Effective 1 January 2022, the tax exemption for foreign-sourced income (“FSI”) received by Malaysian residents provided for under Para 28 was removed following the Budget 2022 made on 29 October 2021.

Hence, Foreign Income received in Malaysia which is eligible for the tax exemptions are as follows:

- Foreign dividend income received in Malaysia by a resident company, resident LLP and resident individual in relation to a partnership business in Malaysia [P.U.(A) 235/2022].

- All foreign income excludes income from a partnership business received in Malaysia by a resident individual [P.U.(A) 234/2022].

The exemption in paragraph 1.4(a) does not apply to a resident carrying on the business of banking, insurance, or sea or air transport.

On December 29, 2022, the Malaysian Inland Revenue Board (IRB) issued a press release (available only in Bahasa Malaysia) announcing an additional requirement for tax exemption on eligible persons’ foreign-source dividend income received in Malaysia.

In accordance with this additional requirement, amendments have been made to the Guidelines for tax treatment in relation to income received from abroad, which were uploaded to the official IRBM portal on December 29, 2022.

Foreign dividend income received in Malaysia by a resident company, resident LLP and resident individual in relation to partnership business in Malaysia from 1 January 2022 until 31 December 2026 is exempted from tax subject to the following conditions:

- Dividend income has been subjected to tax in the country of origin in which the income arises;

- The headline tax rate in the country of origin is not less than 15%; and

- Comply with the economic substance requirements.

In determining whether dividends have been subjected to tax in the country of origin in which the income arises [(1) above], the conditions are as follows:

(i) Tax has been imposed in the country of origin on foreign dividend income received in Malaysia as follows:

(A) Tax paid or payable in the country of origin is either income tax or withholding tax; or (B) Foreign dividend income received has been subjected to underlying tax;

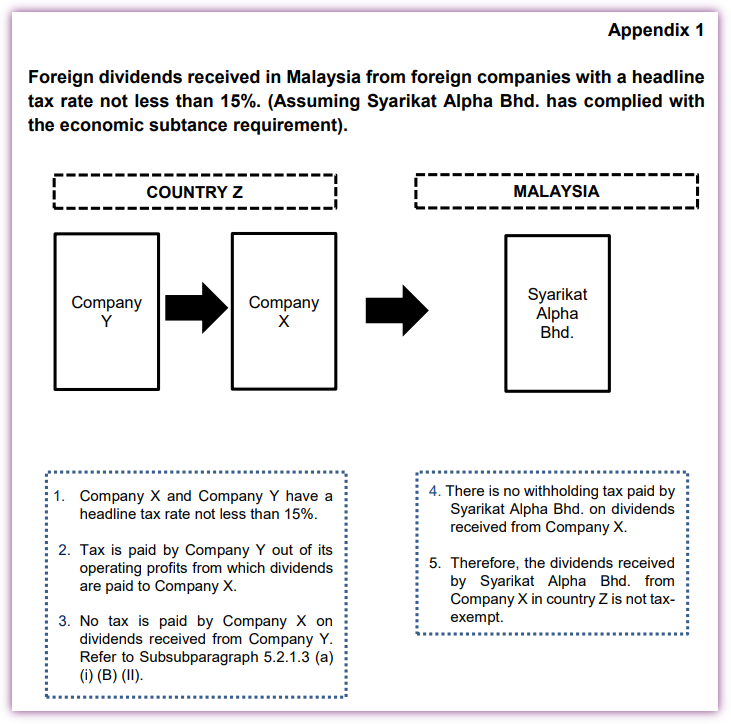

Note: I. Underlying tax is an income tax paid or payable in the country of origin related to the underlying profit that arises from operating income in the country of origin where the income after tax is used to pay dividends. II. If the payer company (Company X) pays dividends out of dividends received from another company (Company Y) (either within the country which is the same as Company X or otherwise), the underlying tax paid by Company Y on the dividend cannot be considered as tax paid or payable by Company X for the purpose of this qualifying conditions (refer to the illustration in Appendix 1).

or

(ii) Tax is not imposed in the country of origin because foreign dividends are paid out of underlying profits arising from operating income in the country of origin which is not subjected to tax due to:

(A) Unabsorbed losses or capital allowances;

(B) Arising from capital gains;

(C) Enjoyed tax incentives in compliance with substantive requirements in the country; or

(D) Tax regulations under the tax consolidation regime in the country of origin (refer to the illustration in Appendix 2(a) and 2(b)).

Appendix 1 of the Guidelines was extracted as follows:

CTIM Comment:

IRBM’s interpretation of P.U. (A) 235/2022 in the example above has very serious implications for the holding structure of Malaysian groups and multinationals with regional holding companies in Malaysia.

We request that IRBM recognize the fact the dividend ultimately arises from profits that have been subject to tax in a jurisdiction with a headline tax rate of at least 15%. In particular:

- The dividend paid by Syarikat X is traceable to the operating profits of Syarikat Y which has been subject to tax.

- The headline tax rate is at least 15%.

Hence, taxpayers should be allowed to take the view that the criteria imposed by P.U. (A) 235/2022 are satisfied.

Restricting the interpretation of the exemption criteria to only the payer of the dividend (i.e. Company X in the example above) will have serious and damaging consequences on industry practices and potentially on the national economy, on which we urge industry consultation to be initiated and we at CTIM are prepared to participate in further deliberation on this topic.

Response from IRBM:

It is a policy decision under the Ministry of Finance.

Disclaimer:

The articles, templates, and other materials on our website are provided only for your reference.

While we strive to ensure that the information presented is current and accurate, we cannot guarantee the completeness, reliability, suitability, or availability of the website or its content, including any related graphics. Consequently, any reliance on this information is entirely at your own risk.

If you intend to use the content of our videos and publications as a reference, we recommend that you take the following steps:

- Verify that the information provided is current, accurate, and complete.

- Seek additional professional opinions, as the scope and extent of each issue, may be unique.

免责声明:

我们网站上的文章、模板和其他材料只供参考。

虽然我们努力确保所提供的信息是最新和准确的,但我们不能保证网站或其内容,包括任何相关图形的完整性、可靠性、适用性或可用性。因此,您需要承担使用这些信息所带来的风险。

如果你打算使用我们的视频和出版物的内容作为参考,我们建议你采取以下步骤:

- 核实所提供的信息是最新的、准确的和完整的。

- 寻求额外的专业意见,因为每个问题的范围和程度,可能是独特的。

Keep in touch with us so that you can receive timely updates

请与我们保持联系,以获得即时更新。

1. Website ✍️ https://www.ccs-co.com/ 2. Telegram ✍️ http://bit.ly/YourAuditor 3. Facebook ✍

- https://www.facebook.com/YourHRAdvisory/?ref=pages_you_manage

- https://www.facebook.com/YourAuditor/?ref=pages_you_manage

4. Blog ✍ https://lnkd.in/e-Pu8_G 5. Google ✍ https://lnkd.in/ehZE6mxy

6. LinkedIn ✍ https://www.linkedin.com/company/74734209/admin/