Capital Allowances are a complex tax technical area largely governed by case law and precedent.

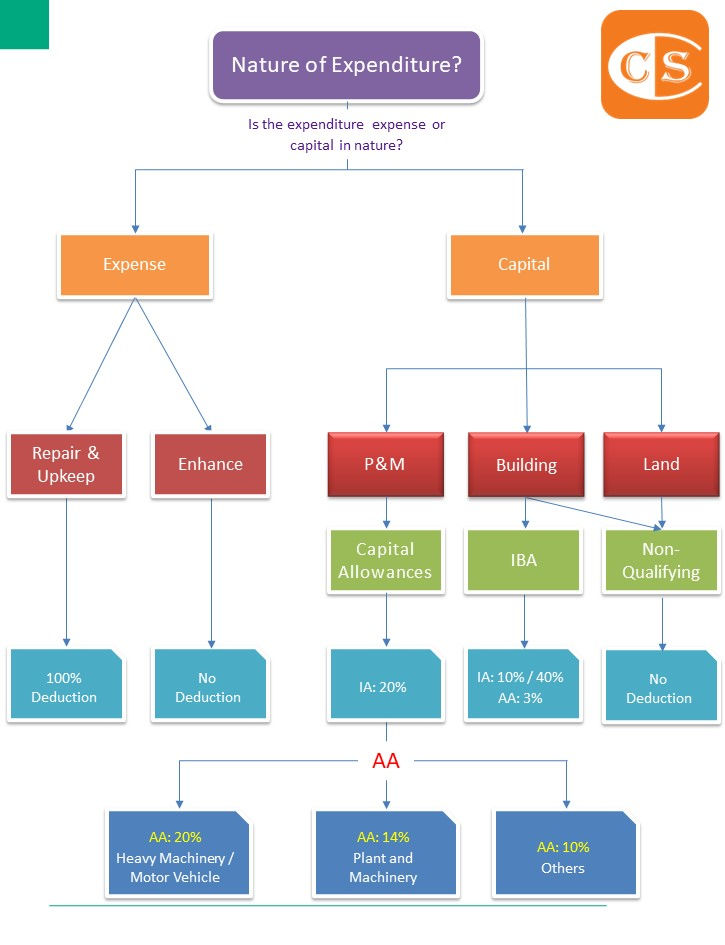

As illustrated in Fig. below, before calculating the Capital Allowances available in respect of capital expenditure incurred, two criteria must be considered:

- Is the expenditure expense or capital in nature?

- If it is capital, is it incurred on qualifying assets – i.e. P&M as per Schedule 3 of the Income Tax Act 1967, Industrial Buildings [also covered under Schedule 3 of the Income Tax Act 1967], or non-qualifying assets?

资本津贴在税收技术领域来说是一个复杂概念,主要受案例法 (Case Law) 和先例的制约。

如上图所示,在计算发生的资本支出可获得的资本津贴额之前,首先必须考虑两个标准:-

- 该支出的性质,究竟是费用还是资本?

- 如果是资本,它是发生在符合条件的资产上– 即《1967年所得税法令》附表3规定的P&M,工业建筑 [也是涵盖在《1967年所得税法令》附表3中],还是不符合条件的资产?

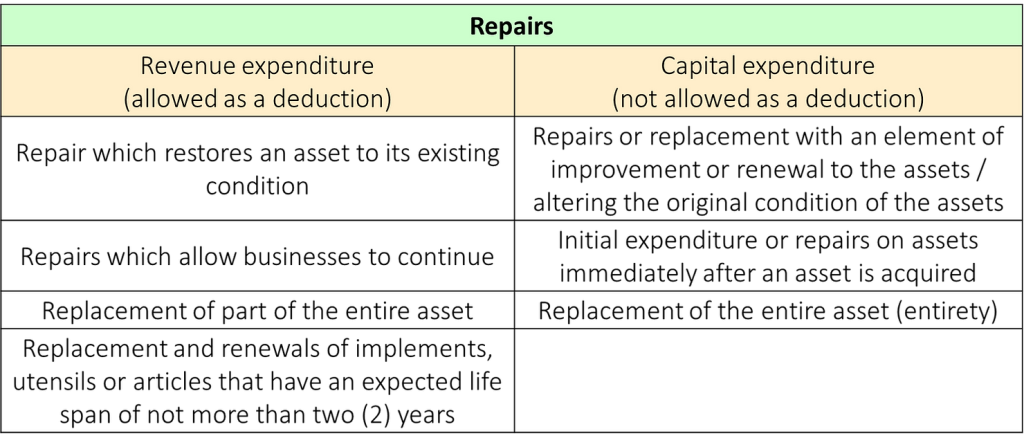

Expenses on Repairs and Renewals

In most cases, a person can reduce their overall gross income from a source such as a business or rental property by deducting expenses related to repairs and renewals.

Paragraph 33(1)(c) of the Income Tax Act 1967 (“ITA”) allows a deduction for the expenses wholly and exclusively incurred for:

- the repair of premises, plant, machinery or fixtures employed in the production of gross income; or

- the renewal, repair or alteration of any implement, utensil or article so employed in the production of gross income from that source other than implements, utensils or articles on which the expenditure would be qualifying plant expenditure for the purposes of Schedule 3 of the ITA.

However, the cost of reconstructing or rebuilding:

- any premises, buildings, structures or works of a permanent nature;

- any plant or machinery; or

- any fixtures

are not allowed as a deduction from the gross income in ascertaining the adjusted income from that source.

在大多数情况下,一个人可以通过扣除与维修和复新有关的费用来减少其来自某一来源(如:企业或出租房产)的总收入。

《1967年所得税法令》(”ITA”)第 33(1)(c) 段允许扣除完全和专门用于以下方面的费用:-

- 修理用于生产总收入的场所、厂房、机器或固定装置;或

- 更新、修理或改造用于生产总收入的任何工具、器具或物品;然而就《1967年所得税法令》附表3而言,该支出属于合格设备支出的工具、器具或物品除外。

然而,重建或改造的费用,源自于:

- 任何房舍、建筑物、结构或永久性工程。

- 任何工厂或机器;或

- 任何固定装置

在确定来自该来源的调整收入时,不允许从总收入中扣除。简单的来说,就是不能用来扣税。

The ITA does not include a definition for the word “Repair”

The word “repair” is defined as “to restore (a composite, structural, and others) to good condition by renewing or replacing the damaged parts” in The Shorter Oxford English Dictionary On Historical Principles – Third Edition.

In general, the term “repair” refers to the process by which an asset is returned to its initial condition without any component of improvement, addition, or alteration being included in the process.

This can be accomplished by renewing or replacing the parts of the asset that are damaged or inoperable, respectively.

“修复”一词在《牛津英语短词典–第三版》中被定义为 “通过更新或替换损坏的部分,将(复合材料、结构件和其他)恢复到良好状态”。

一般来说,”修复 “一词指的是将资产恢复到其初始状态的过程,在这一过程中不包含任何改进、增强或改造的成分。

这可以通过更新或替换资产中被损坏或无法使用的部分来实现。

When the effectiveness of an asset has decreased from its initial state because it has been employed in the operations of the business for some time, the asset requires some form of maintenance or repair.

In layman’s terms, it is an expense that was made purely to put the asset in the state it is currently in, enabling it to perform correctly to the level of efficiency it had previously possessed.

To put it another way, the process of repairing anything should not require the reconstruction or rebuilding of the entire asset or a significant portion of the entire asset.

当一项资产因为在企业运营中被采用了一段时间而从最初的状态下降时,该资产需要某种形式的维护或修理。

通俗地说,它是一种纯粹为了使资产处于目前的状态,使其能够正确地发挥以前所拥有的效率水平而进行的支出。

换句话说,修复任何东西的过程都不应该要求重建或重造整个资产或整个资产的很大部分。

Implements, utensils or articles with a life span of less than two years

Expenditure incurred on the replacement, repairs and renewal of implements, utensils or articles used in the production of income is allowed as a deduction against gross income on a replacement basis.

Generally, replacing implements, utensils or articles with an expected life span of not more than two (2) years is allowed as a deduction in ascertaining the adjusted income.

Normally, expenditure allowed on a replacement basis is the expenditure on the replacement of small items in terms of size and price.

更换、修理和更新用于生产总收入的工具、器具或物品所发生的支出,允许在更换基础上从总收入中扣除。

一般来说,更换预期寿命不超过两年的工具、器具或物品,在确定调整后的收入时,允许作为一项扣除。也就是说,这项费用可以直接拿来扣税。

通常情况下,这类型预期寿命不超过两年的工具、器具或物品,是指在尺寸上属于较小的物品,同时价格也不高。

Examples of implements, utensils or articles that can be allowed as a deduction on a replacement basis include dishes, spoons, forks, knives and pots.

The determination of the life span of an asset will be based on the facts of each case, and a person who wishes to claim a deduction on the asset is responsible for determining its life span.

The tax treatment on replacing implements, utensils or articles with an expected life span of not more than two (2) years applies to all types of business.

可以允许在重置基础上 (replacement basis) 进行直接扣税的器具、用具或物品的例子包括:盘子、勺子、叉子、刀子和锅子。

资产寿命的确定将基于每个案例的事实,想要对更新的资产直接扣税的纳税人,有责任确定其寿命。

更换预期寿命不超过两(2)年的器具、器皿或物品的税收待遇,适用于所有类型的企业。也就是说,即使是跨国大企业,如果他们有此项指出的话,同时也符合了资格,那么他们也享有此税务便利。

Example

Restaurant C (RC) has been in operation since 2017.

In 2021, RC incurred expenses of RM2,000 to purchase 200 dinner plates to replace some of the existing chipped and cracked crockeries.

RC can claim those expenses for deduction against gross income on a replacement basis for the year assessment 2021.

However, for expenditure allowed on a replacement basis for implements, utensils or articles used in the production of income, such expenses shall be allowed when incurred for the second time.

Expenses incurred for the first time on the asset are regarded as capital expenditure and are not allowed as a deduction.

The same applies to the estimated provision provided to replace implements, utensils or articles used in the production of income which is not allowed since the expenditure is not incurred.

例子

C餐厅(RC)自2017年开始经营。

在2021年,RC 支付了 2,000 令吉的费用购买了200个餐盘,以替换现有的一些有缺口和裂纹的陶器。

在2021年评估年度,RC 可以要求将这些费用按更换基础 (replacement basis) 从总收入中扣除。

然而,对于允许在更换基础 (replacement basis) 上用于生产收入的工具、器具或物品的支出,这些支出需要在第二次产生时才会被允许扣税。也就是说,第一次的第一笔支出,是不能扣税的 [第一次发生在资产上的支出被视为资本支出,不允许扣除]。

同样的情况也适用于为更换用于生产收入的工具、器具或物品而提供的预计拨备 (estimated provision) 经费,由于该支出没有发生,所以不允许扣除。

在会计术语上,预计拨备属于一项只是公司预估会产生的费用,并在账面上作出拨备(Provision)。然而,实际上,有关费用尚未真正发生。

Our website's articles, templates, and material are solely for you to look over. Although we make every effort to keep the information up to date and accurate, we make no representations or warranties of any kind, either express or implied, regarding the website or the information, articles, templates, or related graphics that are contained on the website in terms of its completeness, accuracy, reliability, suitability, or availability. Therefore, any reliance on such information is strictly at your own risk.

Keep in touch with us so that you can receive timely updates |

要获得即时更新,请与我们保持联系

1. Website ✍️ https://www.ccs-co.com/ 2. Telegram ✍️ http://bit.ly/YourAuditor 3. Facebook ✍

- https://www.facebook.com/YourHRAdvisory/?ref=pages_you_manage

- https://www.facebook.com/YourAuditor/?ref=pages_you_manage

4. Blog ✍ https://lnkd.in/e-Pu8_G 5. Google ✍ https://lnkd.in/ehZE6mxy

6. LinkedIn ✍ https://www.linkedin.com/company/74734209/admin/