After a long wait, the Finance Act 2023 was finally gazetted on 31 May 2023.

Amendments to various acts have been made, including:

- the Income Tax Act 1967 with 14 amendments,

- the Real Property Gains Tax 1976 with 1 amendment,

- the Stamp Act 1949 with 1 amendment,

- the Petroleum (Income Tax) Act 1967 with 5 amendments, and

- the Finance Act 2018 with 1 amendment.

For those interested in reading more, we to download the attachments below to access the full context:-

140.1 Finance Act 2023

Amendments to the Income Tax Act 1967 are as follows:-

Amendment of section 46 [in red]:

46(1) In the case of an individual or a Hindu joint family resident for the basis year for a year of assessment, there shall be allowed for that year of assessment personal deductions of:-

…………….

(g) medical expenses expended or deemed expended under subsection (3) in that basis year by that individual—

(i) on himself if he is undergoing treatment for a serious disease or on his wife or child who is undergoing treatment for a serious disease, or in the case of a wife, on herself, if she is undergoing treatment for a serious disease or on her husband or child who is undergoing treatment for a serious disease;

(ii) on himself if he is undergoing fertility treatment or on his wife who is undergoing fertility treatment, or in the case of a wife, on herself, if she is undergoing fertility treatment or on her husband who is undergoing fertility treatment; or

(iii) on himself, his wife or child for vaccination, or in the case of a wife, on herself, her husband or child for vaccination an amount limited to a maximum of one thousand ringgit:

Provided that—

(a) the claim is evidenced by a receipt and certification issued by a medical practitioner registered with the Malaysian Medical Council that the serious disease treatment was provided to that individual, spouse or child or that fertility treatment was provided to that individual or the spouse;

(b) the total amount of deduction under this paragraph is subject to a maximum amount of ten [before – “eight”] thousand ringgit;

(c) for the purpose of subparagraph (ii)—

(A) the individual is married; and

(B)”fertility treatment” means intrauterine insemination or in vitro fertilisation treatment or any other fertility treatment; and

(d) for the purposes of subparagraph (iii), the vaccinations which qualify for deduction are for:

- pneumococcal;

- human papillomavirus (HPV);

- influenza;

- rotavirus;

- varicella;

- meningococcal;

- TDAP combination (tetanus-diphtheria-acellular-pertussis); and

- Coronavirus Disease 2019 (COVID-19);

[Effective from Y/A 2023]

(h) an amount limited to a maximum of one thousand ringgit expended or deemed expended under subsection (3) in that basis year by that individual on himself or on his wife or on his child, or in the case of a wife, on herself or on her husband or on her child, in respect of—

(i) complete medical examination expenses as evidenced by receipts issued by a hospital or a medical practitioner registered with the Malaysian Medical Council;

(ii) Coronavirus Disease 2019 (COVID-19) detection test, as evidenced by receipts issued by a hospital or a medical practitioner registered with the Malaysian Medical Council or receipts of the purchase of Coronavirus Disease 2019 (COVID-19) self-detection test kit; or

(iii) mental health examination or consultation as evidenced by receipts issued by a hospital, a psychiatrist within the meaning of section 2 of the Mental Health Act 2001 [Act 615], a clinical psychologist registered with the Malaysian Allied Health Professions Council under the Allied Health Professions Act 2016 [Act 774] or a counsellor registered with the Board of Counsellors under the Counsellors Act 1998 [Act 580]:

Provided that the deduction under this paragraph shall be part of the amount limited to a maximum of ten [before – “eight”] thousand ringgit in paragraph (g);

[Effective from Y/A 2023]

(ha) an amount limited to a maximum of four thousand ringgit expended or deemed expended under subsection (3) in that basis year by that individual on his child who at any time in that basis year is of the age of eighteen years and below, in respect of:

(i) assessment for the purpose of diagnosis of learning disability certified by a medical practitioner registered with the Malaysian Medical Council; or

(ii) early intervention programme or rehabilitation treatment for learning disability conducted by an allied health practitioner in the field of learning disability registered under the Allied Health Professions Act 2016:

Provided that—

(a) the claim is evidenced by a receipt and certification issued by the medical practitioner that the assessment for the purpose of diagnosis was provided to the child and that the child is diagnosed with learning disability;

(b) the claim is evidenced by a receipt and certification issued by the allied health practitioner that the early intervention programme or rehabilitation treatment was provided to the child;

(c) the assessment for the purpose of diagnosis, early intervention programme or rehabilitation treatment which qualifies for deduction is for the following learning disabilities:

- autism spectrum disorder;

- attention deficit hyperactivity disorder;

- global developmental delay;

- intellectual disability;

- down syndrome; and

- specific learning disability;

(d) the assessment for the purpose of diagnosis, early intervention programme and rehabilitation treatment are provided in Malaysia;

(e) the maximum amount of deduction under this paragraph shall apply notwithstanding that, that individual may have more than one child; and

(f) the deduction under this paragraph shall be part of the amount limited to a maximum of ten thousand ringgit in paragraph (g);”; and

[Effective from Y/A 2023]

(k) an amount limited to a maximum of eight thousand ringgit deposited in that basis year by that individual for his child into the Skim Simpanan Pendidikan Nasional account established under the Perbadanan Tabung Pendidikan Tinggi Nasional Act 1997 [Act 566]:

Provided that if any withdrawal is made from the account by that individual in that basis year, the amount deposited during that year shall be reduced by that withdrawal and regard shall be had only to the reduced amount subject to a maximum amount of eight thousand ringgit;

[The Finance Act 2018 is amended in subsection 3(3) by substituting for the words “and 2022” the words “, 2022, 2023 and 2024”.]

(r) an amount limited to a maximum of two thousand ringgit expended or deemed expended under subsection (3) in respect of the payment of child care fees to a child care centre registered with the Director General of Social Welfare under the Child Care Centre Act 1984 [Act 308] or a kindergarten registered under the Education Act 1996 [Act 550] in that basis year by that individual for a child of that individual aged six years and below as evidenced by receipts issued by such child care centre or kindergarten:

Provided that—

- where a wife living together with her husband is assessed separately for that year, the deduction under this paragraph shall only be allowed either to the husband or to the wife;

- the maximum amount of deduction under this paragraph shall apply notwithstanding that, that individual may have more than one child; and

- a further one thousand ringgit shall be allowed for the years of assessment 2020 until 2024 [Before – “2023”];

[Extended to Y/A 2024]

46(3) For the purposes of subsections (1)(d), (g), (h), (ha) (k), (p), (r), (s), (t) and (u), any amount expended by the wife or the husband in the year of assessment—

(a) where subsection 45(2) applies, shall be deemed to have been expended by the husband of the wife who elects or by the wife of the husband who elects, as the case may be; or

(b) where the wife or the husband has no total income, shall be deemed to have been expended by the husband of that wife who has no total income or the wife of that husband who has no total income, as the case may be:

Provided that where paragraph 45(2)(b) applies or the husband has no total income, any amount expended by the husband shall be deemed to have been expended by the wife, who has been allowed a deduction under section 45A.

[Effective from Y/A 2023]

Amendment of section 49 [in red]:

49(1) Subject to this section, in the case of an individual resident for the basis year for a year of assessment, there shall be allowed for that year of assessment a deduction—

- not exceeding three thousand ringgit, in respect of premium paid by that individual for any insurance or any voluntary contribution made by that individual to the Employees Provident Fund or for both;

- not exceeding four thousand ringgit, in respect of any voluntary or obligatory contribution to the approved scheme (other than a private retirement scheme) made or suffered by that individual who is an employee or a self-employed person within the meaning of the Employees Provident Fund Act 1991 [Act 452], or a pensionable officer within the meaning of section 2 of the Pensions Act 1980; or

- not exceeding four thousand ringgit, in respect of any amount made or suffered by that individual on any contribution under any written law relating to widow, widower and orphan’s pension or under any approved scheme within the meaning of any such law.

[Effective from Y/A 2023]

49(1A) For the purpose of subsection (1)—

a. the total amount of deduction under subsection (1) shall not exceed seven thousand ringgit;

aa. the total amount of deduction for voluntary contribution to the Employees Provident Fund under paragraph (1)(a) shall not include the amount of deduction for voluntary contribution to the Employees Provident Fund under paragraph (1)(b) made by an individual who is an employee or a self-employed person within the meaning of the Employees Provident Fund Act 1991, or a pensionable officer within the meaning of section 2 of the Pensions Act 1980;

b. where subsection 50(2) or 50(3) applies, the amount of deduction to be allowed shall be in accordance with paragraphs (1)(a), (b) and (c) and the total deduction under subsection 50(2) or (3) shall not exceed seven thousand ringgit.

c. in the case of an individual who is a pensionable officer within the meaning of section 2 of the Pensions Act 1980 [Act 227] and no deduction is made under paragraph (1)(b) or (c) to that individual, the amount of deduction under paragraph (1)(a) shall not exceed seven thousand ringgit [Deleted].

[Effective from Y/A 2023]

49(2) For the purposes of subsection (1), other than voluntary contributions to the Employees Provident Fund made by any individual [Deleted – “a self-employed person within the meaning of the Employees Provident Fund Act 1991 or a pensionable officer within the meaning of section 2 of the Pensions Act 1980”], no regard shall be had to any contribution to an approved scheme unless the contribution was obligatory by reason of—

- any contract of employment of the individual claiming a deduction in respect of the contribution; or

- any provision in the rules, regulations, by-laws or constitution of the scheme,

and, where the contribution was partly obligatory by reason of such a contract or provision and partly not so obligatory, regard shall be had only to the part which was so obligatory.

[Effective from Y/A 2023]

Amendment of section 77: Return of income by a person other than a company, limited liability partnership, trust body or co-operative society [in red]:

77(1B) For the purposes of this section, the person referred to in subsection (1) shall furnish to the Director General a return in the prescribed form on an electronic medium or by way of electronic transmission in accordance with section 152A.

[Effective from Y/A 2024]

Amendment of section 77A: Return of income by every company, limited liability partnership, trust body or co-operative society [in red]:

77A(1A) For the purposes of this section, a company, limited liability partnership, trust body and co-operative society [Before – “a company and a limited liability partnership”] shall furnish to the Director General a return in the prescribed form on an electronic medium or by way of electronic transmission in accordance with section 152A.

[Effective from Y/A 2024]

Amendment of section 77B: Amendment of Return [in red]:

77B(1A) For the purposes of this section, a person who is a company, limited liability partnership, trust body and co-operative society shall furnish to the Director General an amended return in the prescribed form on an electronic medium or by way of electronic transmission in accordance with section 152A.”.

[Effective from Y/A 2024]

Amendment of section 83: Return by Employer [in red]:

83(1B) Where the employer is a company, limited liability partnership, trust body or co-operative society, the return referred to in subsection (1) shall be furnished on an electronic medium or by way of electronic transmission in accordance with section 152A.

[Effective from Y/A 2024]

Amendment of section 86: Return by Partnership [in red]:

86(1A) For the purposes of this section, the person referred to in paragraphs (1)(a) and (b) shall furnish to the Director General a return in the prescribed form on an electronic medium or by way of electronic transmission in accordance with section 152A.

[Effective from Y/A 2024]

Amendment of section 97A: Notification of non-changeability [in red]:

97A(5) Where a person has furnished to the Director General a return for a year of assessment in accordance with subsection 77(1) or 77A(1), and there is no chargeable income for that year of assessment, then if the person in respect of such return alleges that—

- there is an error or a mistake made by the person in that return; the person may make an application in writing to the Director General for an amendment to be made in respect of such return; or

- the amount that has been computed in return is inaccurate by reason of—

- any exemption, relief, remission, allowance or deduction granted for that year of assessment under this Act or any other written law published in the Gazette after the year of assessment in which the return is furnished;

- the approval for any exemption, relief, remission, allowance or deduction is granted after the year of assessment in which the return is furnished; or

- a deduction not allowed in respect of payment not due to be paid under subsection 107A(2), 107D(3) or 109(2), section 109A, or subsection 109B(2) or 109F(2) on the day a return is furnished,

the person may make an application in writing to the Director General for relief.

[Effective from 1.1.2023]

Amendment of section 103: Payment of tax [in red]:

103(3) [10% penalty on unpaid tax]

Subject to subsection (7), where [Before – “Where”] any tax due and payable under subsection (1) has not been paid by the due date, so much of the tax as is unpaid upon the expiration of that date shall without any further notice being served be increased by a sum equal to ten per cent of the tax so unpaid, and that sum shall be recoverable as if it were tax due and payable under this Act.

103(7) [Payment of tax by instalments]

Where any tax is payable in accordance with subsection (1), (1A) or (2), the Director General may allow the tax to be paid by instalments in such amounts and on such dates as he may determine and in the event of default in payment of any one instalment on the date specified for payment the balance of the tax then outstanding shall be due and payable on that date and shall without any further notice being served be increased by a sum equal to ten per cent of that balance, and that sum shall be recoverable as if it were tax due and payable under this Act.

[Effective from Y/A 2023]

Amendment of section 107B: Payment by instalments [in red]:

107B(2) [Determination of amount to be paid]

In determining the amount to be paid under subsection (1), the Director General may take into consideration the tax assessed, if any, in respect of the person for the year of assessment preceding that year of assessment:

Provided that the Director General may, upon an application made by the person once not later than the thirtieth day of June or once not later than the thirty-first day of October, or both [Before – “not later than the thirtieth day of June”] in that year of assessment, vary the amount to be paid by instalments on account of tax and the number of instalments.

[Effective from Y/A 2023]

Amendment of section 107D: Deduction of tax from the payment made to agent, etc. [in red]:

107D(1) Where a company, in this section referred to as the payer, is liable to make payments in monetary form to an agent, a dealer or a distributor at any time in a basis year for a year of assessment arising from sales, transactions or schemes carried out by that agent, dealer or distributor, the payer shall upon paying or crediting such payments in a calendar month deduct therefrom tax at the rate of two per cent of the payments on account of tax for that year of assessment which is or may be payable by that agent, dealer or distributor [deleted – “for any year of assessment”] and, whether or not that tax is so deducted, shall not later than the end of the following calendar month [deleted – “within thirty days”] after paying or crediting such payments render an account and pay the amount of that tax to the Director General:

Provided that the Director General may—

- give notice in writing to the payer requiring the payer to deduct and pay tax at some other rates or to pay or credit the payments without deduction of tax; or

- under special circumstances, allow extension of time for tax deducted to be paid over.

[Effective from 1.1.2023]

Amendment of section 131A: Relief other than in respect of error or mistake [in red]:

131A(1) Where any person who has furnished to the Director General a return for a year of assessment in accordance with subsection 77(1) or 77A(1) and has paid tax for that year of assessment alleges that the assessment relating to that year of assessment is excessive by reason of—

- any exemption, relief, remission, allowance or deduction granted for that year of assessment under this Act or any other written law is published in the Gazette after the year of assessment in which the return is furnished;

- the approval for any exemption, relief, remission, allowance or deduction is granted after the year of assessment in which the return is furnished; or

- a deduction not allowed in respect of payment not due to be paid under subsection 107A(2), 107D(3) or 109(2), section 109A, or subsection 109B(2) or 109F(2) on the day the return is furnished, the person may make an application in writing to the Director General for relief

[Effective from 1.1.2023]

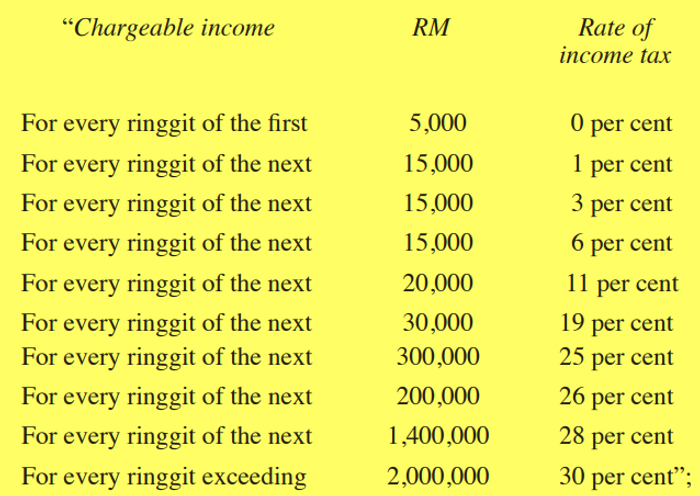

Amendment of Schedule 1 [in red]:

Part I — Rates of tax

1 Except where paragraphs 1A, 2, 2A, 2D, 3 and 4 provide otherwise, income tax shall be charged for a year of assessment upon the chargeable income of every person at the following rates:

[Effective from Y/A 2023]

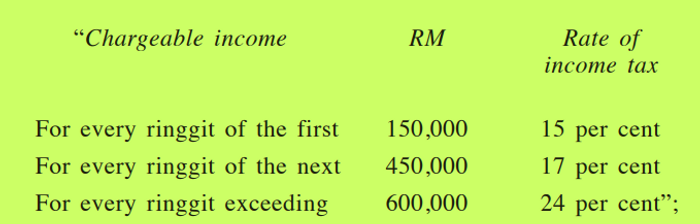

2A Subject to paragraphs 2B, 2C and 3, income tax shall be charged for a year of assessment on the chargeable income of a company resident and incorporated in Malaysia which has a paid-up capital in respect of ordinary shares of two million five hundred thousand ringgit and less at the beginning of the basis period for a year of assessment and gross income from source or sources consisting of a business not exceeding fifty million ringgit for the basis period for that year of assessment at the following rates:

[Effective from Y/A 2023]

2B The provisions of paragraph 2A shall not apply to a company referred to in that paragraph if more than—

- fifty per cent of the paid-up capital in respect of ordinary shares of the company is directly or indirectly owned by a related company;

- fifty per cent of the paid-up capital in respect of ordinary shares of the related company is directly or indirectly owned by the first-mentioned company; [Deleted – “or”]

- fifty per cent of the paid-up capital in respect of ordinary shares of the first mentioned company and the related company is directly or indirectly owned by another company; or

- twenty per cent of the paid-up capital in respect of ordinary shares of the company at the beginning of the basis period for a year of assessment is directly or indirectly owned by one or more companies incorporated outside Malaysia or by one or more individuals who are not citizens of Malaysia

[Effective from Y/A 2024]

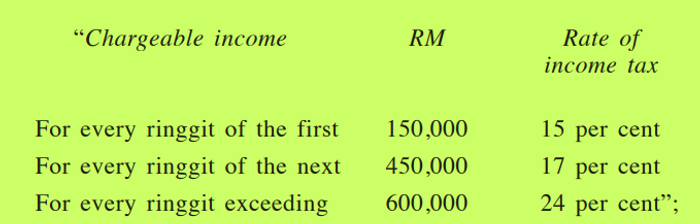

2D Subject to paragraphs 2E, 2F and 3, income tax shall be charged for a year of assessment on the chargeable income of a limited liability partnership resident in Malaysia which has a total contribution of capital (whether in cash or in kind) of two million five hundred thousand ringgit and less at the beginning of the basis period for a year of assessment and gross income from source or sources consisting of a business not exceeding fifty million ringgit for the basis period for that year of assessment at the following rates:

[Effective from Y/A 2023]

2E The provisions of paragraph 2D shall not apply to a limited liability partnership referred to in that paragraph if more than—

- fifty per cent of the capital contribution (whether in cash or in-kind) of the limited liability partnership is directly or indirectly contributed by a company;

- fifty per cent of the paid-up capital in respect of ordinary shares of the company is directly or indirectly owned by the limited liability partnership; [deleted – “or”]

- fifty per cent of the capital contribution (whether in cash or in-kind) of the limited liability partnership and fifty per cent of the paid-up capital in respect of ordinary shares of the company is directly or indirectly owned by another company; or

- twenty per cent of the capital contribution (whether in cash or in-kind) of the limited liability partnership at the beginning of the basis period for a year of assessment is directly or indirectly contributed by one or more companies incorporated outside Malaysia or by one or more individuals who are not citizens of Malaysia.

[Effective from Y/A 2024]

2F The company referred to in paragraph 2E, other than another company referred to in subparagraph 2E(c) and the company or companies incorporated outside Malaysia referred to in subparagraph 2E(d), shall have a paid-up capital in respect of ordinary shares of more than two million and five hundred thousand ringgit at the beginning of the basis period for a year of assessment.

[Effective from Y/A 2024]

Amendment of Schedule 3 [in red]:

70A(1) In this Schedule, “plant” means an apparatus used by a person for carrying on his business but does not include a building [deleted – “, an intangible asset,”] or any asset used and that functions as a place within which a business is carried on.

70A(2) Notwithstanding subparagraph (1), the Minister may prescribe any other assets as assets which are excluded from the definition of “plant.”

Amendments to the Real Property Gains Tax Act 1976 are as follows:-

Amendment of Schedule 2 [in red]:

3(1) In the following cases the disposal price shall be deemed to be equal to the acquisition price, that is to say—

(a) the devolution of the assets of a deceased person on his executor or legatee under a will or intestacy or on the trustees of a trust created under his will;

(b) (i) the transfer of assets between spouses; [deleted – “or”]

(ia) the transfer of assets between former spouses pursuant to an order of any court in consequence of the dissolution or annulment of their marriage; or”; and

(ii) the transfer of assets owned by an individual, by the wife of the individual or by an individual jointly with his wife or with a connected person, by a nominee for the individual, a nominee for the wife of the individual or a nominee for both, or by a trustee for the individual, a trustee for the wife of the individual or a trustee for both, to a company incorporated in Malaysia [deleted – “to a company resident in Malaysia or not”], controlled by the individual, by the wife of the individual, by the individual jointly with his wife or with a connected person, by the nominee for the individual, the nominee for the wife of the individual or the nominee for both, or by the trustee for the individual, the trustee for the wife of the individual or the trustee for both, for a consideration consisting of shares in the company or for a consideration consisting substantially of shares in the company and the balance of a money payment;

(c) acquisitions from or disposals to a nominee or trustee resident in Malaysia by an individual or his wife or by both being absolutely entitled as against the nominee or trustee;

(d) the conveyance or transfer of an asset by way of security, or the transfer of a subsisting interest or right by way of security in or over an asset (including re-transfer on the redemption of the security);

(e) gifts made to the Government, a State Government, a local authority or a charity exempt from income tax under the income tax law;

(f) the disposal of an asset as a result of compulsory acquisition under any law;

(g) the disposal of any chargeable asset pursuant to a scheme of financing approved by the Central Bank, the Labuan Financial Services Authority, the Malaysia Co-operative Societies Commission or the Securities Commission as a scheme which is in accordance with the principles of Syariah, where such disposal is strictly required for the purpose of compliance with those principles but which will not be required for any other schemes of financing.

3(2) Any transfer of assets between spouses or former spouses or to a company referred to in sub-subparagraph (1)(b) shall involve an asset owned by a citizen.

19(5) Where an asset which has been transferred under sub-subparagraph 3(1)(b) is subsequently disposed of by the spouse or former spouses or the company, the disposer shall be deemed to have acquired the asset at an acquisition price equal to the acquisition price paid by the transferor plus the permitted expenses incurred by the transferor or, if the asset was acquired by the transferor prior to 1 January 1970, the market value of the asset as at 1 January 1970 plus the permitted expenses incurred by the transferor as from 1 January 1970 less the sum of the kind referred to in sub-subparagraph 4(1)(a), (b) or (c) received by or forfeited as the case may be to the transferor as from 1 January 1970.

Disclaimer:

The articles, templates, and other materials on our website are provided only for your reference.

While we strive to ensure that the information presented is current and accurate, we cannot guarantee the completeness, reliability, suitability, or availability of the website or its content, including any related graphics. Consequently, any reliance on this information is entirely at your own risk.

If you intend to use the content of our videos and publications as a reference, we recommend that you take the following steps:

- Verify that the information provided is current, accurate, and complete.

- Seek additional professional opinions, as the scope and extent of each issue, may be unique.

免责声明:

我们网站上的文章、模板和其他材料只供参考。

虽然我们努力确保所提供的信息是最新和准确的,但我们不能保证网站或其内容,包括任何相关图形的完整性、可靠性、适用性或可用性。因此,您需要承担使用这些信息所带来的风险。

如果你打算使用我们的视频和出版物的内容作为参考,我们建议你采取以下步骤:

- 核实所提供的信息是最新的、准确的和完整的。

- 寻求额外的专业意见,因为每个问题的范围和程度,可能是独特的。

Keep in touch with us so that you can receive timely updates

请与我们保持联系,以获得即时更新。

1. Website ✍️ https://www.ccs-co.com/ 2. Telegram ✍️ http://bit.ly/YourAuditor 3. Facebook ✍

- https://www.facebook.com/YourHRAdvisory/?ref=pages_you_manage

- https://www.facebook.com/YourAuditor/?ref=pages_you_manage

4. Blog ✍ https://lnkd.in/e-Pu8_G 5. Google ✍ https://lnkd.in/ehZE6mxy

6. LinkedIn ✍ https://www.linkedin.com/company/74734209/admin/