Section 131A “Relief other than in respect of error or mistake” is read as follows:

Section 131A(1)

Where any person who has furnished to the Director General a return for a year of assessment in accordance with subsection 77(1) or 77A(1) and has paid tax for that year of assessment alleges that the assessment relating to that year of assessment is excessive by reason of:-

- any exemption, relief, remission, allowance or deduction granted for that year of assessment under this Act or any other written law is published in the Gazette after the year of assessment in which the return is furnished;

- the approval for any exemption, relief, remission, allowance or deduction is granted after the year of assessment in which the return is furnished; or

- a deduction not allowed in respect of payment not due to be paid under subsection 107A(2), 107D(3) or 109(2), section 109A, or subsection 109B(2) or 109F(2) on the day the return is furnished,

the person may make an application in writing to the Director General for relief.

Section 131A(2) The application under subsection (1) shall be made:-

- in respect of paragraphs (1)(a) and (b), within five years after the end of the year the exemption, relief, remission, allowance or deduction is published in the Gazette or the approval is granted, whichever is the later; or

- in respect of paragraph (1)(c), within one year after the end of the year the payment is made.

Section 131A(3) On receiving an application under subsection (1), the Director General shall inquire into the matter and may give by way of repayment of tax such relief as appears to the Director General to be just and reasonable.

Section 131A(4) An application under subsection (1) shall be as nearly as may be in the same form as a notice of appeal under section 99.

Section 131A(5) Where the applicant is aggrieved by the Director General’s decision on the application under subsection (1), the following provisions shall apply:

- the applicant may, within six months after being informed of the decision, request in the prescribed form for the Director General to forward the application to the Special Commissioners;

- the Director General shall within three months after receiving the request send the application forward as if he were sending an appeal forward pursuant to section 102; and

- the application shall thereupon be deemed to be an appeal and shall be disposed of accordingly.

In general, Section 131A outlines the process for persons who have submitted tax returns in accordance with specified sections, particularly subsections 77(1) or 77A(1).

Suppose a person believes their tax assessment is excessive due to changes such as newly granted exemptions, reliefs, or deductions. In that case, they can apply for relief by making a written request to the Director General within a prescribed timeframe.

The Director General will investigate the matter and may provide relief through tax repayment if deemed just and reasonable.

If dissatisfied with the decision, the applicant can appeal to the Special Commissioners within a specified period.

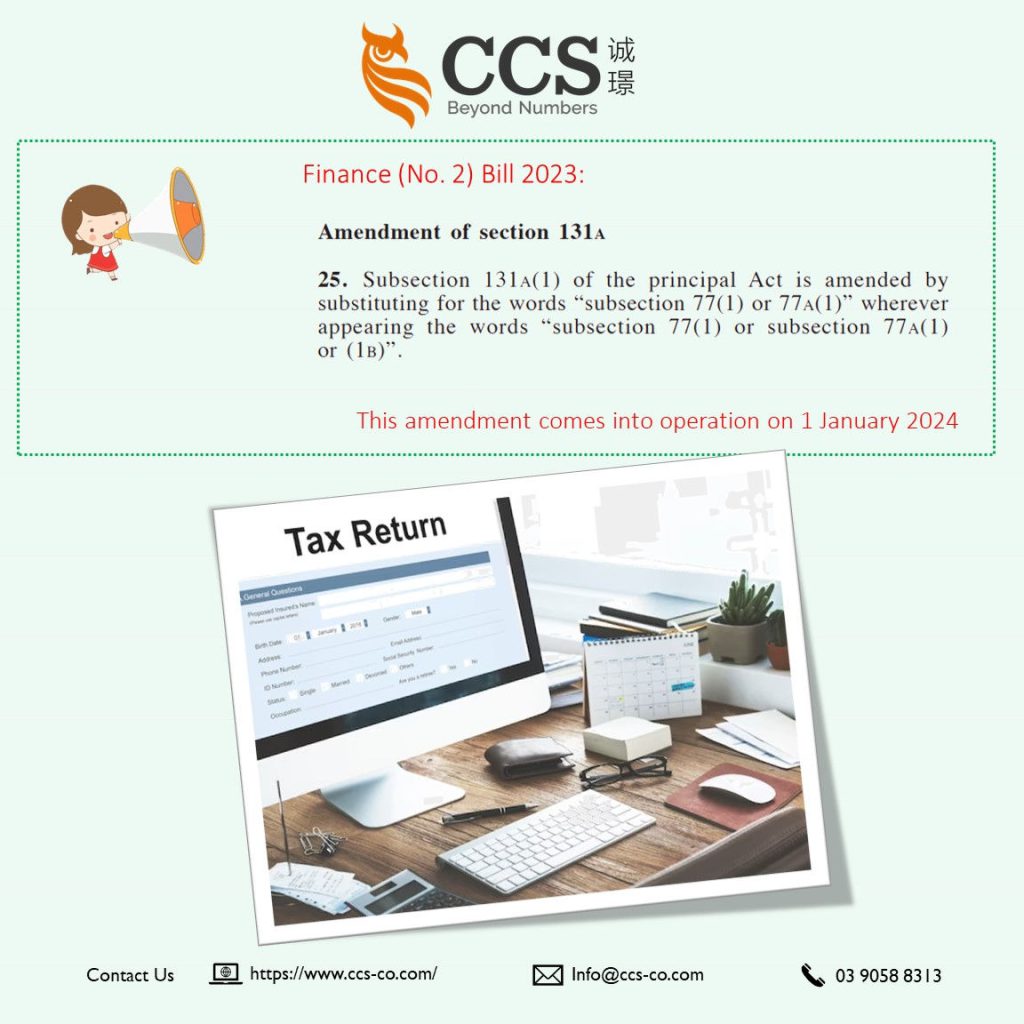

Amendment Description:

The proposed amendment to Section 131A involves substituting the words “subsection 77(1) or 77A(1)” with “subsection 77(1) or subsection 77A(1) or (1B).” This change aims to extend the provision to cover returns filed under the proposed new subsection 77A(1B). Under section 77A(1B), every company, limited liability partnership, trust body or cooperative society that disposes of a capital asset shall, within sixty days (or such other period the Director General may allow on a written request being made to him) of the date of disposal of that asset, furnish to the Director General a return in the prescribed form on an electronic medium or by way of electronic transmission in accordance with section 152A.

Reason for Amendment:

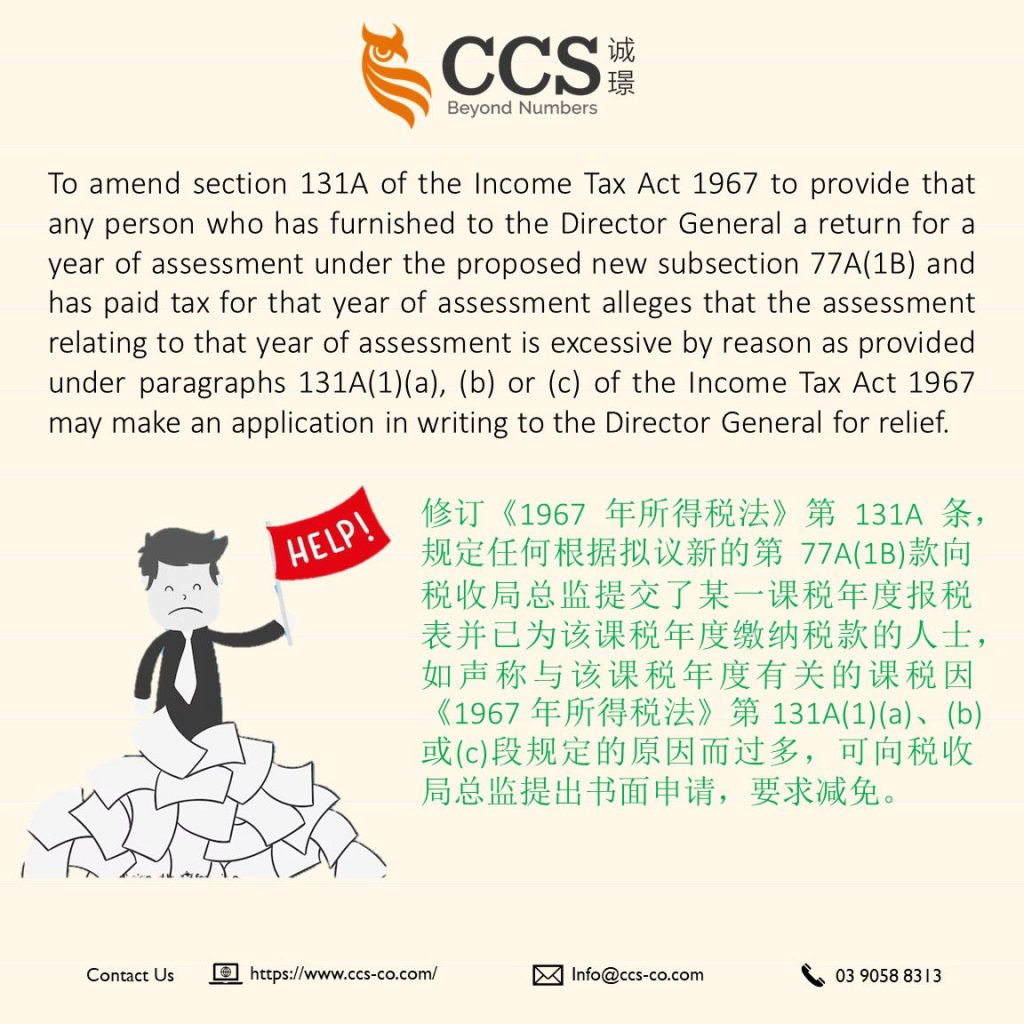

The reason behind this amendment is to specify that persons who have submitted a return for a year of assessment in accordance with the newly proposed subsection 77A(1B) can seek relief if they find the assessment for that year excessive.

The conditions for excessiveness are outlined in paragraphs 131A(1)(a), (b), or (c) of Act 53.

Tax Impact:

The tax impact of this amendment is significant for persons filing returns under the proposed subsection 77A(1B).

It extends the scope of relief for those who have paid tax for a particular assessment year and believe the assessment is excessive due to the specified reasons.

This amendment is set to be in operation from 1 January 2024, indicating that affected parties should be aware of the changes and adapt their practices accordingly to avoid adverse tax consequences.