In the exercise of the powers conferred by paragraph 154(1)(b) read together with paragraph 33(1)(d) of the Income Tax Act 1967 [Act 53], the Minister, on September 9, 2022, gazetted the Income Tax (Deduction for Expenses in relation to the Cost of Detection Test of Coronavirus Disease 2019 (COVID-19) for Employees) (Amendment) Rules 2022 (P.U. (A) 291/2022) (“Amendment Rules“) to amend the Income Tax (Deduction for Expenses in relation to the Cost of Detection Test of Coronavirus Disease 2019 (COVID-19) for Employees) Rules 2021 [P.U. (A) 404/2021] (“Principal Rules”).

Income Tax (Deduction for Expenses in relation to the Cost of Detection Test of Coronavirus Disease 2019 (COVID-19) for Employees) Rules 2021

Under these Principal Rules, a Double Tax Deduction of expenses incurred by an employer resident in Malaysia for the cost of detection test of COVID-19 for its employees from 1 January 2021 until 31 December 2021.

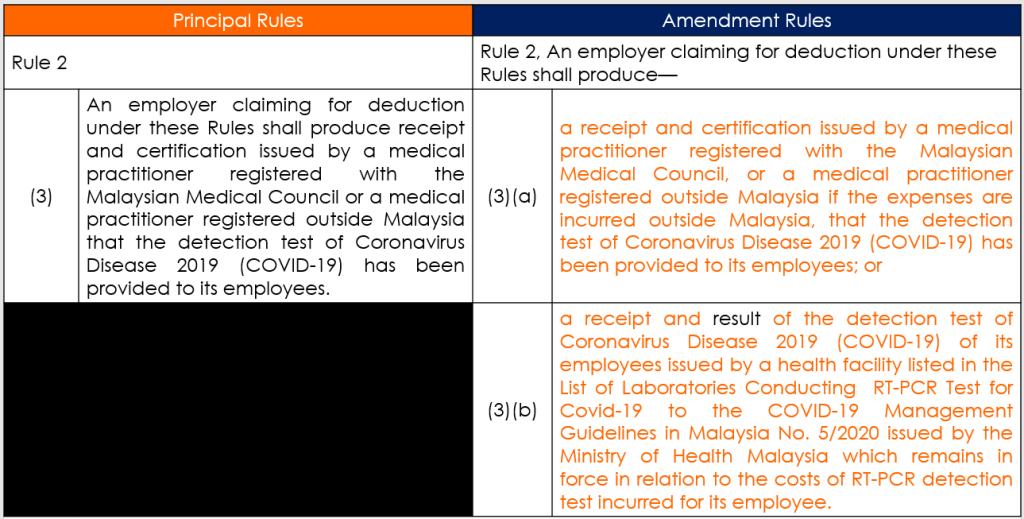

An employer who wishes to claim a deduction under the Rules must produce a receipt and certification issued by a medical practitioner registered with the Malaysian Medical Council or a medical practitioner registered outside Malaysia stating that the Covid-19 Detection Test has been provided to the employees of the employer.

Therefore, a medical report without a certificate is not eligible to claim this deduction.

Likewise, receipts without a certificate are also not eligible to claim this deduction.

The Inland Revenue Board of Malaysia has issued responses dated 18 May 2022 to CTIM members’ issues dated January 31, 2022, reiterating that Sub-rule 2(3) in P.U(A) 404/2021 must be complied with.

Income Tax (Deduction for Expenses in relation to the Cost of Detection Test of Coronavirus Disease 2019 (COVID-19) for Employees) (Amendment) Rules 2022

The Amendment Rules amend the Principal Rules to state that, as an alternative, an employer wishing to claim such a deduction may present a receipt and the results of the Covid-19 Detection Test performed on its employees and issued by a health facility listed in the List of Laboratories Conducting RT-PCR Test for Covid-19 to the COVID-19 Management Guidelines in Malaysia No. 5/20201 issued by the Ministry of Health Malaysia.

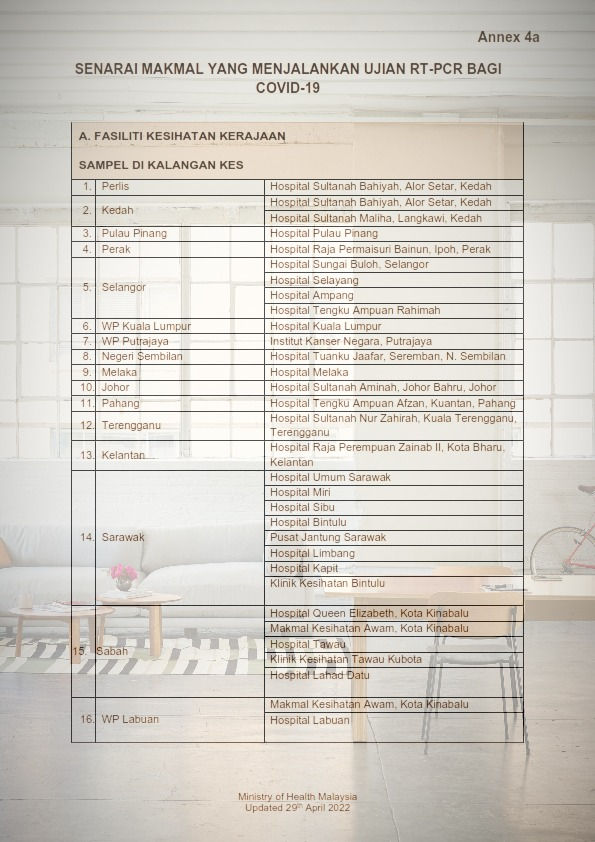

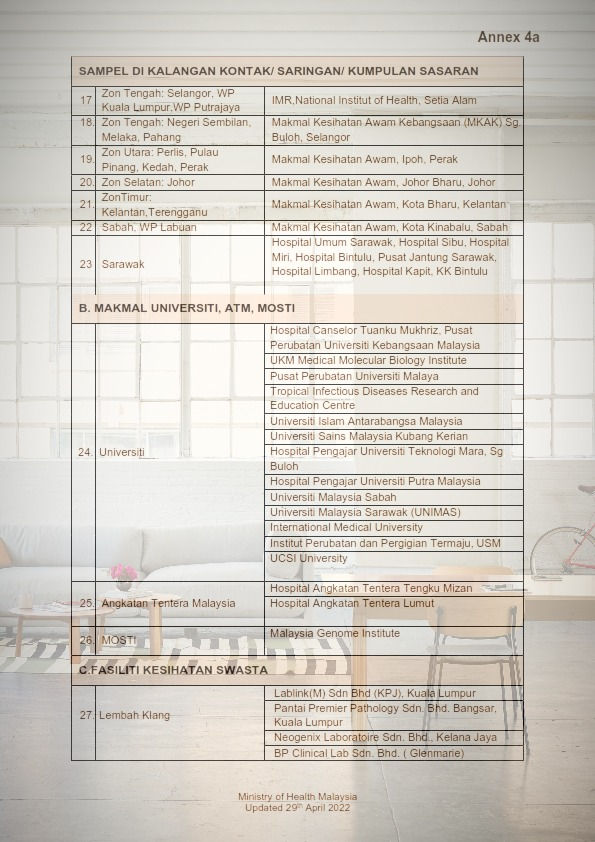

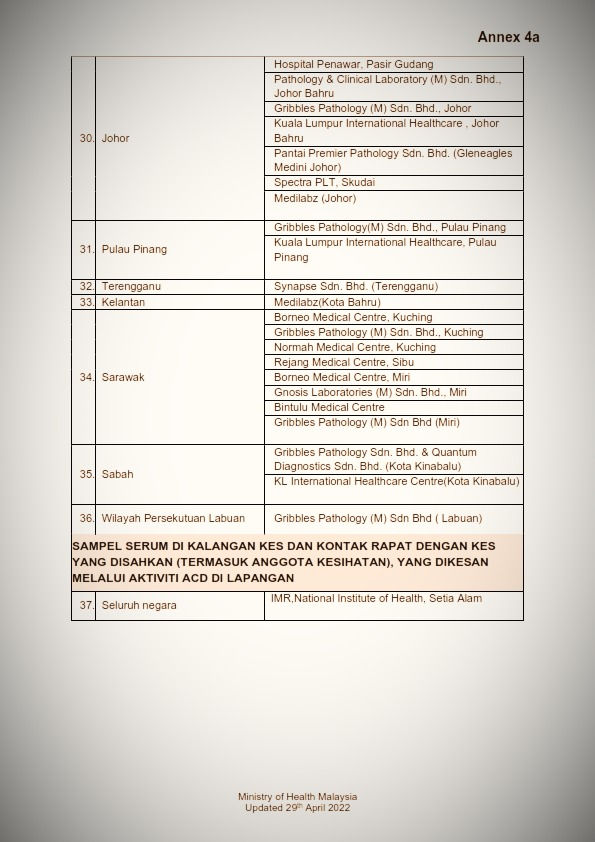

List of Laboratories Conducting RT-PCR Test for Covid-19 to the COVID-19 Management Guidelines in Malaysia No. 5/20201

To Download:

Our website's articles, templates, and material are solely for reference. Although we make every effort to keep the information up to date and accurate, we make no representations or warranties of any kind, either express or implied, regarding the website or the information, articles, templates, or related graphics that are contained on the website in terms of its completeness, accuracy, reliability, suitability, or availability. Any reliance on such information is therefore strictly at your own risk.

Keep in touch with us so that you can receive timely updates |

要获得即时更新,请与我们保持联系

1. Website ✍️ https://www.ccs-co.com/ 2. Telegram ✍️ http://bit.ly/YourAuditor 3. Facebook ✍

- https://www.facebook.com/YourHRAdvisory/?ref=pages_you_manage

- https://www.facebook.com/YourAuditor/?ref=pages_you_manage

4. Blog ✍ https://lnkd.in/e-Pu8_G 5. Google ✍ https://lnkd.in/ehZE6mxy

6. LinkedIn ✍ https://www.linkedin.com/company/74734209/admin/