The Accounting Requirements for Business Combinations have not been altered due to the amendments made to MFRS 3 Business Combinations; instead, MFRS 3’s reference to the Conceptual Framework for Financial Reporting has been brought up to date.

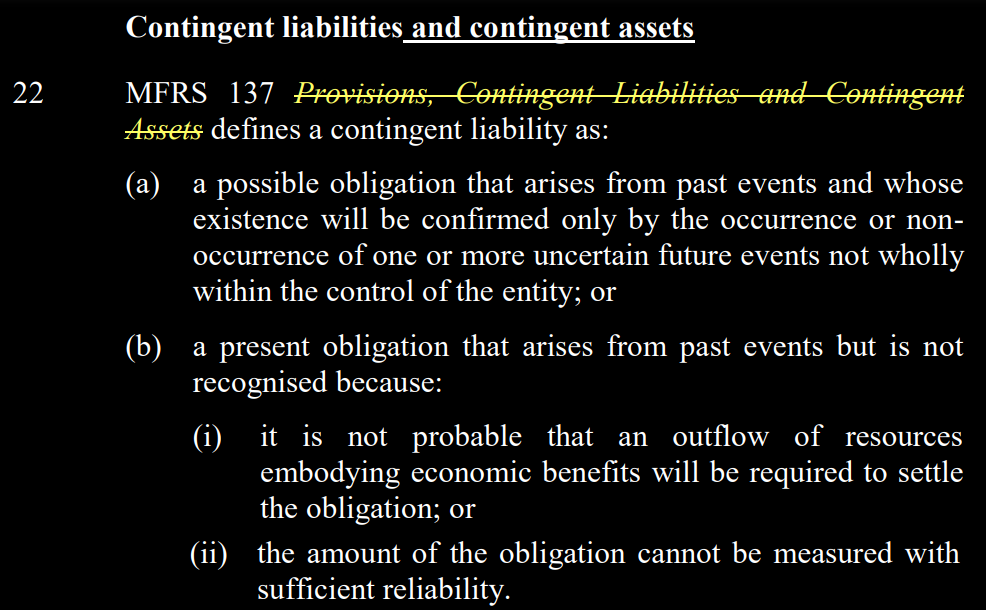

In addition, the amendments make it clear that contingent assets should not be recognised at the acquisition date.

An entity shall apply those amendments to business combinations for which the acquisition date is on or after the beginning of the first annual reporting period beginning on or after 1 January 2022.

Earlier application if at the same time or earlier an entity also applies all amendments made by Amendments to References to the Conceptual Framework in MFRS Standards issued in April 2018.

Amendments:

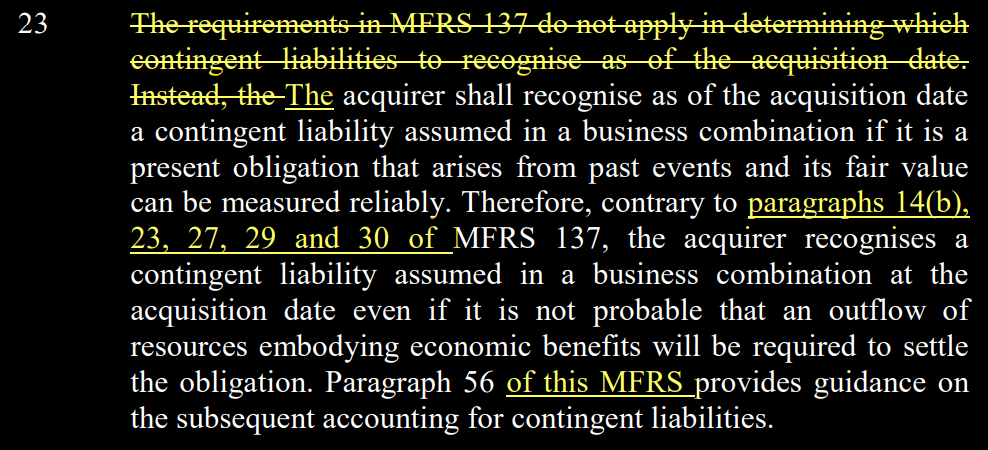

New text is underlined, and deleted text is struck through.

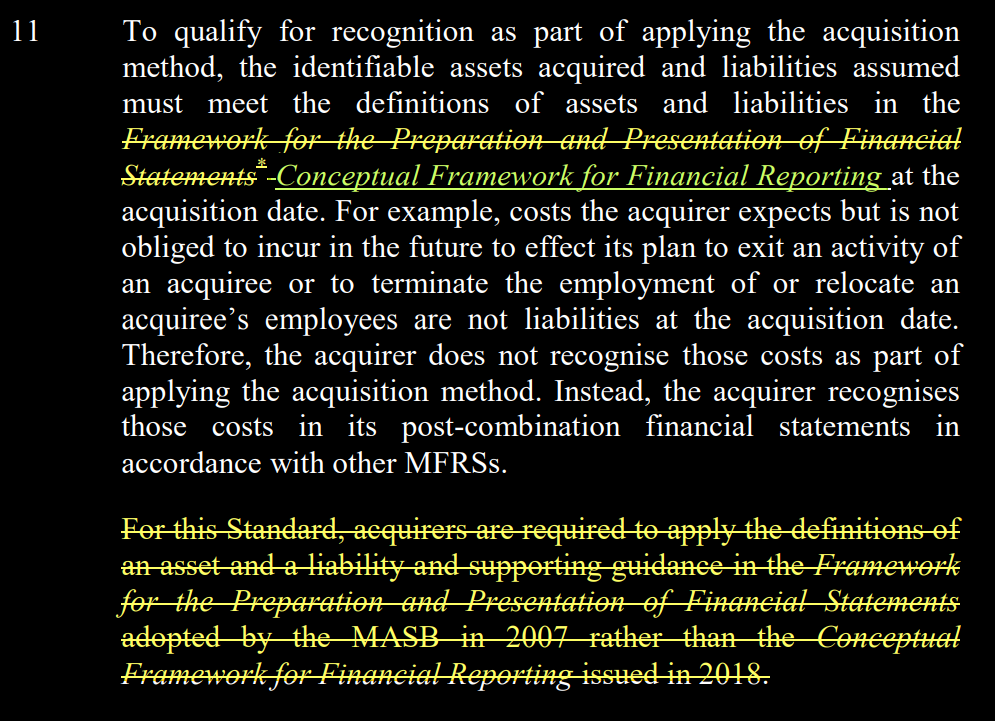

- Paragraph 11 is amended, and the footnote to Framework for the Preparation and Presentation of Financial Statements in paragraph 11 is deleted.

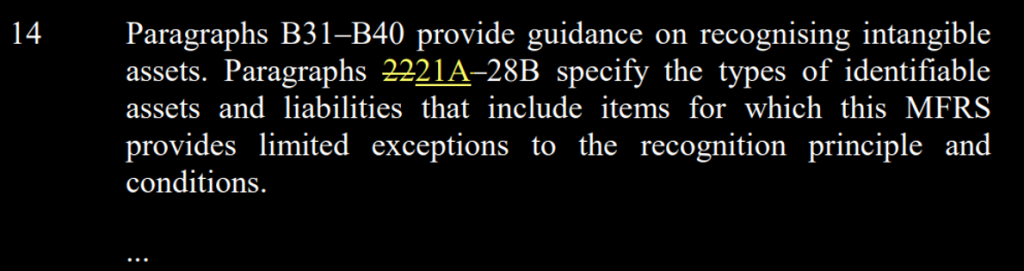

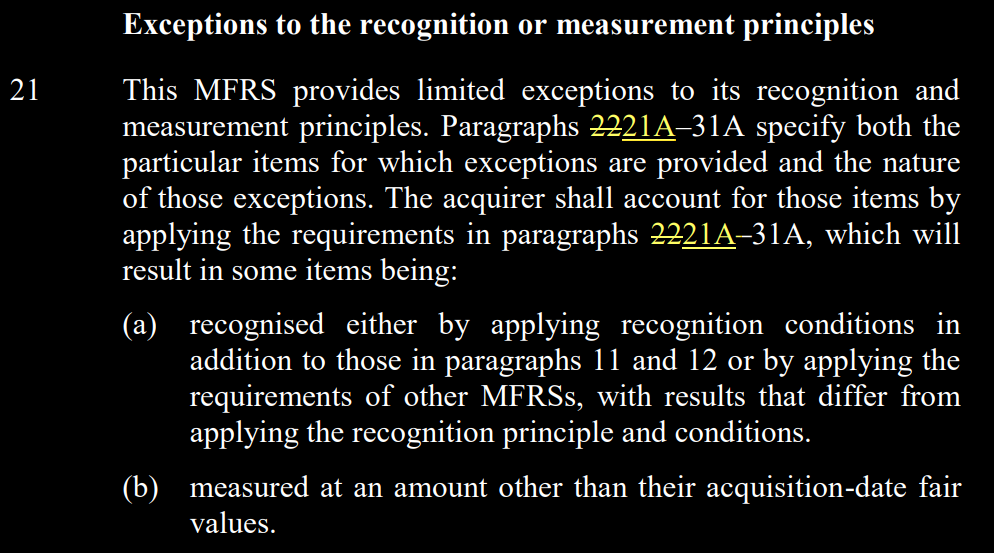

- Paragraphs 14, 21, 22 (The headings below paragraph 21 and above paragraph 22 are amended) and 23 are amended;

- Paragraphs 21A (A heading is added above the paragraph), 21B, 21C, 23A and 64Q are added;