The International Auditing and Assurance Standards Board, also known as the IAASB, is responsible for setting the International Standards on Auditing (ISAs).

It is an independent body that sets international standards of high quality on aspects of:

- Auditing;

- Assurance;

- Quality Control;

- Review; and

- Related services.

The International Auditing and Assurance Standards Board were established in March 1978. Before that, it was known as the International Auditing Practices Committee (IAPC), and its activity used to be concentrated on three main areas at the time:

- Objects and scope of audits of Financial Statements;

- Engagement letters; and

- General auditing guidelines.

It is easy to see how the work of the International Auditing and Assurance Standards Board (IAASB) has dramatically progressed since 1991, when the guidelines initially developed by the International Auditing Practices Committee (IAPC) were renamed the International Standards on Auditing (ISAs).

In 2002, the IAPC changed its name to the International Auditing and Assurance Standards Board (IAASB), and the International Federation of Accountants (IFAC) approved a series of reforms. These reforms were primarily designed (among other things) to strengthen the standard-setting process, which included the operations at the IAASB.

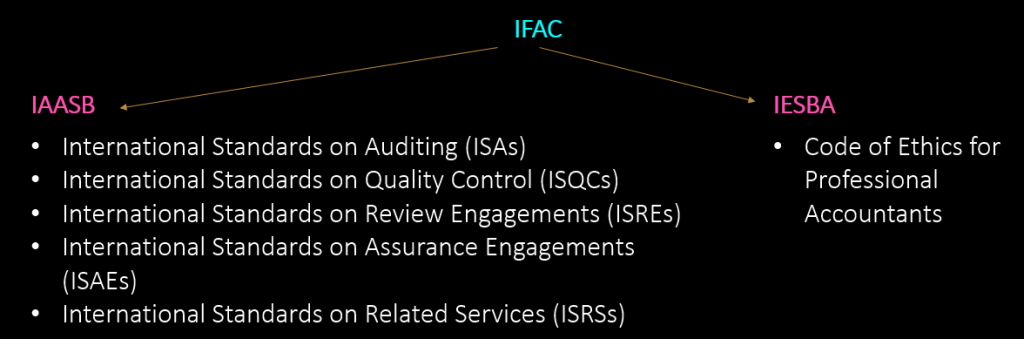

The International Auditing and Assurance Standards Board (IAASB) is a technical standing committee of the International Federation of Accountants (IFAC) that has close ties to the International Ethics Standards Board for Accountants (IESBA), which is responsible for the production of the Code of Ethics for Professional Accountants. The following is an example that illustrates the hierarchy:

According to the introduction to the revised edition of International Standards on Quality Control, Auditing, Assurance, and Related Services Pronouncements (2011), the standards that the IAASB produced are considered authoritative content.

As these standards are authoritative, they must be followed in an audit conducted in accordance with the ISAs.

In addition to publishing documents that are considered to be “authoritative,” the IAASB also publishes materials that are considered to be “non-authoritative,” which provide a type of “advice” rather than requirements. These are:

- International Auditing Practices Notes (IAPNs) – These are designed to provide practical assistance to auditors rather than impose mandatory requirements.

- Practice Notes Relating to Other International Standards.

- Staff Publications – these are designed to raise awareness of new or emerging issues about the standards and to direct attention to the relevant parts of IAASB pronouncements.

Some jurisdictions will have their bodies that are responsible for standard-setting. For instance, the Financial Reporting Council is the organisation in charge of establishing standards in the UK.

Some nations have decided to adopt ISAs, but such laws will need to be modified before they can be implemented. For instance, in the United Kingdom, ISAs are adopted; however, they are modified in certain areas so that they are compatible with UK standards; the resulting documents are nevertheless referred to as ISAs (UK and Ireland).

Example

The auditor is required by ISA 570 Going Concern to determine whether management has made a going concern assessment that covers a period of 12 months beginning on the date of the financial statements. However, in the United Kingdom and Ireland, this assessment of the company's ability to continue operations should encompass a period of one year beginning on the day that the financial statements are approved (or the date that is likely to be approved). Because of this, the ISA for the United Kingdom and Ireland spans a period of time that is distinct from that of the mainstream ISA; this exemplifies how the standard-setters have adapted the latter to be applicable only in the United Kingdom and Ireland. In the UK the going concern ISA is known as ISA (UK and Ireland) 570 Going Concern. In the UK and Ireland ISAs are frequently referred to as ‘ISA pluses’ because they contain additional or amended requirements to the mainstream ISA that is issued by the IAASB.