1. Individual tax residents must subtract personal reliefs — such as those for the individual taxpayer, children, and so on — from their Total Income to arrive at Chargeable Income.

2. Next, it is necessary to apply the appropriate tax rates to the Chargeable Income, which are determined by:

👉 the type of taxpayer in question (for example, a knowledge worker in Iskandar Malaysia is taxed at 15%.) and

👉 the rate of tax applicable to that person (Graduated Tax Rates apply to resident individuals).

👉 Since non-individuals are not eligible for personal exemptions, the chargeable income of non-individuals (including companies, Limited Liability Partnership, etc.) will be the same as total income.

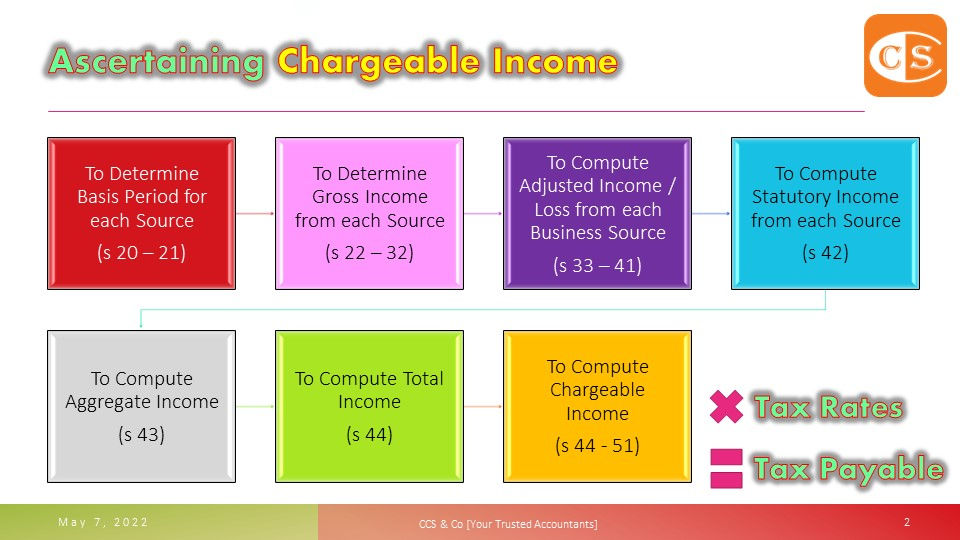

3. As to how to Determine the Basis Period for each Source, Determine Gross Income from each Source, Compute Adjusted Income / Loss from each Business Source, Compute Statutory Income from each Source, Compute Aggregate Income, and Compute Total Income, are other stories.

4. Join our Telegram – https://t.me/YourAuditor

🌻🌻🌻🌻🌻🌻🌻🌻🌻🌻🌻🌻

1. 个人税收居民必须从其总收入(Total Income)中减去个人减免 — 如针对其本身、子女等的减免,以得出应征税收入(或称之为“课税收入”)。

2. 接下来,有必要对应征税收入(或称之为“课税收入”,Chargeable Income)施予适当的税率,这一点由以下因素决定: 👉 有关纳税人的类型(例如,马来西亚伊斯干达的知识工作者的税率为15%);和 👉 适用于该人的税率(累进税率 (Graduated Tax Rates) 仅适用于税务居民个人)。 👉 由于非个人不能享受个人减免的待遇,非个人(包括公司、有限责任合伙公司等)的应征税收入(或称之为“课税收入”)将与总收入 (Total Income)相同。

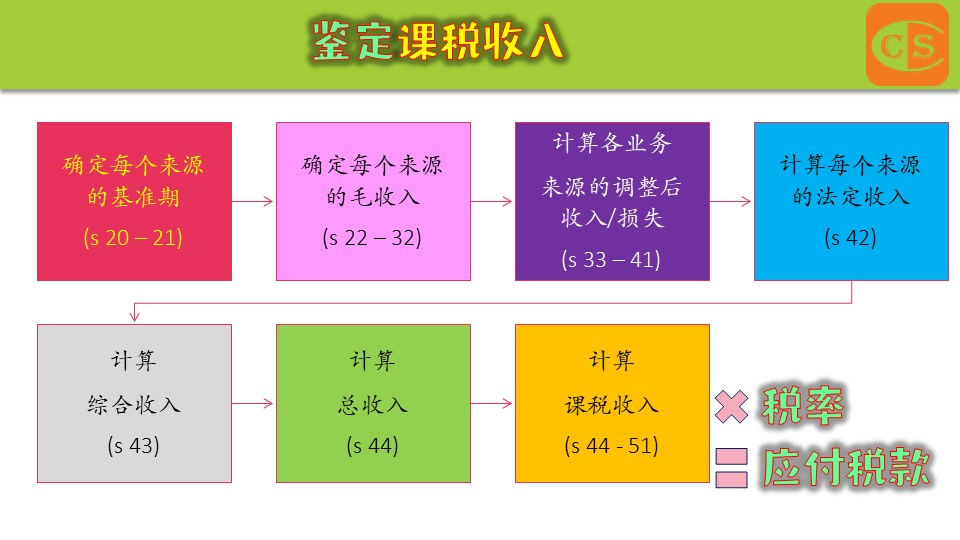

3. 至于如何确定每个来源的基准期,确定每个来源的毛收入 (Gross Income),计算每个业务来源的调整收入/损失 (Adjusted Income / Loss),计算每个来源的法定收入 (Statutory Income),计算总收入(Total Income),以及计算课税收入 (Chargeable Income),是另一个故事

4. Join our Telegram – https://t.me/YourAuditor 🌳🌳🌳🌳🌳🌳🌳🌳🌳🌳🌳🌳