeconomic variables such as economic downturns or conditions peculiar to a particular sector. The responsibility for this risk lies with Ever Bright Sdn. Bhd.

However, if there were a fall in customer demand, Everlasting Pte Ltd would have a comparable decrease in the number of orders it processed. The possibility exists that Ever Bright Sdn. Bhd. will not fully recover its operational costs due to insufficient sales volumes.

As a result, it can be deduced that Ever Bright Sdn. Bhd. is exposed to some degree of indirect industry and market risk; nevertheless, the impact has not been particularly noteworthy during the time under consideration.

Only Everlasting Pte Ltd supplies Ever Bright Sdn. Bhd. with the raw materials used in the manufacturing processes carried out by Ever Bright Sdn. Bhd.

As a consequence of this, Ever Bright Sdn. Bhd. does not have legal ownership of these raw materials.

Any costs associated with product liability suits will, in the end, be shouldered by Everlasting Pte Ltd as principal. As a result, Ever Bright Sdn. Bhd. is not responsible for the risks associated with product responsibility and warranty.

Everlasting Pte Ltd will bear the risks associated with holding raw materials and finished goods inventory, as well as final demand and price risks.

The production risk that is connected with Ever Bright Sdn. Bhd.’s ordinary manufacturing operations are borne by the company.

The Technical Services section of Ever Bright Sdn. Bhd. manages the company’s production risk through the implementation of continuous process improvement.

Ever Bright Sdn. Bhd. sell all its finished goods to Everlasting Pte Ltd, who are unlikely to default on payment, or delay payment, hence Ever Bright Sdn. Bhd. does not bear credit and collection risk.

Ever Bright Sdn. Bhd. mainly transacts in MYR,

Functional Characterisation of Ever Bright Sdn. Bhd.

The above analysis of the functions performed includes risk assumed and assets employed by Ever Bright Sdn. Bhd. and its related party, Ever Bright Sdn. Bhd. may be characterised as a toll manufacturer in the industry.

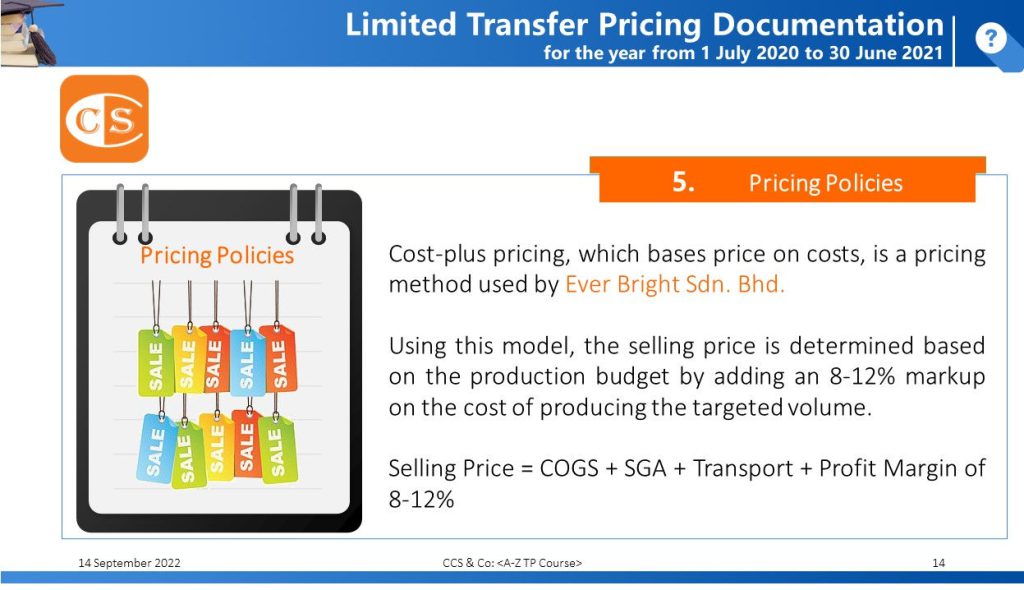

3. Pricing Policies – Paving the way for the journey ahead

The formulation of transfer pricing policies is essential to implementing transfer pricing.

The company should have a transfer pricing policy to help ensure that all of its employees are on the same page.

It is an undeniable indication that transfer pricing has been given due consideration and that it has been carried out appropriately.

It is common knowledge that a transfer pricing policy should be carefully crafted and methodically carried out because of the long-term nature of the situation.

Your company can choose from various pricing methods; however, broadly speaking, three primary pricing techniques are the most frequently used by businesses when setting their prices:-

- Cost Plus Pricing

- Competitive Based Pricing

- Value-Based Pricing

The pricing method known as “cost-plus” involves “marking up” (adding a fixed percentage) the price of the goods and services to arrive at the final selling price.

You, as the seller, would first perform a calculation considering the fixed and variable costs incurred in the production of your goods. Then you would apply the markup % to the total amount calculated.

This tactic is often utilised since it is straightforward to justify and is typically fair and non-discriminatory.

Pros:

- Less likelihood of price wars

- It can guarantee certain levels of earnings.

- Simple to implement

Cons:

- Reduces productivity and raises costs without providing any benefits.

- It is not guaranteed to pay all costs because a significant portion of the computation is based on estimations.

- When necessary, it cannot be easy to make pricing adjustments.

You have observed that the management of Ever Bright Sdn. Bhd. has adopted the cost-plus pricing approach; hence, you need to produce a description and show how the method functions.

You notice that Ever Bright Sdn. Bhd.’s management is adopting the Cost-plus pricing method; therefore, you need to describe and illustrate how it works.

Process costing is a method in which raw materials, labour, and factory overhead are charged to the main cost or department.

The costs charged to each product unit are determined by dividing the total costs charged by the main cost by the number of units produced at the main cost.

In the process costing calculation, in general, there are three required data;

- production data,

- overhead cost, and

- raw material cost.

Cost of goods sold per unit is calculated as:

- Cost of goods sold per unit = Total Cost / Equivalent Unit

With these steps, that’s it, you’ve completed a simplified version of your transfer pricing document. Congratulations!

Our website's articles, templates, and material are solely for reference. Although we make every effort to keep the information up to date and accurate, we make no representations or warranties of any kind, either express or implied, regarding the website or the information, articles, templates, or related graphics that are contained on the website in terms of its completeness, accuracy, reliability, suitability, or availability. Any reliance on such information is therefore strictly at your own risk.

Keep in touch with us so that you can receive timely updates |

要获得即时更新,请与我们保持联系

1. Website ✍️ https://www.ccs-co.com/ 2. Telegram ✍️ http://bit.ly/YourAuditor 3. Facebook ✍

- https://www.facebook.com/YourHRAdvisory/?ref=pages_you_manage

- https://www.facebook.com/YourAuditor/?ref=pages_you_manage

4. Blog ✍ https://lnkd.in/e-Pu8_G 5. Google ✍ https://lnkd.in/ehZE6mxy

6. LinkedIn ✍ https://www.linkedin.com/company/74734209/admin/