Small and medium-sized enterprises (SMEs) are integral to the Malaysian economy as they contribute 38% or more than RM500bil to our gross domestic product (GDP).

There were altogether 1,226,494 MSMEs in 2021 which accounts for 97.4% of overall establishments in Malaysia.

Today we are pleased to inform you of an important update regarding the redefinition of the ‘Micro, Small and Medium Enterprise’ (MSME) under the Income Tax Act 1967.

Effective from the Year of Assessment 2024 (YA 2024), new provisions, namely Para 2B(d) and 2E(d) of Part I of Schedule 1, have been introduced to refine the criteria for qualifying as an MSME.

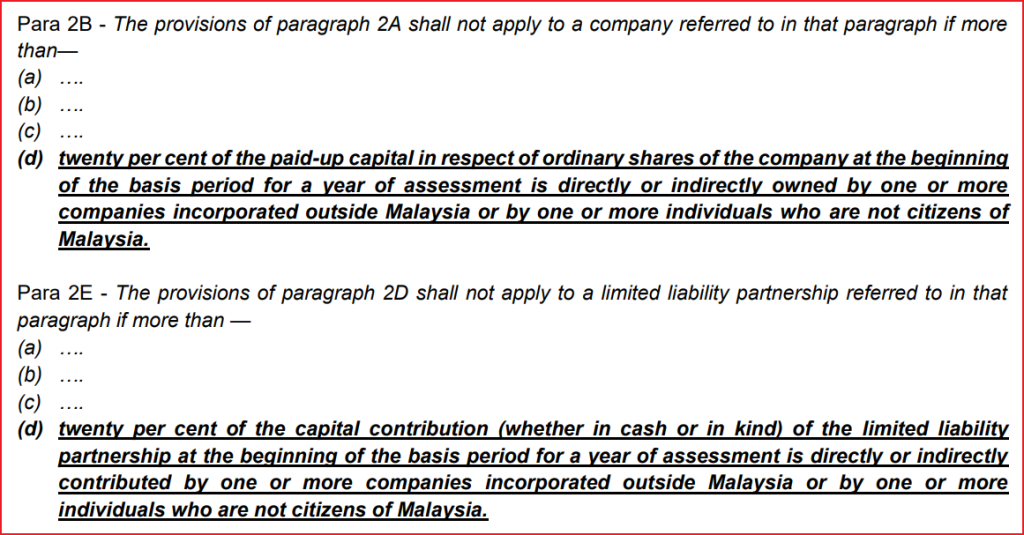

New Para 2B(d) & 2E(d) of Part I of Sch 1 (with effective YA 2024) are read as follows:-

Under Para 2B, the existing provisions mentioned in Para 2A will not apply to a company if more than 20% of the paid-up capital in respect of ordinary shares of the company, at the beginning of the basis period for a year of assessment, is directly or indirectly owned by one or more companies incorporated outside Malaysia or by one or more individuals who are not citizens of Malaysia.

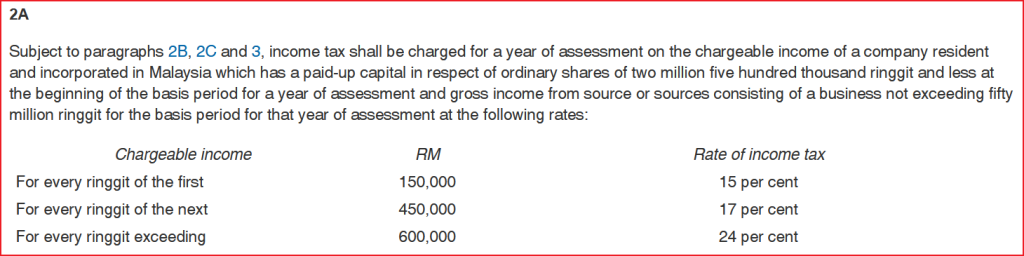

Para 2A of Part I of Sch 1 (with effective YA 2024) is read as follows:-

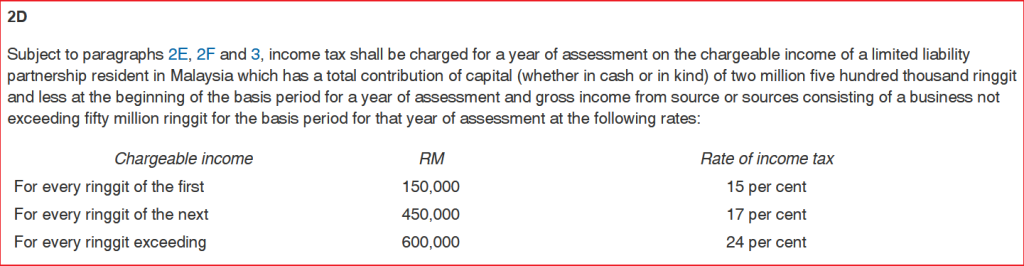

Similarly, under Para 2E, the provisions mentioned in Para 2D will not apply to a limited liability partnership (LLP) if more than 20% of the capital contribution, whether in cash or kind, of the LLP at the beginning of the basis period for a year of assessment, is directly or indirectly contributed by one or more companies incorporated outside Malaysia or by one or more individuals who are not citizens of Malaysia.

These changes aim to refine the definition of an MSME by ensuring that businesses predominantly owned by foreign companies or individuals are excluded from the MSME category.

The government believes that this modification will better align the definition with the intended purpose of supporting and promoting local enterprises.

The redefined criteria for MSMEs will apply for the Year of Assessment 2024.

Grandfathering Rules Does Not Apply

In response to inquiries regarding grandfathering rules for existing Micro, Small and Medium Enterprises (MSMEs) and Limited Liability Partnerships (LLPs) that currently meet all the pre-requisite conditions as MSMEs or LLPs as of the Year of Assessment (YA) 2023, we would like to provide the following feedback from Lembaga Hasil Dalam Negeri Malaysia (LHDNM):

There will be no application of grandfathering rules for the proposed amendments. The proposed amendments will take effect from the Year of Assessment 2024 and subsequent assessment years.

This means that the additional criterion, as stated in Para 2B(d) and 2E(d) of Part I of Schedule 1, will apply to all MSMEs and LLPs from the Year of Assessment 2024 onwards, irrespective of their previous categorisation.

It is important for existing MSMEs and LLPs to review their ownership structures and assess their eligibility under the redefined criteria.

While the new provisions may impact their categorisation, it is crucial to comply with the updated regulations to ensure accurate classification and potentially access any benefits or incentives associated with the MSME category.

We encourage all businesses to review their ownership structures and assess their eligibility under the updated regulations.

The “more than 20%” threshold is not applicable if the ultimate shareholder (owned more than 50% of the paid-up capital in respect of ordinary shares) is a company incorporated in Malaysia or individuals who are Malaysian citizens.

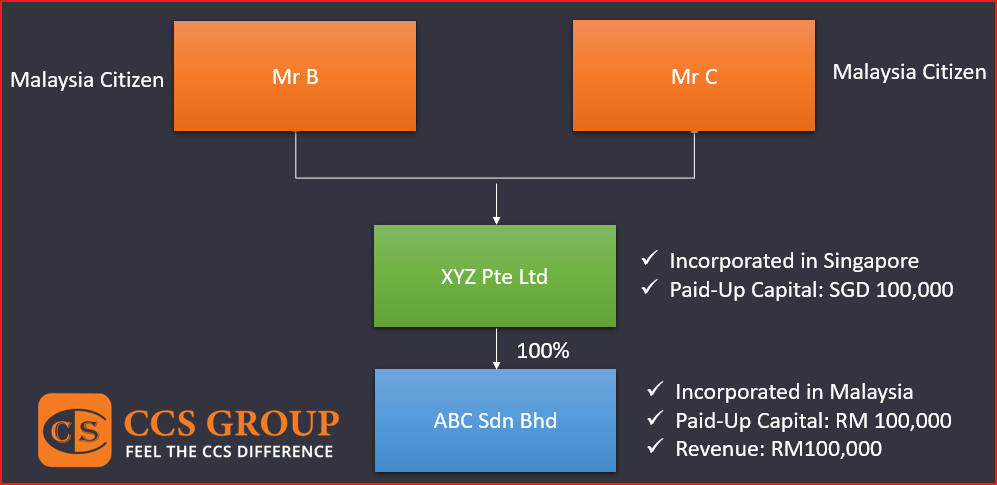

Illustration:-

Based on the above illustration, Feedback from LHDNM (Inland Revenue Board of Malaysia):

Under subparagraph 2B(d), Schedule 1 of the Income Tax Act 1967, to enjoy the preferential tax rate, a company/LLP (Limited Liability Partnership) cannot be owned more than 20% of the paid-up capital either directly or indirectly at the beginning of the basis period for an assessment year by one or more companies incorporated outside Malaysia or by one or more individuals who are not Malaysian citizens.

Therefore, ABC Sdn Bhd is not eligible to enjoy the tax rate under paragraph 2A, Schedule 1, of the Income Tax Act 1967, as more than 20% of the paid-up capital of ABC Sdn Bhd’s ordinary shares is directly held by XYZ Pte Ltd, which is incorporated outside of Malaysia, even though the ultimate shareholders, Mr A and Mr B, are Malaysian citizens.

It is important to ensure compliance with the revised provisions to maintain accurate categorisation and receive any benefits or incentives associated with the MSME classification.

The government remains committed to fostering a conducive environment for the growth and development of MSMEs.

These changes are aimed at strengthening the support provided to local enterprises and enabling them to thrive in a competitive business landscape.

If you would like more clarification or guidance on applying the amendments, we encourage affected MSMEs and LLPs to seek professional advice.

Q&A:

1. For Para 2A n 2D sch 1, the company is held by a foreign co. with> RM2.5m share cap in some years and < RM2.5m in other years due to forex difference, do we need to determine it yearly?

Yes. We need to determine the share capital of the SME company at the beginning of the year.

2. If the taxpayer no longer qualifies as PMKS, the tax rate will be flat 24%.

Yes. The tax rate will be 24%.

3. If the 20% foreign company shareholder is ultimately owned by a Malaysian, will this para apply? Can the company enjoy SME status?

The SME company is not eligible to enjoy the tax rate under paragraph 2A of Schedule 1 because 20% of the company’s shares are held by a foreign company.

4. Will this affect the exemption for submission of tax estimation for the first 2 years of assessment upon commencement of business?

Amendment on para 2A, Part 1, Schedule 1 will not affect the exemption for submission of tax estimation.

5. Besides the RM2.5m paid-up capital and the gross income not exceeding the RM50M criteria, do we need to check the shareholding for the SMSE tax rate?

Yes

6. Will it affect Section 107C (4A)- definition for companies not require to submit CP204 for 1st 2 YAs?

No

7. Does the 20% rule also applies to shares held by an individual foreigner/Malaysian permanent resident? What if the 20% shareholders are foreigners who are tax residents who have resided in Malaysia for years? Will the company not enjoy the reduced tax rate for their company?

PMKS Company is not eligible to enjoy the tax rate under paragraphs 2A and 2D, Part I, Schedule I if the company’s ownership consists of more than 20% ordinary shares held directly or indirectly by a company incorporated outside Malaysia or individuals who are not Malaysian citizens.

The same condition also applies to limited liability partnerships with capital contributions held by more than 20% by a company incorporated outside Malaysia or contributed by individuals, not Malaysian citizens.

Disclaimer:

The articles, templates, and other materials on our website are provided only for your reference.

While we strive to ensure that the information presented is current and accurate, we cannot guarantee the completeness, reliability, suitability, or availability of the website or its content, including any related graphics. Consequently, any reliance on this information is entirely at your own risk.

If you intend to use the content of our videos and publications as a reference, we recommend that you take the following steps:

- Verify that the information provided is current, accurate, and complete.

- Seek additional professional opinions, as the scope and extent of each issue, may be unique.

免责声明:

我们网站上的文章、模板和其他材料只供参考。

虽然我们努力确保所提供的信息是最新和准确的,但我们不能保证网站或其内容,包括任何相关图形的完整性、可靠性、适用性或可用性。因此,您需要承担使用这些信息所带来的风险。

如果你打算使用我们的视频和出版物的内容作为参考,我们建议你采取以下步骤:

- 核实所提供的信息是最新的、准确的和完整的。

- 寻求额外的专业意见,因为每个问题的范围和程度,可能是独特的。

Keep in touch with us so that you can receive timely updates

请与我们保持联系,以获得即时更新。

1. Website ✍️ https://www.ccs-co.com/ 2. Telegram ✍️ http://bit.ly/YourAuditor 3. Facebook ✍

- https://www.facebook.com/YourHRAdvisory/?ref=pages_you_manage

- https://www.facebook.com/YourAuditor/?ref=pages_you_manage

4. Blog ✍ https://lnkd.in/e-Pu8_G 5. Google ✍ https://lnkd.in/ehZE6mxy

6. LinkedIn ✍ https://www.linkedin.com/company/74734209/admin/